The 2024 survey of the top issues in trucking, undertaken each year by the American Transportation Research Institute, once again finds that what drivers think are the big issues aren’t the same as those of the industry as a whole.

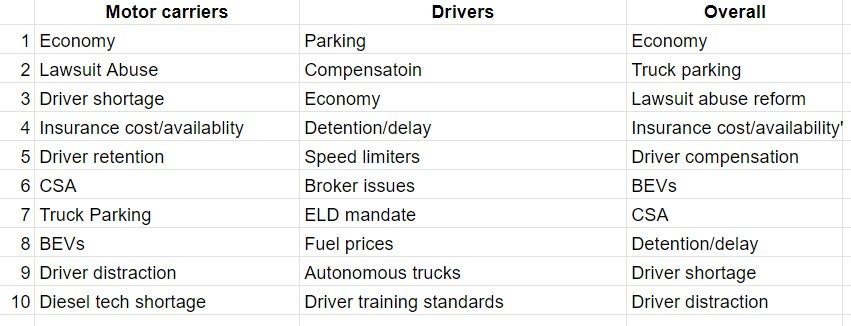

Laying the results of what drivers say are the key issues in trucking against the results of the overall survey – in which driver submissions are part of the final ranking – shows that in 2024, only two issues made it on both the overall top 10 lists and the top 10 list for drivers: truck parking and the state of the economy.

ATRI is the research arm of the American Trucking Associations. The results were revealed at the group’s annual meeting in Nashville, Tennessee.

Only the economy was closely ranked by both the overall respondents and the driver survey: It was at No. 1 and No. 3, respectively.

The issue of parking was on the top for drivers but seventh overall.

The final results of the survey are compiled in a complex weighting process that takes into account the submissions of motor carrier company respondents, drivers and “other industry stakeholders.”

The end result, therefore, can reflect high scores from the driver survey on issues that don’t show up on the top 10 list of motor carrier respondents. This year, there were two issues that weren’t on the motor carrier list but which made the top 10 on the strength of driver concerns: driver compensation and detention/delay issues.

The motor carrier group constituted 45.9% of all respondents, and the industry stakeholders were an additional 22.8%. That leaves drivers at 31.3%.

The ATRI methodology, as explained by the group, incorporates various weighting factors. An issue that comes in as particularly important to a group of respondents will carry greater weight in the final rankings than other votes.

Besides parking at No. 1 and the economy at No. 3, the other issues that were most important to drivers were:

- No. 2 – driver compensation.

- No. 4 – detention/delay at customer facilities.

- No. 5 – speed limiters.

- No. 6 – broker issues.

- No. 7 – the ELD mandate, which went into full effect in December 2019 and is not under consideration for repeal.

- No. 8 – fuel prices, which last year was No. 2 on the list for drivers.

- No. 9 – autonomous trucks.

- No. 10 – driver training standards.

Laying that list up against the motor carrier response shows the sharp divide.

Besides the economy at No. 1 and parking at No. 7, motor carriers’ key issues were:

- No. 2 – lawsuit abuse reform.

- No. 3 – driver shortage.

- No. 4 – insurance cost/availability.

- No. 5 – driver retention.

- No. 6 – compliance, safety and accountability (CSA) scoring.

- No. 8 – battery electric vehicles.

- No. 9 – driver distraction.

- No. 10 – diesel technician shortage.

The combined responses result in the following top 10 list:

- Economy.

- Truck parking.

- Lawsuit abuse reform.

- Insurance cost/availability.

- Driver compensation.

- Battery electric vehicles.

- CSA.

- Detention/delay.

- Driver shortage.

- Driver distraction.

Comparisons between the biggest issues of 2023 and 2024, whether for motor carriers or drivers, reflect some changes in the industry, but not a large number. The top 10 lists for the two groups did not significantly change over the course of 12 months.

- In 2023, fuel prices were fifth for motor carriers and third for drivers. That issue did not make it into the top 10 for carriers this year and fell to eighth for drivers. The Department of Energy/Energy Information Administration weekly retail diesel price in September 2023, which is when that survey was conducted, was about $4.56 a gallon. A year later, in September 2024, it was almost exactly $1 less, at $3.577.

- A driver shortage was third for motor carriers this year and second last year. While there is no one data point in the market that is considered a barometer of driver availability, comments made on the second-quarter earnings call for Ryder System (NYSE: R) suggested that for Ryder at least, driver availability is loosening. On the call, CFO John Diez said Ryder’s Dedicated segment, which provides transportation to clients, “continued to benefit from favorable driver conditions as the number of open positions and time to fill for our professional drivers continue to improve.”

- Fuel prices in 2024 were fifth for independent owner-operators but not in the top five for company drivers. (ATRI only provided the top five rankings for the company versus owner-operator comparison). That isn’t surprising; fuel consumed by company drivers is paid for by the employer, but independent owner-operators pay for it themselves and need to be sure to secure freight rates that adequately compensate them for fuel usage.

Each of the 10 points for the survey’s overall score came with a suggested list of policy options that might help deal with the stated issue, drawn from respondent suggestions.

For truck parking, the suggestions were for the industry to push for a “dedicated federal funding program to increase truck parking capacity at freight-critical locations; lobby local governments to reduce regulatory hurdles to build new parking or expand existing sites; and support state applications to the Department of Transportation for grants to expand parking.”

More articles by John Kingston

E2open stock price plunges after earnings report; strategic review ‘ongoing’

OOIDA, Truckstop team up; load board is now group’s ‘exclusive’ partner

NFI’s Brown seeks dismissal of New Jersey case, cites minor role in dispute