What was billed as a blowout quarter got off to a slow start with the first couple of truckload (TL) carriers posting in line or worse-than-expected quarterly reports. As the earnings season progressed, several companies began to report results better than and some well ahead of analysts’ forecasts.

Carriers were busy in the third quarter hauling all the essentials required by stay-at-home-lifestyles. Shipments of grocery and other retail consumables, appliances, exercise equipment and home improvement goods moved through supply chains at a breakneck pace. Hard goods in need of shipment have replaced discretionary spending on services and the need for continual restocking was on full display in the quarter.

Every carrier to some degree proclaimed the strength in consumer demand and the lack of available truck capacity to meet the need. Expectations of favorable freight fundamentals, including significant contractual price increases throughout 2021, was the hot topic on most earnings calls. However, every carrier bemoaned their struggles capturing incremental freight as drivers remain in short supply, a condition the group expects will continue through next year.

Analysts raced to raise earnings estimates for the carriers they follow as the quarter progressed, with each seemingly outdoing the other to sit atop with “Street-high” forecasts. The TL stocks ticked higher with each passing positive data point until the trade petered out shortly after the Labor Day freight lull.

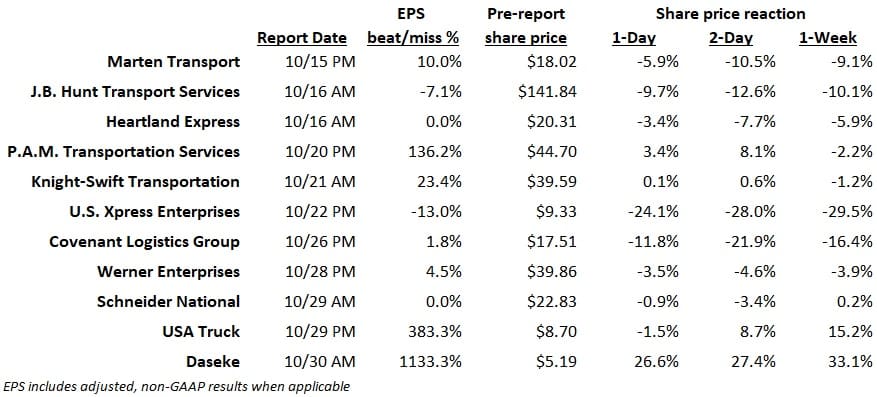

While the stocks cooled off a bit heading into the third-quarter earnings season, the perception from investors didn’t. Most names were still seemingly priced for perfection and anything less was met by a sell-off. The average one-day share price reaction for companies posting a modest beat, in line results or a miss was -7%, not reflective of a truck market still in the early innings of a bull cycle.

If this list were based solely on share price performance, it would mostly include laggards. To be fair, the broader market sold off at the end of October followed by a strong rebound this week, potentially detracting or enhancing share price reactions for some carriers.

The bull-bear debate is likely to continue into 2021, with the bulls expecting inventory restocking, tight truck capacity and a lack of drivers to tighten the screws on asset utilization and move rates higher. They will say those factors combined with COVID-cost actions, some of which will not be reversed, will move operating ratios (ORs) and earnings higher. The bears will point to capacity – previously parked and new Class 8 truck orders – as indicative of a market not likely to produce the large contractual rate increases already priced into the stocks.

In any event, the following is a compilation of the TL carriers that stood out in the quarter and those that lagged the group.

The winners

Knight-Swift Transportation (NYSE: KNX)

The nation’s largest carrier, Knight-Swift put up the type of quarter analysts were anticipating. The carrier bested third-quarter adjusted earnings per share (EPS) estimates by 23% (on an estimate that increased 34% in the 90 days leading up to the report), raised 2020 earnings guidance by more than 20% and issued full-year 2021 guidance 14% higher than the consensus estimate at the time of the print.

The increased guidance was the expectation that “strong freight conditions” will continue and management’s belief that current fundamentals support “low double-digit contract rate increases in 2021.”

There was some noise in the adjusted earnings number, but all of the underlying trends were impressive.

The TL segment reported steady volume trends with revenue per tractor increasing 5% due to a similar increase in the pricing metric, revenue per loaded mile excluding fuel surcharges. A “focus on cost control” also played a hand in adjusted OR improvement of 620 basis points year-over-year to 81.3%. Consolidated adjusted operating income increased 61% on virtually no increase in revenue. TL adjusted operating income was up 54%.

P.A.M. Transportation Services (NASDAQ: PTSI)

P.A.M. Transportation, which generates nearly half of its revenue moving goods for the auto manufacturing sector, snapped back to a profit, posting third-quarter adjusted earnings more than double that of the consensus estimate.

