“The market has spoken: Coal is dying” declared a September 2019 headline in CNN Business, after China announced it would cease funding overseas coal projects. “Coal is dead. Power to the people!” activist group 350.org triumphantly tweeted.

These predictions have not aged well. Bulk cargo vessels full of coal crisscross the oceans. Storage areas are so full of coal near ports in the Netherlands and Belgium that iron ore storage space is being commandeered.

China’s production in the first half of 2022 rose 10% year on year. The Chinese government approved billions in new domestic mining investments. The Indian government granted its mines the right to expand production by up to 50% without obtaining new permits. Indonesia, the world’s largest exporter, is also hiking production.

Germany is creating a new coal reserve to secure supply and has delayed the closedown of several coal-fired plants. The U.K., Poland, Italy, Greece, Poland, the Czech Republic and Romania have also delayed closures of coal-fired plants.

South Korea has suspended coal-plant load restrictions. France may restart one of its coal-fired plants this winter. Japan will start up one in August. China is building multiple new coal-fired power plants.

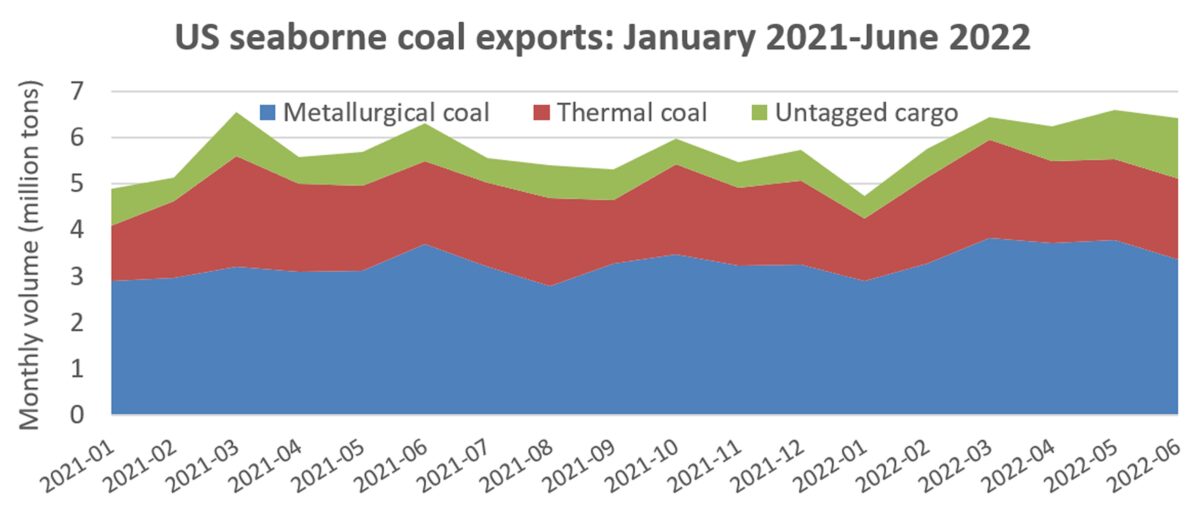

Among those that stand to benefit: U.S. mining companies exporting coal and international owners of dry bulk carriers.

Trade flow drivers

Two big variables will affect shipping patterns in the second half.

First, the Ukraine-Russia war: how it impacts supply and pricing of liquefied natural gas, which competes with thermal coal for power production, and how the EU ban on Russian coal starting Aug. 10 changes trade flows.

Second, what happens with China and India, the two largest buyers. Will China offset economic hits from COVID lockdowns and property developer debt by subsidizing projects that boost steel production? Will China’s government remove its unofficial ban on imports of Australian coal?

War and looming EU import ban

Russia is the world’s third-largest supplier, behind Indonesia and Australia.

Shipbroker Braemar said that “several utilities in Europe started avoiding [imports from Russia] almost immediately in March.” Overall, however, EU imports of Russian coal stayed relatively strong through May, then dropped in June.

