As Deutsche Bank analyst Amit Mehrotra told American Shipper back in March, “You ain’t seen nothing yet.” He was right. The latest data reveals that despite a deluge of inbound cargo since the second half of last year, import demand is not abating — it’s increasing.

Importers are still playing catch-up. The Institute for Supply Management (ISM) Customers Inventories Index, released Monday, dropped to 28.4 for April. That set a new record for the lowest number since the index was created in 1997 and is down 34% from April 2019, pre-COVID.

As one retail survey respondent told the ISM, “Market capacity in most areas is oversold, with no realistic improvement on the horizon. In fact, it appears that demand will continue to strengthen, leading to more significant disruptions.”

The Census Bureau’s retail inventory-to-sales ratio in February was down to 1.23, 18% below the March 2019 number and the second lowest ratio ever (after this January’s). The next Census Bureau release is in mid-May. Asked whether the latest ISM inventory index drop implies a further fall for the Census Bureau retail inventory-to-sales ratio, Mehrotra responded, “I think that’s a safe bet!”

Customs data tells import story

Customs data reveals the curve of the import boom to date.

FreightWaves’ SONAR platform collects data on the daily number of customs filings for maritime imports (seven-day trailing average), irrespective of the volume per shipment (SONAR: CSTM.USA).

The numbers show imports surging past 2020 levels in the first three months of this year; in the first quarter of last year, imports were depressed by COVID. In late April and early May 2020, imports spiked as cargoes delayed by the initial Wuhan lockdown belatedly arrived. Even so, this year’s imports stayed roughly on par with last year’s huge post-Wuhan-lockdown surge.

The next three months should see strong gains year on year, given that 2020 imports in May, June and early July were depressed by U.S. lockdowns and as carriers “blanked” (canceled) trans-Pacific sailings. The question ahead is whether 2021 imports will keep pace with gains seen last year in September-December. The growing consensus is that they will.

In fact, the customs shipments numbers may undercount import growth. A separate FreightWaves SONAR dataset shows that inbound bookings measured in twenty-foot-equivalent units (TEUs) broke from historical norms and began rising more steeply than the number of import shipments starting last May. This suggests that, on average, importers have been increasing the number of TEUs per customs filing.

Bookings data shows what’s to come

FreightWaves’ SONAR platform features a proprietary index of shippers’ ocean bookings (SONAR: IOTI.USA). Bookings to the U.S. are measured in TEUs (10-day-moving-average) as of the scheduled date of overseas departure and indexed to January 2019.

While these are bookings, not loadings, the current index indicates the likely level of U.S. imports later this month and in June, as departing ships arrive at American shores. The forward data for bookings due to depart from all destinations to the U.S. shows a new all-time high will be set next week. The index has continued to climb since mid-May 2020.

The index of import bookings from China (ITOTI.CHNUSA) follows the same upward pattern, with a new all-time record to be set later this week.

Could port volumes increase further?

With ships and container equipment capacity effectively maxed out, the question for U.S. ports is whether already record-high import volumes have any room to increase. According to Nerijus Poskus, vice president of global ocean at freight forwarder Flexport, they do.

It is currently week 18 of the year. Poskus told American Shipper that in weeks 16-18, 20% of Asia-East Coast sailings, 23% of the Pacific Northwest sailings and 16% of California sailings were blanked for operational reasons — because liners didn’t have the ships to service them due to congestion.

“The tiny bit of good news [for shippers] is that this capacity should slowly come back to the market in June, because the congestion situation is getting slightly better,” he said.

As of Tuesday, 19 container ships were at anchor off Los Angeles/Long Beach, down from a daily average of around 30 earlier this year. The decrease is not due to lower import demand, but rather, to lines diverting sailings to Oakland and Tacoma, Washington, as well as the blank sailings. “As the port congestion situation improves [and blank sailings reduce], I do think this will allow actual loaded TEUs on the trans-Pacific to increase about 15-20% June and July,” said Poskus.

That may be welcome news for shippers looking for slots, but not so welcome news for U.S. ports hoping for a breather so their terminals can be cleared before the traditional July-October peak season ensues.

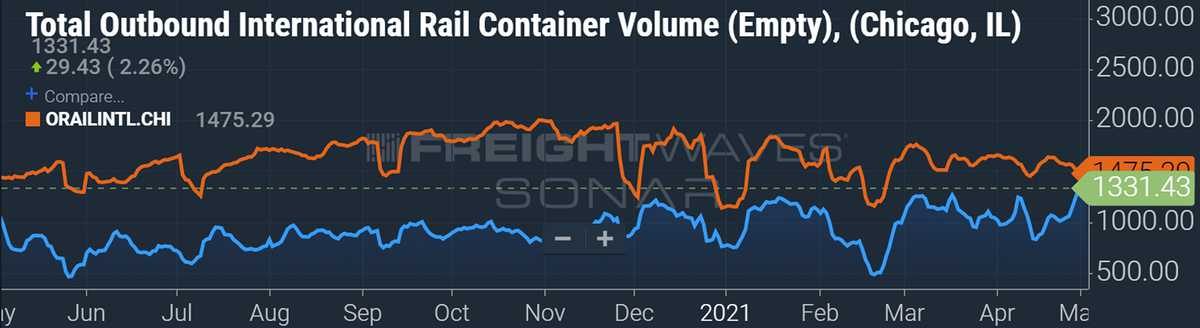

Rail data reveals scramble for empties

Meanwhile, liners’ rush to get empty containers back to Asia to fill with import cargo — a strong indicator of forward import demand — is becoming increasingly apparent in rail data.

Until this year, loaded inbound rail containers to Los Angeles/Long Beach, including 20-, 40- and 45-foot units (SONAR: IRAILINTL.LAX), have been around double the volume of empty rail containers arriving at the Southern California ports (SONAR: IRAILINTE.LAX), according to proprietary data.

But that dynamic has now reversed. As of Sunday, inbound empties were 42% higher than inbound loaded rail containers.

There’s a similarly unusual pattern with outbound rail containers from Chicago. While the number of loaded boxes (SONAR: ORAILINTL.CHI) is still higher than empties (SONAR: ORAILINTE.CHI), the gap has dramatically narrowed and it appears empties could soon overtake loaded outbound volumes.

Looking at the year-on-year change, empties on rail out of Chicago are up 27%, with loaded outbound rail containers up only 3%.

Trans-Pacific spot rates may go higher

Given current market chaos, it’s no surprise that spot trans-Pacific freight rates remain at peak levels. “I think [freight] prices will actually keep rising,” predicted Poskus.

The global composite of the Freightos Baltic Daily Index (SONAR: FBXD.GLBL) hit a new all-time high on Monday and is up 208% year on year. The Asia-West Coast index (SONAR: FBXD.CNAW) is up 210% and the Asia-East Coast index (SONAR: FBXD.CNAE) 144%.

Click for more articles by Greg Miller

Related articles:

- Flexport: Trans-Pacific deteriorating, brace for shipping ‘tsunami’

- ‘March madness’ at LA port amid ‘once in a lifetime’ surge

- Demand boom on collision course with ocean transport ceiling

- ZIM: US importers buckle, sign contracts early, pay 50% more

- Deutsche Bank on import bonanza: ‘You ain’t seen nothing yet’

- Ocean carriers hold all the cards in contract talks with shippers