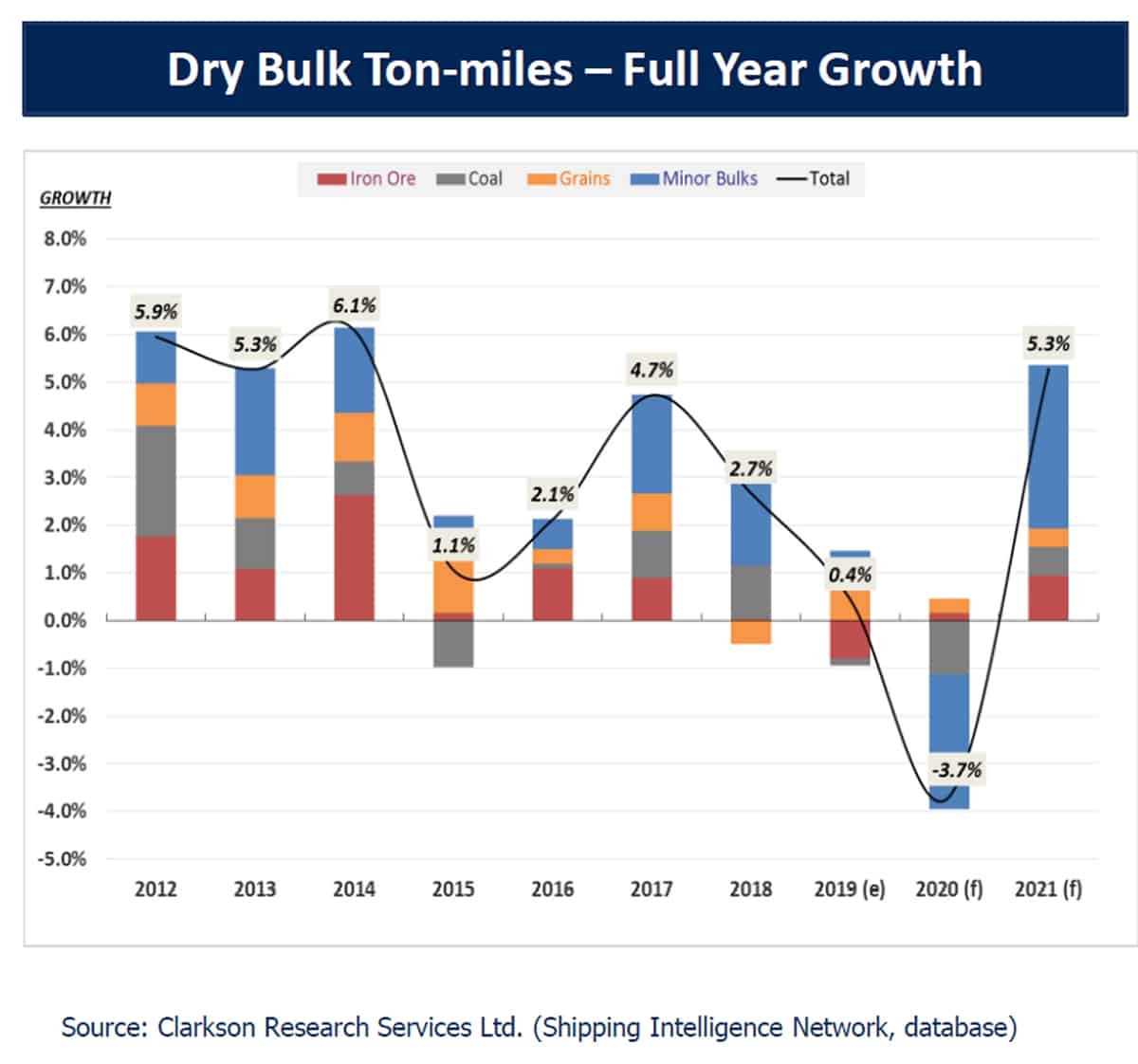

Once upon a time, believe it or not, stock investors were obsessed with dry bulk shipping. A repeat of such seemingly Bizarro World behavior could be a long way off.

Rates for Capesize bulkers (vessels with capacity of around 180,000 deadweight tons) fell yet again on Wednesday, to $3,796 per day, according to the Baltic Exchange’s 5TC index. The tentative bounce beginning in late April has long since fizzled. Futures markets currently put the full-year 2021 average rate at $11,900 per day, still below breakeven for many operators.

