The enforcement deadline for IMO 2020 — the international rule that requires ocean shipping to switch to more expensive low-sulfur fuel — is six days away, on Jan. 1, but the transition to the new fuel type has largely already occurred. Are ship owners and operators successfully passing along the higher cost to beneficial cargo owners (BCOs)?

The very early answer appears to be: mostly no.

Fallout focus has centered on container lines, given their set schedules and high fixed costs. If lines cannot pass incremental fuel expenses along to BCOs via surcharges, they will be forced to “blank” (cancel) more sailings to artificially inflate freight rates.

That, in turn, would have significant consequences for service reliability for BCOs, as well as on port throughput and import box volumes for trucking and rail.

There has been less concern towards bulk shipping earnings in the so-called “tramp” trades, where there is no set schedule, but here too, headwinds from higher IMO 2020 fuel costs could have a significant negative impacts on margins in certain vessel classes.

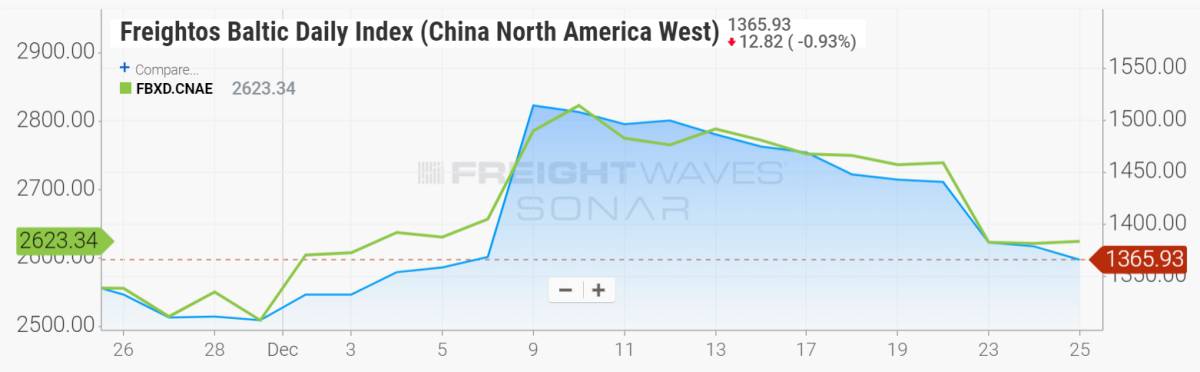

Container shipping effects

Container lines implemented bunker adjustment factors on Dec. 1 to recoup the costs of switching from 3.5% sulfur heavy fuel oil (HFO) to either 0.5% sulfur fuel known as very low sulfur oil (VLSFO) or 0.1% sulfur marine gas oil (MGO).

If those surcharges worked as planned, it should have led to an immediate pop in the spot rates to transport containers, which are tracked by the Freightos Baltic Daily Index.

It did. The rates in the early part of December jumped across all the major trade lanes as expected.

The problem is that the rate hikes haven’t held up across the board. In the largest trade, Asia-Europe, the December rate increases have held firm, but in the second-largest trade, the trans-Pacific, they haven’t. Rates from China to the North American West Coast (SONAR: FBXD.CNAW) and the East Coast (SONAR: FBXD.CNAE) have slumped back.

According to Freightos Chief Marketing Officer Eytan Buchman, “China-U.S. rates continue their slide from the early December gains, disappointing carriers hoping to sustain higher prices through IMO 2020 costs and reduced capacity.”

A container ship carrying 8,000 20-foot equivalent units (TEUs) transiting the Pacific at a speed of 19 knots burns about 100 tons of fuel oil per day. The current cost of VLSFO in Singapore is about $690 per ton. A year ago, the cost of HFO in Singapore was around $340 per ton. Thus, an 8,000-TEU trans-Pacific vessel is now experiencing a year-on-year fuel cost increase of $35,000 per day, whereas year-on-year box-shipping rates between Asia and California are down $190 per TEU.

Dry bulk shipping effects

In the bulk trades, fuel is paid by the vessel owner-operator in a spot voyage deal (which is priced in dollars per ton of cargo), whereas in a time-charter agreement (priced in dollars per day), the time charterer, not the vessel interest, pays for fuel. Owner-operators with ships locked away on profitable time charters are shielded from IMO 2020 fuel costs until those contracts expire.

Current dry bulk spot rates are not compensating owners for switching over to VLSFO/MGO. In a client note on Dec. 20, Clarksons Platou Securities analyst Frode Mørkedal warned that higher VLSFO prices have “generally put pressure on owners’ earnings as freight rates have not adjusted accordingly.”

As bulker owners switched to more expensive fuel over the fourth quarter, spot freight rates have fallen. Their costs increased as revenues decreased, meaning that the IMO 2020 fuel switch exacerbated profit headwinds.

