AP Moller Maersk (Copenhagen: MAERSK-B), the largest container-line operator in the world, announced better-than-expected guidance for 2020, but that guidance has high downside risk due to the coronavirus.

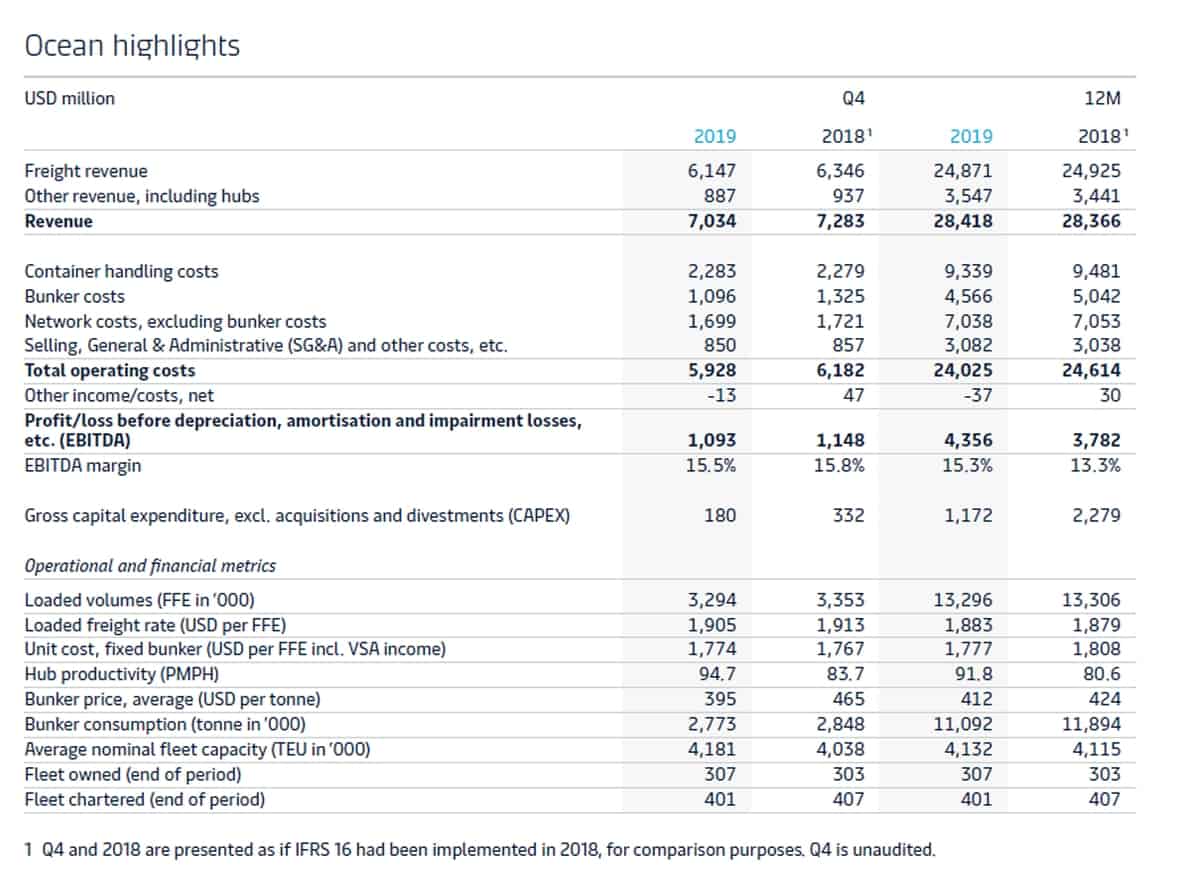

On Thursday, Maersk reported earnings before interest, tax, depreciation and amortization (EBITDA) of $1.463 billion for the fourth quarter of 2019 versus $1.449 billion for the fourth quarter of 2018. EBITDA for the most recent quarter came in 3% below the consensus forecast of $1.514 billion.

The number the market is much more focused on is Maersk’s EBITDA guidance for full-year 2020: $5.5 billion (plus or minus 10%), which came in 7% below the consensus estimate of $5.9 billion.

According to Frode Mørkedal, shipping analyst at Clarksons Platou Securities, “Given the usually conservative guidance from the company, one might find solace in that the guidance wasn’t lower than this … [it] could be viewed as relatively optimistic.”

That appears to be what the market initially thought, with Maersk’s share price jumping 5% in the first 30 minutes after the opening bell. However, shares then fell back , declining during the call with analysts and thereafter, and were down over 4% later in the trading session.

Contingent on coronavirus

The earnings release made clear that the 2020 guidance “is subject to significant uncertainties.” The call comments emphasized that swift containment of the coronavirus is pivotal to the guidance — implying one reason why Maersk’s stock gave back early gains.

Maersk CEO Soren Skou said on the call, “We estimate right now that factories in China are operating at 50-60% of capacity. That will be ramping up to around 90% of capacity by the first week of March.

“Currently, the external consensus is that the outbreak will peak over the coming weeks and data suggests that this is true. [If so] we can expect a trajectory similar to the one experienced during SARS, but with a larger magnitude, because China’s impact on the global supply chain is much bigger today and China’s role in the global economy is much bigger.”

He continued, “That would imply a so-called V-shaped crash and recovery, which means that we would have really, really weak Chinese exports in February — we know that for sure — then a weak March, and hopefully a strong rebound in April, May and June.

“But this prognosis certainly implies there will be no new outbreaks and no big outbreaks in other countries outside China,” Skou said. “So, the next two to three weeks will really tell us what track we are on. It all depends on how long the outbreak lasts.”

He warned, “If a V-shaped or U-shaped recovery does not happen, because new cases start to appear elsewhere, even in countries that have less ability to deal with it, that is the main risk [to the guidance] we’re worried about. I want to be cautious about saying how much I expect the V-shaped recovery. That’s what the trend looks like right now but I want to emphasize that there are plenty of risks.”

IMO 2020 on track

Before coronavirus came to the fore, the most important issue for container shipping was the IMO 2020 fuel rule, which requires all vessels without exhaust-gas scrubbers switch from 3.5% sulfur heavy fuel oil (HFO) to more expensive 0.5% sulfur fuel called very slow sulfur fuel oil (VLSFO) or 0.1% sulfur marine gas oil (MGO). For container lines, the most important question is: Can the added fuel cost be fully passed along to cargo shippers?

According to Skou, “We are two months into the year and I can say that the switchover to low-sulfur fuel was very successful. We didn’t have any operational problems and our fleet is now fully compliant with the sulfur cap. Currently, only a limited number of our vessels have scrubbers installed due to delays at the yards and the situation in China, and I think those delays are probably going to become even longer.”

He said Maersk’s fleet currently consumes 10% HFO, 10% MGO and 80% VLSFO. By year end, when more scrubbers are installed, he expects HFO’s share to rise to 25%.

“We have witnessed high volatility in fuel prices,” he added, noting that as a result, Maersk will implement a new surcharge of $50-$200 per forty-foot-equivalent unit on March 1.

Asked about passing costs along to shippers, he replied, “As far as spot volumes, which are about half our volumes, if you look at the Shanghai Freight Index, freight rates have gone up substantially since Oct. 1 [2019] at least until Chinese New Year.”

Regarding contracts, he said, “We are pretty much halfway through the contracting season. What I can say is: ‘So far, so good.’ But obviously, we have the other half still to be negotiated and that will be negotiated in a weak environment post-Chinese New Year, so we’ll see how it goes.” More FreightWaves/American Shipper articles by Greg Miller