Just when it looked like the airfreight market’s steady yearlong deflation had finally paused, it may have sprung a new leak.

Logistics professionals and freight analysts are hard-pressed to say whether freight patterns have normalized or will improve later this year, because there are so many conflicting economic signals and other variables impacting supply and demand.

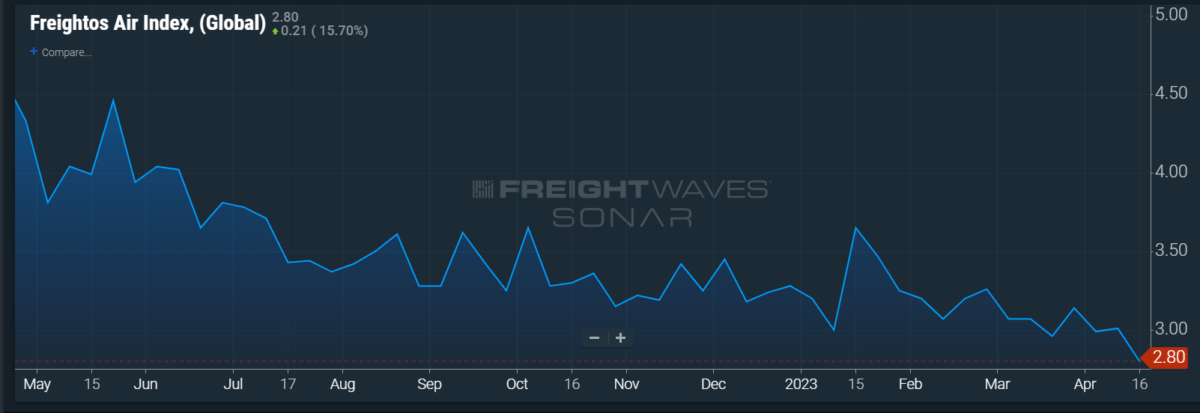

Preliminary data shows air shipping volumes and rates deteriorated faster in the first half of April than in recent weeks, potentially upsetting the narrative that the market has finally stabilized and will slowly gather steam for the busy fall shipping season that failed to materialize in 2022.

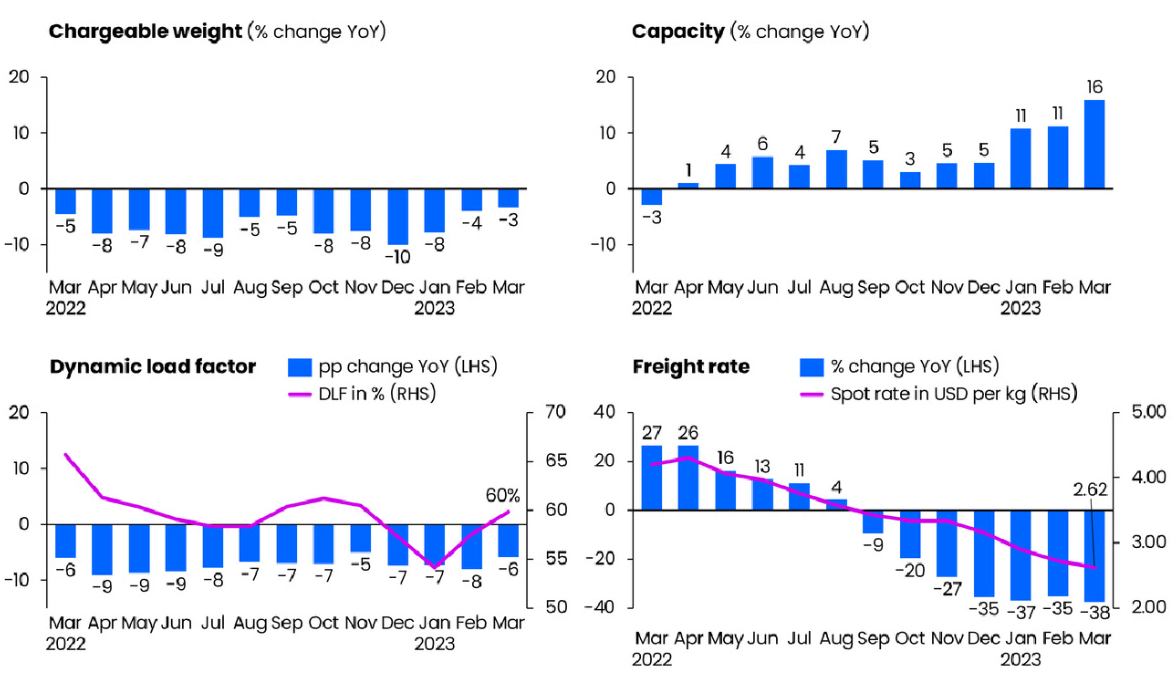

The previous two weeks have registered the sharpest drop in transported tonnage since the Chinese New Year factory closures in January. Sequential global demand dropped 8%, according to research firm WorldACD. North America shipment levels to Europe and Latin America were 12% lower than in late March. Year over year, volumes are down 11% compared to 8% in March. Analysis by Susquehanna Financial Group shows a similar downward change.

