The views expressed here are solely those of the author and do not necessarily represent the views of FreightWaves or its affiliates.

Normally we view changes in the intermodal rail business as a series of national data, lane data or big railway company reports.

This report card is different.

This week we look at intermodal rail from the point of view of J.B. Hunt (JBHT stock symbol) as the enterprise.

J.B. Hunt is selected because this analyst has been tracking the company since 1990. It has morphed from a trucker into the nation’s biggest single intermodal “train user.”

Today, it is the largest asset-based rail intermodal logistics company in North America.

What do we mean by the term asset-based? We mean that J.B. Hunt provides rail intermodal shippers with drivers, tractors, containers, trailers and integrated self-tracking/tracing transportation management system resources.

The J.B. Hunt fleet includes over 97,400 trailing units (mostly high-cube capacity, 53-foot domestic containers), including a growing reefer/container fleet. To that add just over 5,640 tractors.

Here is what J.B. Hunt doesn’t supply intermodally:

— Train crews.

— Train dispatching.

— Railroad tracks and structures.

— The railroad container stack cars and locomotives.

Essentially the railroads provide the real estate, train operating management and train sets.

J.B. Hunt provides the beneficial freight and the cargo container plus the drayage.

J.B. Hunt was the first beta test large trucker to engage in rail intermodal contracts in a big way.

How big?

They completely reengineered their trucking business model from long-distance highways to mostly long distance by rail plus local pickup and delivery truck drayage.

It was a gutsy move when they first linked their business fortune with the then-Santa Fe Railroad (now part of BNSF). The 1989 original deal with Santa Fe at the time surprised most railroaders. After all, trucking had until then been the enemy.

Why did Santa Fe’s senior management freely negotiate this deal? Because it was a way for the railroad company to serve shippers far beyond the limits of Santa Fe’s steel tracks.

Financially, there were some follow-on up and down years. Real life often disrupts the best of strategic plans.

A deal with Conrail to reach the New York market beyond Chicago followed.

Suffice it to say that after a decade of challenges, by the early 2000-2006 period, the J.B. Hunt team had captured the admiration of most railroad executives.

Some railroaders even wondered if the next step might involve a logistics trucking-based company making an M&A bid for control of a railroad.

But that didn’t happen.

Instead J.B. Hunt expanded its rail partnership tariff and premium service arrangement with other selected carriers, including Norfolk Southern (NS).

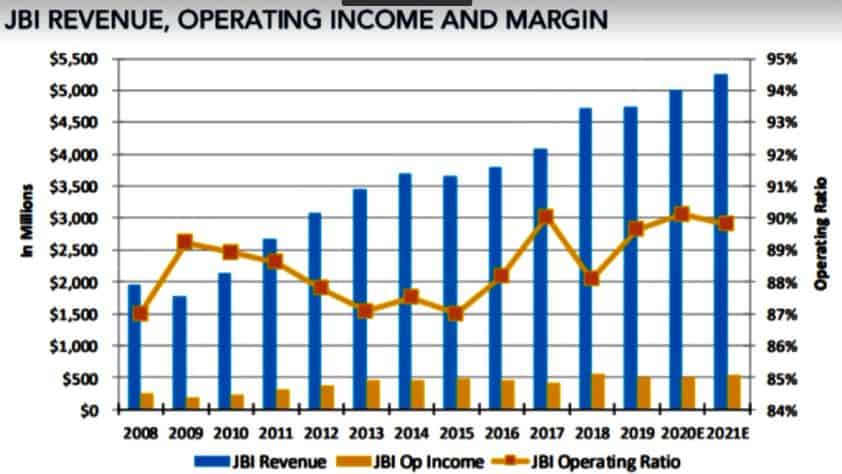

Here is a look at J.B. Hunt’s key intermodal financials between 2008 and 2019. The graph also shows management’s pre-COVID outlook toward uninterrupted growth into 2021.

COVID-19 events disrupted that forecast in March 2020 and out into the second quarter.

But like the trucking industry, J.B. Hunt’s intermodal business volume has been recovering from the downturn months into the third quarter.

What’s J.B. Hunt’s uniqueness?

The answer is found in this business case checklist. The company:

☑️ Positioned itself to serve all 50-states.

☑️ Provides its standard 53-ft big boxes for each customer.

☑️ Provides all GPS, billing and supply chain intelligence to its shippers.

☑️ Tries to provide its own managed local truck drayage.

☑️ Is focused on growth, not simply internal profitability.

☑️ Offers long-term solutions.

☑️ Provides more domestic containers than anybody.

To this observer, J.B. Hunt provides customers with more than just train rides.

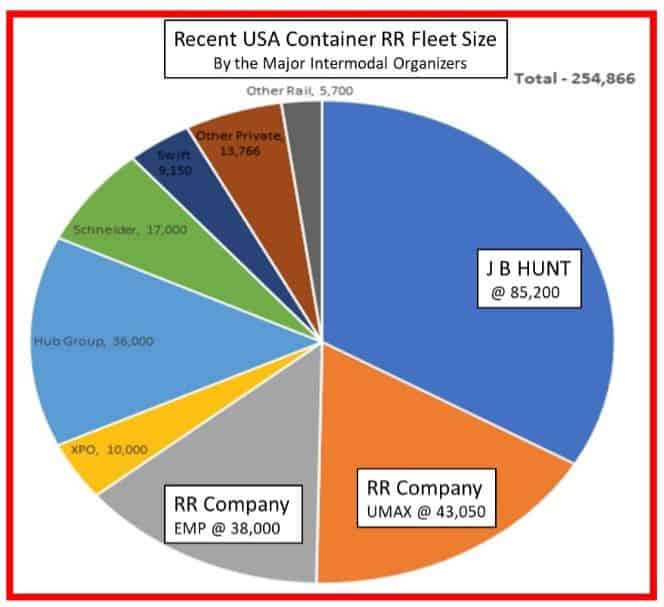

This graph of a recent U.S. container rail fleet shows just how dominant J.B. Hunt is. Its container fleet alone exceeds that of the two largest railroad carrier company — UMEX and EMP — fleets.

