Improved trucking demand and spot rates should begin to bleed into Jacksonville-based freight broker Landstar System’s (NASDAQ: LSTR) financial results more meaningfully in the third quarter. The company appears to be turning the corner from the depths created in the early days of COVID-19-related lockdowns.

That was the tone of the company’s second quarter earnings call held with analysts on Thursday, July 23.

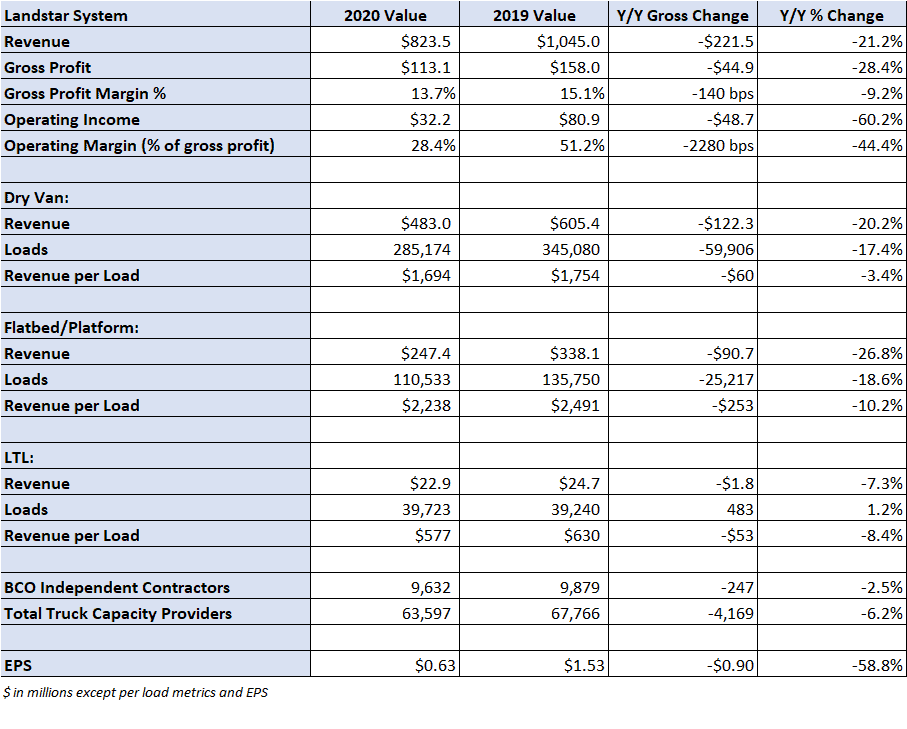

The company’s third quarter outlook calls for revenue to be in the range of $885 million to $935 million and earnings per share (EPS) to be in a range of $1.11 to $1.17. That outlook is much better than the company’s second quarter result, a revenue decline of 21% year-over-year with EPS falling to $0.63. The result was a fraction of the $1.53 EPS posted in the second quarter of 2019 and fell short of consensus estimates that ranged from $0.70 to $0.72 per share.

The new EPS guidance range is 14% higher than the $1 per-share consensus estimate (at the midpoint of range) and doesn’t include any improvement in the industrial sector. So far in July, loads and revenue per load moved by truck are down in the mid-single-digit range year-over-year, a trend the company expects to hold throughout the third quarter. This is an improvement from the 21% decline in loads reported during April and May. June loads were off 9%.

Second quarter results

The headline EPS miss included some one-off items. Landstar paid $12.6 million, or $0.25 per share, in pandemic-related incentive compensation to workers during April and May. There were two separate charges of $0.05 per share related to asset impairments in its Mexico operations and higher third-party insurance premiums. Excluding the COVID-19 bonuses and asset impairments, the EPS result was better than $0.90 per share.

The 21% year-over-year revenue decline was comprised of declines across most industries Landstar serves. Automotive (-53%), metals (-35%) and machinery (-30%) saw the biggest declines. Categories like consumer durables, building products and hazmat were off approximately 20%. The outperformers were foodstuffs (+22%), which continue to benefit from the stay-at-home trend, and energy (-2%).

Members of the management team said they expect automotive, steel and aerospace to start to contribute more moving forward. Automotive-related freight accounts for 8% to 10% of Landstar’s revenue.

Revenue per load was off by 6%, 9% and 6% year-over-year in April, May and June, respectively.

When asked on the call why Landstar didn’t see a stronger snapback in yields as spot rates improved through the quarter, management said they are seeing sequential improvement in yields. However, they noted their affiliates are mostly small business owners and tend to lag the broader market and large operations in responding to changes in spot rates. They believe the rate improvement in the market will start to bleed into results soon. Their official guide is for pricing on truck loads to improve “slightly” from the second quarter.

Landstar reported a 2% increase in business capacity owners (BCO) from the first quarter, but total truck capacity in the network declined 2.1% as approved and active carriers were down 3.3% sequentially. Management said that utilization in those numbers remains low as some carriers with high-risk drivers parked their trucks for a few weeks. Utilization among Landstar’s BCOs was the worst in a decade with the metric down 18% in April, 16% in May and only down 4% in June. Management expects modest BCO growth in the third quarter.

On industry-wide capacity eliminations, management said other headwinds like higher insurance costs are curbing capacity, but they haven’t seen a major decline in available trucks from the fleets with 10 trucks or less.

The company’s operating margin, defined as operating income as a percentage of gross profit, declined 2,280 basis points year-over-year to 28.4%. The result included the bonus payments of $50 to each agent dispatching a load and each BCO delivering a load during the months of April and May.

Also, insurance and claims expenses continue to be a headwind. Landstar’s 2020 insurance renewal on May 1 resulted in a $14 million, 175%, increase. Management said the increase was in part due to the age of the equipment. The bulk of the BCO fleet is pre-2017 models, which don’t have the latest crash avoidance systems. Landstar is looking at ways to incent the fleet to outfit their tractors with aftermarket sensors, etc. to lower premium expense.

The company’s goal is to still generate operating margins in the high 40% to 50% range in the future.

Landstar generated $99.2 million in operating cash flow during the quarter and closed the period with $282 million in cash and short-term investments and undrawn revolving credit capacity of $216 million. The company’s cash balance was up $71 million compared to the first quarter. Landstar raised its quarterly dividend 13.5% to $0.21 per share, but didn’t repurchase any of its shares in the quarter.

Management said they will stay “prudent” in regard to liquidity due to the potential for widespread shutdowns as new COVID-19 cases increase. The company normally increases the divided 10% annually.

Shares of LSTR are up less than 1% on the day compared to S&P 500, which is off slightly. The stock is up 8% for the month of July.

Click for more FreightWaves articles by Todd Maiden.