Meanwhile, global rates fell nearly 6% during the first week in April after modestly firming up and are down about 40% year over year, largely due to airlines passing on higher fuel and labor costs to customers. Rates for shipments into the U.S. from Asia at the end of March were 70% lower than a year ago, at about $3.30 per kilo, recent data from price reporting agencies shows. In Europe, rates from Asia are down more than 45% year over year and 20% since the end of February. Notably, the cost of shipping goods by air is still above pre-COVID levels.

The rate of negative, year-over-year growth had slowed from 10% in December to 3% in March, the lowest decline in 12 months, according to a monthly snapshot from market intelligence firm Xeneta.

The commodities that have declined the most in airfreight moving from Asia to the U.S. are computers, sweaters, phones, microphones and loudspeakers, clothing, and printer ink, said Jason Miller, the interim chairperson of Michigan State University’s Department of Supply Chain Management, on the latest episode of the Freight Buyers’ Club podcast.

Shipments of traditional personal computers fell 29% in the first quarter from a year ago due to weak demand, excess inventory and worsening macroeconomic conditions, said International Data Corp.

The pressure on rates is twofold: Demand is down at the same time capacity is rising as passenger airlines restore more international services following COVID closures. Xeneta said freight capacity increased 16% in March from the prior year. Those additional widebody flights carry much of the world’s cargo and are reducing the need for some freighters. Available space for cargo is now 1% greater than at this time in 2019, before COVID upset the global economy, and is significantly higher (up 10%) in the trans-Pacific trade lane to the U.S., according to Seabury Consulting.

American Airlines’ (NASDAQ: AAL) summer schedule, for example, has more than 400 extra widebody flights per month compared to last year, with new services and increased frequencies between its U.S. hubs and major European cities, as well as Tokyo, Sydney and Santiago, Chile. In July alone, American will operate more than 4,100 widebody flights across the Atlantic Ocean.

Europe-North America rates ticked down 4% last month to $2.61 per kilo, down from $3 at the start of the year, according to digital booking platform Freightos, and an influx of new capacity is likely to push rates down further.

Passenger belly capacity in Asia is expected to surge this quarter with the end of COVID travel restrictions. Seabury estimates lower-deck capacity between Asia and the U.S. will increase 44% year over year this summer and 60% by the end of the year, with trans-Atlantic belly capacity above 2019 levels.

Load factors, a measure of how much cabin space is filled with cargo, were down six to eight points in March from last year, Xeneta said.

United Airlines (NASDAQ: UAL) posted first quarter earnings this week that showed a 37% drop in cargo revenue versus the same 2022 period, largely due to the steep fall in average yield.

Seasonally adjusted flight activity for freighter aircraft declined 4.8% in March – the steepest decline in two years, said Fadi Chamoun, BMO Capital Markets’ transportation analyst, in a client note.

The International Air Transport Association releases figures each month that lag those of the private data providers and are calculated differently. Its report tends to confirm the more current observations about the market’s direction. The latest version said global traffic fell 7.5% in February versus 2022 — half the rate of decline in each of the previous two months — underscoring the first quarter’s improvement before air logistics operators hit the recent turbulence in demand. International bellyhold capacity increased to 75% of the pre-pandemic level. Xeneta, by comparison, previously reported February volumes were 4% lower than the previous year.

IATA said February demand, measured in cargo tons flown, is 2.9% ahead of the 2019 level.

A growing school of thought within the air logistics sector is that freight rates are artificially lower than pure supply and demand would dictate because airlines have consciously chosen to operate more aircraft than necessary so that they are ready for the next upcycle.

“In the short term, airlines are willing to price irrationally, even below their cash cost to operate the flight, because they want to maintain their schedule and weather through any short-term fluctuations,” said Neel Jones Shah, executive vice president of air strategy and carrier development at Flexport, on a recent company webcast.

