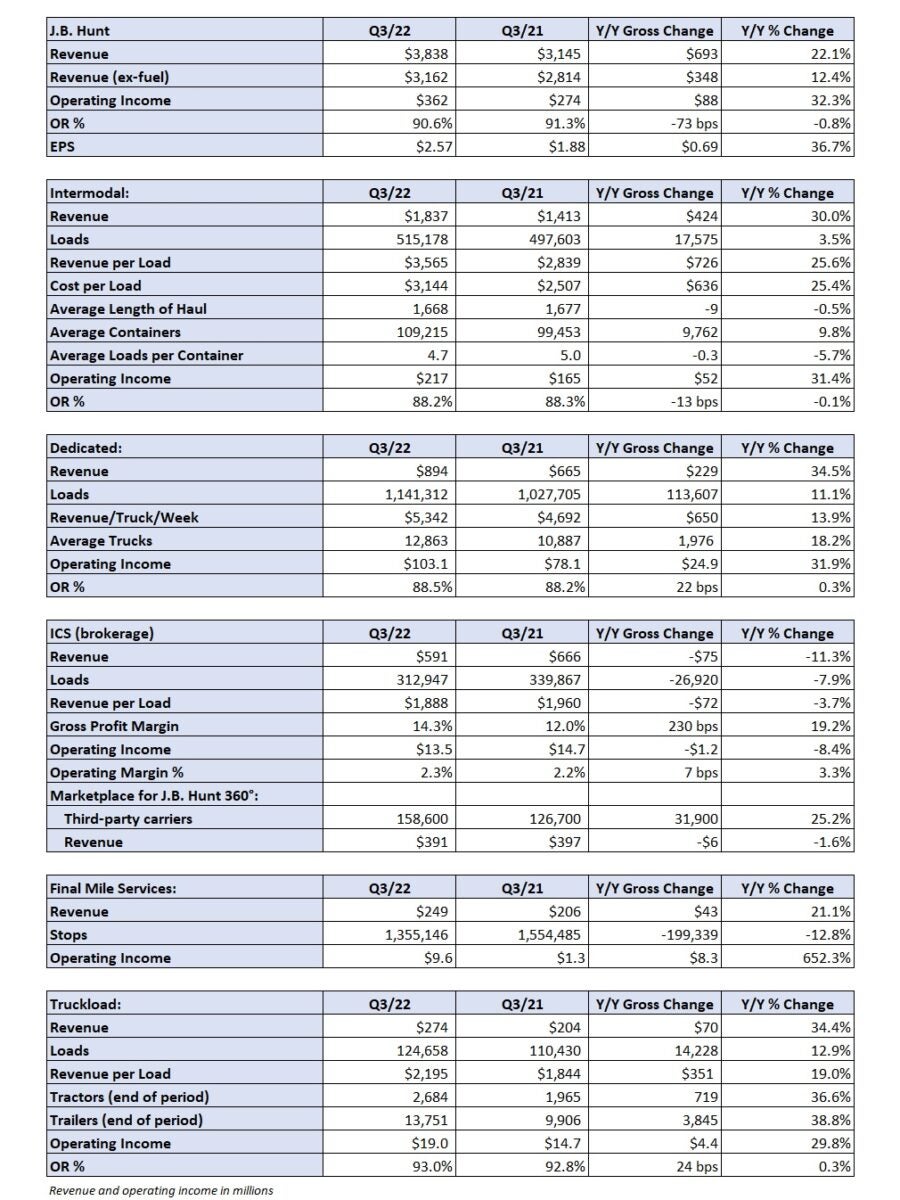

J.B. Hunt Transport Services beat third-quarter expectations Tuesday after the market closed, posting earnings per share of $2.57 compared to the consensus estimate of $2.45.

Consolidated revenue of $3.84 billion was 22% higher year over year (y/y) and slightly ahead of analysts’ expectations. Excluding fuel surcharges, revenue was up 12% y/y.

Revenue in J.B. Hunt’s (NASDAQ: JBHT) biggest segment, intermodal, increased 30% y/y to $1.84 billion. Revenue per load jumped 26% y/y, in part due to higher fuel prices, with loads up just 4% y/y but outpacing the rest of the industry. Overall intermodal container traffic on the U.S. Class I railroads during the quarter was down 1% y/y. Intermodal revenue per load was up 17% y/y excluding fuel.

Rail service continued to impede intermodal results, but improvement was seen by the end of the quarter, a news release stated.

“During the quarter, we continued to experience growth in demand for intermodal services, but volume was negatively impacted by rail velocity challenges, customer detention of equipment and overall supply chain uncertainties facing our customers,” the report read. “As the quarter progressed, rail velocity and service levels improved notably to the best levels experienced since early 2021.”

Average intermodal loads per container dropped to 4.7 in the period compared to 5 in both the second quarter and the 2021 third quarter. Operating income was up 31% y/y, with the operating ratio improving 10 basis points to 88.2%.

Dedicated revenue jumped 35% y/y to $894 million as the company grew revenue-producing truck counts in the segment by 18% y/y and revenue per truck per week by 14% y/y. Even with the new account and equipment additions, the dedicated operating ratio backed up just 20 bps y/y to 88.5%.

Brokerage revenue fell 11% y/y to $591 million. The combination of an 8% decline in loads and a 4% dip in revenue per load were the culprits. Gross margin improved 230 bps to 14.3%. Operating income was down $1.2 million y/y to $13.5 million as higher personnel costs, tech-related expenses and bad debt expense provided headwinds.

The company hosted a call at 5 p.m. EDT Tuesday to discuss results with analysts. Stay tuned to FreightWaves for continuing coverage of J.B. Hunt’s earnings announcement.

More FreightWaves articles by Todd Maiden

- XPO, RXO financial targets imply no letup through 2027

- Cass: September increase in shipments a head fake

- Transfix pulls IPO, new private funding round planned