Soon after the war broke out, EU buyers ramped up purchases from sources outside of Russia: the U.S., Australia, Colombia, South Africa and Indonesia.

According to shipbroker BRS, Europe bought 44 million tons from these five countries in all of 2021. It had already bought 41 million tons from these countries in the first half of 2022, led by 14 million tons from the U.S. and almost 13 million tons from Australia.

The EU “has been sourcing the maximum coal from the U.S,” said BRS.

U.S. exports — including both thermal and metallurgical or “met” coal (used for steel production) — totaled 36.2 million tons in the first half, up 6% year on year, according to data from Kpler.

India and China step in

The wartime coal trade is following the same pattern as the wartime oil trade. Russian volumes that formerly went to Western buyers are going to China and India instead. Other suppliers are replacing Russian volumes.

“In June, 2.7 million tons of coal was lifted on bulk carriers from Russia to India, by far the largest monthly total on record,” reported Braemar.

“India has shown a clear willingness to buy Russian coal. And given the heavy discounts it will achieve compared to other suppliers, we expect this to continue and likely continue to increase.”

Russia’s shift in sales toward India and China will change demand for different bulker size categories, according to Braemar. Smaller Handysizes (bulkers with capacity of up to 35,000 deadweight tons) saw strong coal shipments in the first half, accounting for 8.8% of total volume. Of that, 49% of Handysize coal loadings were in Russia, for delivery to the EU in the east and Japan in the west.

“The Handysize coal trade will continue at reduced levels,” predicted Braemar. “We believe the majority [of Russian volume] will head east to India and China on the larger vessels.”

Indian and Chinese coal demand

According to BRS statistics, China bought 284.2 million tons of seaborne coal in the first half of the year. India imported 195.1 million tons.

Braemar pointed to a “share rise in Indian coal demand as power stations replenish inventories. India experienced widespread power outages in April and May, when the easing of COVID lockdowns and a severe heat wave led to a surge in power demand.” Power usage pulled back this month as rain during the monsoon season brought “a respite from the heat,” said Braemar. That relief should end in August.

The big unknown on the demand side is China.

Since high-profile blackouts last year, China has increased consumption of thermal coal but has relied heavily on domestic supplies.

Chinese steel production — which drives demand for imported met coal and iron ore — fell 3.4% in the first half of 2022 versus the year before, according to data from WorldSteel. BRS expects Chinese steel production to continue to slide through the second half as the country undergoes a “painful contraction” of its economy.

Will China resuming buying Australian coal?

China used to be a heavy buyer of Australian coal, until a diplomatic spat led to an unofficial ban on imports from Australia beginning in October 2020. After the ban, China replaced Australian cargo with supplies from Indonesia and Russia; Australia replaced Chinese sales with shipments to Japan, India, South Korea, Taiwan and Europe.

There are now reports that China may soon end the ban on Australian thermal and met coal.

According to Pranay Shukla, associate director at S&P Global Market Intelligence, the impending EU ban on Russian coal has led to “an expectation of strong flows [of Australian coal] into Europe in the second half, which is expected to continue thereafter.”

“If mainland China lifts the Australian coal import restrictions, Europe would need to source more from the U.S., Colombia, Mozambique,” said Shukla.

BRS doesn’t agree. It pointed out that Australian thermal coal prices are now more than double domestic Chinese prices. “Easing the ban doesn’t make much difference unless the imported price of the Aussie coal comes to the competitive level to procure,” it said.

However, the easing of the ban could lead to flows of Australian met coal to China, said Argus Media. It noted that the price of Chinese domestic met coal is over 60% higher than Australian met coal.

As with all ocean commodity markets, what happens in one trade ripples through others. If Australia has less met coal available for European steel producers because it’s selling to China again, met coal exporters in America would have more opportunities to sell to Europe after the EU ban on Russian coal enters force.

Click for more articles by Greg Miller