Rational behavior will prevail over the medium term with ongoing cost pressures from jet fuel, richer labor contracts for pilots and airport service providers, “which is why I believe airfreight rates will stabilize 35% to 50% higher than 2019 levels,” or about $2.60 to $2.70 per kilogram, the former cargo chief at Delta Air Lines said.

Timing the restocking cycle

The latest pothole for air carriers comes amid growing cracks in the industry consensus that traffic will rebound in the second half of the year as retailers finally resume large orders with overseas suppliers after focusing on clearing excess inventories. Companies like Walmart, Target and Kohl’s have mostly corrected stock levels, but executives have indicated they are more cautious about purchasing activity because of ongoing concerns about inflation dampening consumer confidence and purchasing power.

U.S. retail sales last month dipped 1%, the second straight monthly decrease, according to the Commerce Department.

Leisurewear merchandiser Lululemon is continuing to reduce inventory growth and expects to realize “significant” gains in gross margin by using less airfreight this year, CFO Meaghan Frank said on a March 28 quarterly earnings briefing.

Meanwhile, home improvement stores like Home Depot are still plagued by higher inventory-to-sales ratios than normal, while apparel wholesalers like Nike are taking 23% longer to turn inventory than in 2019, said Miller.

Executives at STG Logistics and J.B. Hunt Transport Services have also voiced skepticism about a strong second-half inventory restocking in the U.S. But even a mild increase in orders would create some semblance of peak season for airfreight, according to Stifel logistics analyst Bruce Chan.

What’s confounding for business planners is the number of conflicting signals suggesting the global economy could head up or down.

The overall U.S. economy is not showing real signs of tipping into a recession, despite the Federal Reserve’s high interest rate policy to cool inflation. The Federal Reserve Bank of Atlanta forecasts that first-quarter gross domestic product will be 2.5%. Consumer inflation continues to moderate, unemployment is at historic lows, credit card delinquency rates are still below pre-COVID levels, wage growth is strong and the industrial sector is doing well.

The National Retail Federation reported ocean imports for March were down nearly 30% but forecasts container volumes will improve each month leading up to the peak season. The problem for airfreight, however, is that much of that new demand is likely headed to ocean carriers that have huge amounts of empty space to sell and rock-bottom rates once again in the absence of port bottlenecks.

In fact, the normalization of ocean trade and lack of wait times is even causing “air-to-ocean conversions where traditional air shippers are turning a percentage of their supply chain to fast-boat services on the ocean to diversify and save some money,” said Jones Shah.

Globally, China is now open for business after lifting restrictive COVID containment policies in December, and the country’s export production is growing again. Goods trade is declining at a slower rate, inflation in G7 countries declined three-tenths of a point in February and energy prices have dropped since last year. But manufacturing in major developed economies continues to contract.

Adding to the uncertainty is how the Ukraine war will play out, as well as geopolitical tensions in the South China Sea between China and Taiwan.

Despite the deceleration in air freight demand over the past year, global freighter flight activity remains 14.7% higher than in 2019, which suggests the potential for further downside movement, Chamoun said.

“I think we’ll see for the general merchandisers more of a traditional peak season this year, albeit it’s going to be a cautious one. But I’m not looking for Asia to the U.S., either ocean or air, for it to be that great of a year because we’re still over-inventoried and there’s a lot of caution out there,” said Michigan State’s Miller. “2023 is the hangover from the 2021 party.”

The perception of the air cargo market hitting bottom appears to be why more forwarders are inking longer-term contracts with shippers again, Xeneta said in its report.

Prior to COVID, about one-third of air shipments were booked based on immediate, one-time quotes and the rest were under longer-term contracts. Since COVID, the share of freight volume moving in the spot market has been higher than 45%. The nascent sense of more market certainty resulted in six-month agreements for guaranteed blocks of space rising to 36% in the first quarter from 23% during the final three months of 2024 as forwarders sought to lock in customers for a longer period.

“I think we’re seeing signs that some forwarders are willing to take a little more risk on what airfreight rates might do because they don’t expect the market to drop much further. Everybody wants to achieve growth, but if the market is not growing, you have to grab a share from someone else,” said Niall van de Wouw, Xeneta’s chief airfreight officer.

And even though spot rates are very low at the moment, many shippers would rather agree on a reasonable price once rather than spending precious resources renegotiating every week or month, he added.

Click here for more FreightWaves and American Shipper articles by Eric Kulisch.

Sign up for the weekly American Shipper Air newsletter here.