Rates for Capesizes (vessels with capacity of 100,000 deadweight tons, DWT, or more) burning VLSFO averaged $14,600 per day on Dec. 20, which is getting close to breakeven levels and is down 40% from the end of the third quarter.

Mørkedal believes current rate levels will spur pushback in spot negotiations from owners facing higher expenses. “The surging fuel cost is likely to be met with resistance from owners going into 2020,” he said.

Analysts and executives have highlighted upside for bulker owners installing exhaust-gas scrubbers, which will allow for the continued use of cheaper HFO. Amit Mehrotra, analyst for Deutsche Bank, said in a Dec. 26 client note, “The average spread [between HFO and VLSFO] has firmed to $263 per ton, the highest level on record. We continue to have a favorable outlook on fuel price spreads in 2020, which has positive implications for companies investing in scrubbers.”

One caveat to the pro-scrubber case is that the fuel-spread upside depends upon the percentage of a company’s fleet with scrubbers and when they’re installed.

The furthest along among the public companies is Star Bulk (NYSE: SBLK), which expects almost all of its fleet to have scrubbers installed by Jan. 1. In the case of most companies, however, yard delays are pushing a large number of installations into the first and second quarters of 2020.

Meanwhile, many companies, as exemplified by Golden Ocean (NASDAQ: GOGL), are installing scrubbers on only a portion of their fleets. When companies report their quarterly average time-charter equivalent (TCE) rates, converting spot rates done in dollars per ton into the equivalent dollars-per-day rate with expenses such as fuel factored in, scrubber ships in the spot market should inflate the fleet’s average TCE due to lower fuel costs. But if a portion of the same fleet needs to burn VLSFO or MGO, it will reduce TCE versus historical rates and counterbalance scrubber upside.

Another caveat that gets relatively little attention is that even if a company’s entire fleet is fitted with scrubbers and therefore reports a higher average TCE, those scrubber installations were expensive, so the true advantage to the company’s bottom line would only accrue after the scrubbers are paid off, which in the best-case scenario would be in 2021.

During a webinar presentation by Capital Link in July, Star Bulk President Hamish Norton argued that IMO 2020 would ultimately benefit all bulker owners, including those that aren’t installing scrubbers.

“When a ship is burning low-sulfur fuel, that’s expensive fuel, and clearly the vast majority of the dry bulk fleet is going to be burning low-sulfur fuel. Either the rates go up, or the fleet will have to slow down,” he claimed. “If the fleet slows down, not as much cargo can be carried. If the same amount of cargo needs to be carried, the fleet cannot slow down and the rate needs to go up to match the increase in fuel price.”

The counterarguments: What if demand weakens and the same amount of cargo does not need to be carried? And even if demand does not weaken, what if the transition to slower speeds takes time, weighing rates before it fully plays out?

Tanker shipping effects

The difference between the tanker sector and the dry bulk sector is that the fundamentals in dry bulk appear weak and the fundamentals for tankers are strong.

In a weak market, the negotiating power in the spot voyage negotiation goes to the cargo interest, meaning that the vessel interest is less likely to recoup its higher fuel cost. The situation reverses when vessel supply is tight, as is the case with tankers.

But even so, higher year-on-year fuel costs for tanker owners with a high percentage of their fleets in the spot market are inherently bad for those vessel interests.

In an interview with FreightWaves on Dec. 19, Lois Zabrocky, CEO of crude- and product-tanker owner International Seaway (NYSE: INSW), admitted, “It’s a negative. When your input costs go higher, that’s a challenge. When you start paying $600-$700 per ton for bunkers, that’s a big cost input for owners — particularly so in containers and dry bulk. For tankers, there’s more refining [due to IMO 2020] and we’re moving the oil, so at least we’re getting benefits from that.”

Further concerns ahead

Even more IMO 2020 risks to ocean shipping bottom lines lie ahead.

VLSFO is less expensive than MGO, but there are yet-to-be-determined risks with VLSFO. There are considerable differences between the compositions of the myriad VLSFO products being marketed around the world, which could spur engine malfunctions and compel owners to use MGO despite higher cost and lower profit margins on spot deals.

In addition, the IMO 2020 transition is occurring amidst a period of relatively benign oil prices. As of Dec. 26, Brent crude was $68 per barrel, well below the $100-plus per barrel levels that prevailed in 2011-14. If crude prices were to go higher due to a geopolitical event, the pricing of VLSFO and MGO would quickly follow suit, putting even more pressure on ocean shipping margins. More FreightWaves/American Shipper articles by Greg Miller

Editor’s note: Freightos has a business agreement with FreightWaves that includes editorial coverage.