The two largest U.S.-listed Capesize owners — Star Bulk (NASDAQ: SBLK) and Golden Ocean (NASDAQ: GOGL) — reported quarterly results on Wednesday and saw their stock prices fall by 2% and 4% respectively on a day when the Dow rose by over 500 points.

Breakwave Advisors, the developer of the Breakwave Dry Bulk ETF (NYSE: BDRY), noted in its latest sector report that “Capesize spot rates have never been lower for this time of the year” and are currently at “unsustainable levels.”

Golden Ocean CEO Ulrik Andersen said on the conference call with analysts, “Shipping is certainly no stranger to rapid changes, but the COVID pandemic has changed the world and shipping rapidly, perhaps forever. In the past few months, we’ve witnessed an unprecedented crisis that has hit us with tremendous force.” He added, “You cannot say ‘Q1’ without saying ‘COVID.’”

The Vale factor

Actually, in the dry bulk sector, you cannot say Q1, or for that matter, Q2, without saying “Vale” (NYSE: VALE). Brazilian iron-ore exports on the long-haul trade to China are the largest driver of Capesize spot rates and Brazilian iron-ore mining giant Vale has dramatically and persistently underperformed.

“The fact that Brazil is experiencing serious issues with its iron-ore exports is having a profound impact on global iron-ore supply,” said Breakwave Advisors.

Pointing to new greenfield projects in West Africa and capacity increases out of Australia, Breakwave Advisors added, “One wonders whether [they] reflect a loss of confidence in the ability of Vale to deliver on its growth promises, not only for this year but on their long-term stated targets. Even during normal times, the company has been unable to meet its production goals.”

And these are not normal times — which could potentially make matters much worse. Coronavirus cases are now spiking in Brazil, where the right-wing president, Jair Bolsonaro, has actively discouraged social distancing. Brazil now has over 391,000 cases, second only to the U.S., and over 24,500 confirmed deaths.

If the coronavirus were to temporarily impede Vale mining and/or port operations, it would send shockwaves through the Capesize sector, given that replacement cargoes to China from mines in Australia would sail a third the distance.

Chinese stimulus: wishful thinking?

The hope within beleaguered dry bulk circles is that China will come to the rescue, as it did in the wake of the 2009 financial crisis, with a massive infrastructure program. According to this view, China will pour vast sums into the construction of more buildings, highways and bridges in an effort to resuscitate its own economy; more infrastructure would equate to more steel production, thus more demand for coal and iron ore to produce the steel, thus more dry bulk shipping demand. Problem solved.

The counterargument to the Chinese stimulus theory is that the country does not need the same scale of infrastructure development it did in 2009, given what was already built in the prior cycle as well as the shift in the economy from basic manufacturing toward more technology and consumer consumption, and China would be wiser to put more stimulus money toward technology development and customer spending, neither of which requires steel.

Few concrete details are available on $667 million in new bonds announced by the Chinese government last week. Both Star Bulk CEO Petros Pappas and Golden Ocean’s Andersen pointed to China’s announcement on their respective calls, with the latter asserting, “Undoubtedly, this will have a positive effect on steel demand when the infrastructure plans are sanctioned.”

Stifel analyst Ben Nolan said in a research note on Star Bulk, “The dry bulk market has been terrible due to the coronavirus … [but] should stimulus translate into infrastructure spending, dry bulk demand could recover quickly.”

Weak quarterly results

Golden Ocean reported a net loss of $160.8 million for the first quarter of 2020 compared to a loss of $7.5 million in the same period last year. Excluding noncash charges of $125.6 million (mainly due to impairments on leased vessels), Golden Ocean posted an adjusted net loss of 20 cents per share, in line with consensus.

Star Bulk reported net income of $2.8 million for the first quarter of 2020 compared to a loss of $5.2 million in the same period last year. However, excluding noncash items such as mark-to-market derivatives gains, Star Bulk posted an adjusted net loss of $22.2 million or 23 cents per share, significantly worse than the adjusted loss of 6 cents per share that analysts expected.

Star Bulk’s fleet earned an average of $10,949 per day in the first quarter of 2020, down from $11,192 per day the year before. Click for more FreightWaves/American Shipper articles by Greg Miller