Following scrutiny from an activist investor group, which includes the company’s founder and former CFO, management at asset-light trucking and logistics company Forward Air (NASDAQ: FWRD) doubled down on its approach to the business during its fourth-quarter call with analysts Friday.

The investor group led by Ancora Advisors issued an open letter to shareholders Wednesday, voicing discontent with the current direction of the company and announcing its decision to nominate four candidates for election to the board. The letter followed weeks of dialogue between investors and the board, which were unable to reach an agreement.

At the core, the group has concerns with Forward’s capital allocation strategy, which has continued to diversify beyond the company’s legacy airport-to-airport expedited trucking offering. Specifically, the group believes investments and acquisitions in drayage and intermodal are driving margins and returns lower.

Forward’s core expedited less-than-truckload offering has seen operating ratios deteriorate, while competitors are seeing improvement. Also, returns on invested capital have been cut in half over the last five years. The group contends the diversification strategy is to blame.

The activist group now holds a 6.3% stake in the $2.2 billion company.

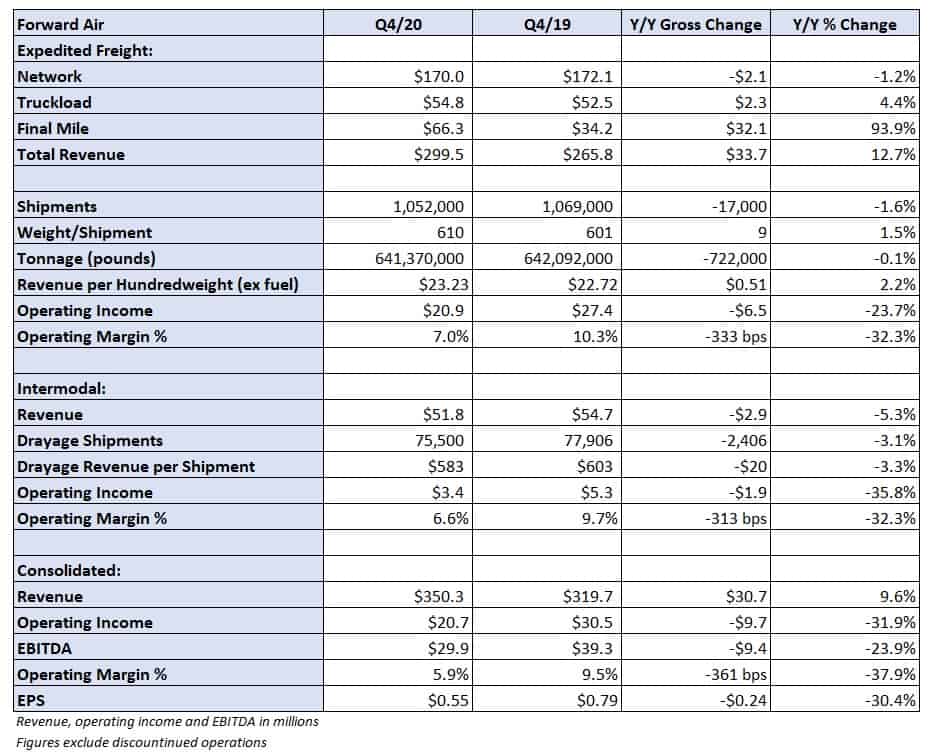

The Greeneville, Tennessee-based company reported earnings per share of 55 cents Thursday night, which included 19 cents per share in lost revenue and charges related to a cyberattack in December. Excluding the attack as well as an increased earnout related to an acquisition, earnings would have been ahead of the prior guidance range.

Forward announced the sale of its high-frequency pool distribution segment for $20 million, which includes a $8 million upfront payment with the remainder subject to an earnout. The deal is expected to close within the next two weeks.

Management doubles down

At the top of the call, Chairman, President and CEO Tom Schmitt said the company has kept pace with commitments previously laid out. The company has continued investing in its terminal infrastructure, expanded the LTL offering outside of the airport lanes, made additional acquisitions in final mile and intermodal and enhanced its mix to include better-priced freight.

Management believes that a “double-double” in revenue growth and margins can be achieved via its plan.

The company added six terminals last year and plans to add between eight and 10 in 2021. Forward’s network has nearly 100 final-mile facilities, some of which are in cities that don’t offer LTL service. The plan is to continue co-mingling modes throughout the network to improve density as some of the company’s core freight – trade shows, cruise lines and concerts – has fallen off during the pandemic.

The double-down approach also included another acquisition.

Forward announced Thursday that it acquired intermodal drayage provider Proficient Transport for $15 million. The Chicago-based outfit adds to Forward’s intermodal footprint in the Midwest and Southern markets. At $23 million in annual revenue and $3 million in earnings before interest, taxes, depreciation and amortization (EBITDA), Forward is now a top 10 provider of drayage in the U.S.

The deal was funded with cash on hand and is expected to close later this month.

2021 off to a strong start

Shipments were off slightly in the fourth quarter and tonnage was flat. Management said the first 10 weeks of the quarter were “an operational beat.” Then the attack hit.

In an earlier filing, the company disclosed January LTL tonnage was up 10.9% year-over-year with shipments up 14.4%. Management was adamant that the numbers are fair comparisons and don’t reflect a catch-up in shipments as systems came back online. The tight time commitments Forward operates under means that the freight opportunities it had at the time of the outage were truly lost to competitors.

Schmitt referred to 2021 as “boom times,” comparing the current market to 2018. He believes the normal seasonal lull around Chinese New Year is off the table this year due to a high-demand environment.

Reasons for the change of course

Management acknowledged the company had much higher margins and returns in the past when it was primarily an expedited trucking company moving airfreight. But they noted the LTL airfreight total addressable market has declined as some of its customers began insourcing transportation. Also, several new competitors showed up.

Management said the best path forward includes offering multiple modes throughout the network, pointing to synergies between truckload and LTL and between final mile and LTL. The goal is to get the expedited segment to a 10% or better margin. The division posted a 7% margin in the fourth quarter, but it was closer to 9% excluding the attack.

The expectation is that the traditional LTL offering can get to 15% margins. The tailwinds include a strong LTL market and the eventual return of freight related to events, which is heavier and has higher margins than the e-commerce shipments the company has been moving recently. The plan is ambitious as Forward wants to capture 10% of the $40 billion-plus LTL market. Expedited as a whole — LTL, TL and final mile — was slightly north of $1 billion last year.

Schmitt noted the final-mile segment is “on a tear.” To hit the overall margin goal, the division needs to sustain a 7% to 8% margin, which he said it is doing currently. It sounds like the truckload segment needs some work. The goal is to reach a 5% margin there.

Schmitt said the intermodal segment is producing a return well above the cost of capital, a point of contention with Ancora. During the quarter, the margin was 6.6%, 310 basis points worse year-over-year, but the division was also impacted by the outage. Schmitt referred to intermodal as a permanent “double-double” opportunity.

The big levers to hit the goal also included raising rates — the company announced a 6% general rate increase last week — and attempting to lower its purchased transportation expense line, which has spiked more recently as capacity tightened.

Shares of FWRD rallied back to flat late in the Friday session compared to the S&P 500, which was up slightly.