J.B. Hunt also diversifies its container intermodality by offering direct trucking, final-mile and other logistical services. It is more than just a train operation.

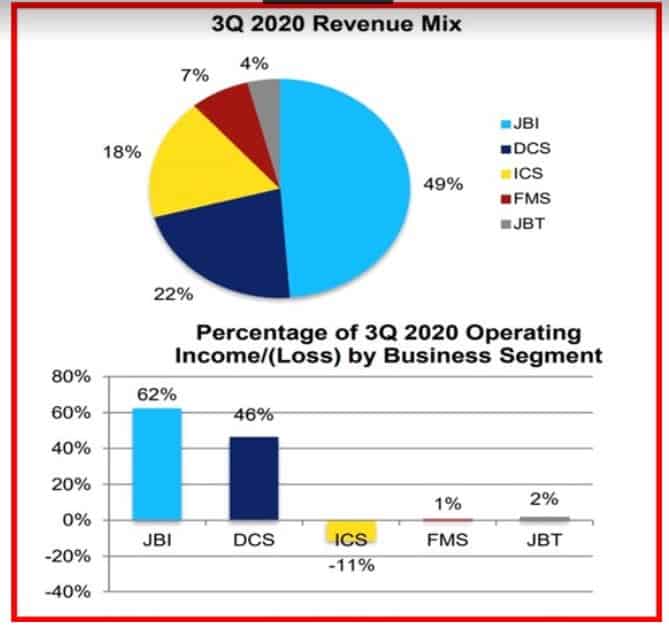

Here is J.B. Hunt’s 2020 Business Division report by revenue and operating margin.

The five sectors are:

1) JB Intermodal.

2) Dedicated Contract Services.

3) Integrated Solutions.

4) Final-Mile Services.

5) JB Trucking.

Intermodal is still its core business sector at over 50% of revenues and more than 60% of operating income.

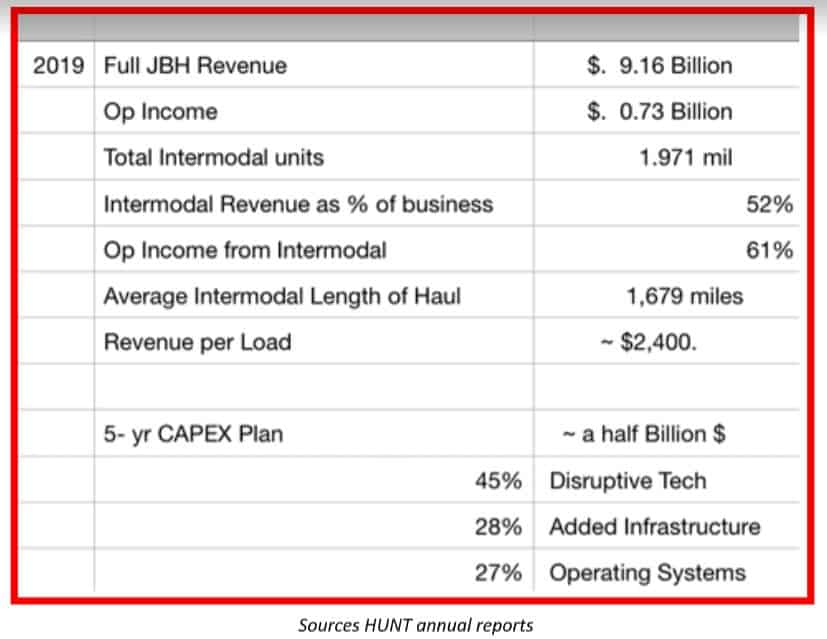

2020 is an obviously disruptive year. Therefore, in our lens, let’s examine the full-year 2019 description of J.B. Hunt’s key benchmarks.

Challenges into 2021

Business in 2021 will likely be impacted by a continuing COVID-19-related economy into the first half of the year.

Once past the viral impacts, J.B. Hunt still must find two growth markets.

One is short-haul intermodal in the less-than-600-mile range.

The second is discovering ways to capture a significant share of the private semi-trailer highway movements. Converting to containers plus chassis is sometimes cumbersome for the semi-trailer segment.

Out toward 2025, which of the big seven railroad companies has a volume growth strategic plan to sync with J.B. Hunt?

What’s your answer?

Sources fact-checked for this report are from IANA, AAR, Larry Gross Consulting, SFG, Ron Sucik Associates, and J.B. Hunt quarterly and annual reports.

Photos and graphs from selected PDF HUNT registered investor site https://www.jbhunt.com/shipment-solutions/shipment-services/refrigerated.html.

Josh Lake

Great article, Jim! I’d love to hear your thoughts on “ways to capture a significant share of the private semi-trailer highway movements.” What’s it going to take? Any startups or larger companies making headway here?

Matthew Andrade

I was curious how you would answer that really good question……..”Out toward 2025, which of the big seven railroad companies has a volume growth strategic plan to sync with J.B. Hunt?