The trends weren’t overly impressive on a year-over-year comparison. Revenue excluding fuel surcharges was flat. Inclusive of fuel, TL revenue fell 15% as average tractors in service, loads and total miles were all down 10% to 12%. Further, pricing and utilization (revenue per loaded mile and revenue per tractor per week excluding fuel surcharges) were only flat.

Previously implemented cost actions drove the earnings improvement. The TL OR improved 290 basis points year-over-year to sub-90%, a far cry from the second quarter’s 104% OR and $2.5 million loss. The carrier’s operations clearly bounced back when its three largest auto manufacturing customers resumed operations.

Werner Enterprises (NASDAQ: WERN)

Carrying “essential” goods for discount and home improvement retailers kept Omaha, Nebraska-based Werner rolling along in the quarter. Adjusted EPS outpaced forecasts, which increased nearly 40% in the 90-day lead-up to the report, by a couple of cents.

The company increased its long-term operating margin goal for its trucking segment from 11% to 13%. To be clear, that’s an average adjusted operating margin, excluding fuel, of 13% throughout each trucking cycle. Management expects to exceed the new target in 2021.

The company’s four largest retail customers saw same-store sales increase by an average of 15% in their most recent reporting periods, while inventories fell by 8% over the same period, which management said could lead to several quarters of inventory replenishment.

The company is planning for a “robust” rate environment in 2021 as capacity is constrained and drivers are becoming increasingly difficult to find. Management sees a “stronger setup” going into 2021 than they saw heading into 2018, noting that the economy isn’t even fully open yet.

TL revenue was down 5% year-over-year but both segments, one-way and dedicated, reported mid-single-digit increases in revenue per tractor per week. Revenue per total mile increased 3% in the one-way segment and the new guidance calls for this metric to be up 3% to 5% in the fourth quarter. Improved pricing and “aggressively managing expenses” produced a record adjusted TL OR of 84.5%.

A nearly $1 million loss in the logistics division, as loads fell 15% and gross margins sank 440 basis points to 10.8%, provided one of the few blemishes on the report.

USA Truck (NASDAQ: USAK)

USA Truck posted an adjusted EPS number nearly 5x what the Street was predicting, its first quarterly profit in the last five attempts. Efforts to transition into a regional carrier and improve asset utilization were evident in the result.

The carrier reported a slight increase in loaded miles per truck. Management said utilization improved throughout the quarter with October “substantially better than September,” and that the fourth quarter should see sequentially better results. They believe there is another 5%-plus upside to be gained in truck utilization.

Revenue per loaded mile increased 9% year-over-year, and cost actions resulted in a 95.8% adjusted OR, 410 basis points better year-over-year and 200 basis points better sequentially. Management said rates have already moved higher in October and they expect to gain a couple hundred basis points of OR improvement in 2021, a level that would be on par with the industry average. With more than 75% of its contracts already repriced higher, the year-over-year comparisons are favorable in the first half of 2021.

Daseke (NASDAQ: DSKE)

The nation’s largest flatbed carrier, Daseke, hammered expectations, reporting adjusted EPS of 31 cents compared to consensus of a modest loss. The company was quick to point out that it benefited from approximately $15 million in incremental earnings before interest, taxes, depreciation and amortization (EBITDA) from project freight that isn’t likely to recur at the same pace going forward. Investors didn’t seem to care as the stock was up 27% the day of the report.

The favorable project work and restructuring efforts – headcount and equipment reductions and consolidating separately operated flatbed companies – resulted in 610 basis points of adjusted OR improvement to 90.9%. Management said the company’s core business should continue to improve in 2021 alongside a favorable rate environment. The company’s longer-term OR goal remains sub-90%.

The improved results drove debt leverage lower as net debt-to-adjusted EBITDA declined to 2.6x from 3x in the second quarter.

The laggards

J.B. Hunt Transport Services (NASDAQ: JBHT)

Not a pure trucking play, as intermodal accounts for 60% of operating income, J.B. Hunt missed the consensus estimate by 7%, a number that was raised nearly 20% by analysts in the three-month period heading into the report. Excluding the impact of prior-year arbitration charges related to a dispute with a railroad partner, operating income was actually down 17%.

The miss was due to railroad congestion and a lack of labor. Containers have flooded into the West Coast in efforts to restock depleted inventories and the rails are still trying to bring back furloughed employees and add equipment to handle the volume surge. Further, management said many of its customers are struggling to find the dockworkers required to unload containers at their facilities, which is further tying up box capacity.

Slower service on the rails and an equipment imbalance produced an elevated cost structure. Excluding the impact of last year’s charges, intermodal operating income was down 18% year-over-year.

Another obstacle in the quarter was widening losses within the brokerage segment. Revenue surged on higher truck rates but gross margins collapsed, down 510 basis points to 7.6%. Brokers were forced to pay up for capacity, which was in short supply, to honor contractual agreements. The loss in the division was more than three times higher year-over-year.

The trucking segment saw improved topline trends year-over-year but a decline in operating results. Loads increased 14%, revenue per loaded mile excluding fuel was up 4% and revenue per truck increased 24%. However, increased costs for purchased transportation, personnel and technology, as well as investments in the drop-trailer program resulted in operating income dropping by more than half (OR deteriorated 430 basis points to 97.3%).

Tailwinds included: roughly 60% of the company’s intermodal business will likely be repriced higher by the end of the first quarter; steady improvement in the dedicated division; and a return to profit in the final mile segment.

U.S. Xpress Enterprises (NYSE: USX)

One quarter removed from posting a large earnings beat and unveiling its new digital fleet Variant, U.S. Xpress couldn’t execute a repeat.

Shares of USX surged 44% in the two days following the second-quarter report on the news that the company’s new digitally dispatched and managed fleet was operating at a 500-basis point OR premium to legacy operations. The stock climbed more than 60% higher in the weeks following the announcement, nearly 40% higher heading into the third-quarter print.

This go around, the Chattanooga, Tennessee-based carrier came in 3 cents per share light of expectations, which had increased from slightly better than breakeven to 23 cents per share in the months leading up to the report. Not to be lost on the headline miss, the company’s adjusted operating income increased nearly 5x to $16 million. The year-over-year comparisons didn’t matter to investors. The stock sunk 24% the following trading session on the miss.

Revenue per tractor in the company’s over-the-road fleet, which sees freight from the spot market, increased 6% year-over-year as revenue per mile climbed 7%. The dedicated segment saw steady results with revenue per tractor up 1% as revenue per mile dipped 2%. The TL division reported adjusted OR improvement of 490 basis points, albeit off near-breakeven levels, to 94.1%. Brokerage was a drag on the quarter, posting a $4.5 million loss compared to breakeven results last year.

The company plans to convert 900 tractors to the digital fleet by the end of the first quarter with another 1,200 units in the works.

Covenant Logistics Group (NASDAQ: CVLG)

Covenant came in slightly ahead of its previously raised expectations. The positive earnings preannouncement in September sent shares 24% higher in the weeks that followed, but the stock managed to hold only a third of that gain heading into the third-quarter report.

Covenant has a restructuring plan in place aimed at improving returns on asset-based offerings like its dedicated and expedited operations while downsizing less profitable segments like solo-driver refrigerated. The carrier operated nearly 550 fewer tractors in the quarter, down 18% year-over-year, which resulted in an 11% decline in TL freight revenue excluding fuel.

Freight revenue per truck improved 8% year-over-year as miles per tractor increased 10% and freight revenue per total mile declined 2%. The change in rate per mile was attributed to a change in freight mix and length of haul, not softness in pricing, which management said “improved markedly.”

A reduction in costs and improved asset utilization resulted in an adjusted OR of 93%, 1,040 basis points better year-over-year. Adjusted TL cost per mile improved by 19 cents on a net basis. Management said that 14 cents of the improvement is related to the restructuring plan, while 5 cents per mile represented temporary COVID-related cost initiatives.

Management said some cost inflation – driver pay and insurance costs – will come back before contractual rates are reset higher, noting that some of its expedited contracts will not reprice until May and June.

The stock was off 12% following the report.

Somewhere in between

Marten Transport (NASDAQ: MRTN)

Refrigerated carrier Marten posted a modest beat but the bulk of the year-over-year improvement can be attributed to a gain from the sale of a facility.

Revenue was up 4% excluding fuel surcharges with revenue per tractor per week increasing 6% in the TL segment, down 3% in dedicated. Both divisions reported mid-single-digit declines in revenue per loaded mile versus 2019. Margins were strong, up 400 basis points in TL and flat in dedicated.

The consolidated tractor count increased 200 net units, a win in a tight driver market, with dedicated seeing the growth. Marten posted its best operating results for the first three quarters of any year since going public in 1986.

Heartland Express (NASDAQ: HTLD)

Heartland posted an in line result, flat year-over-year, on a consensus estimate that increased more than 30% during the quarter.

Revenue increased 14% year-over-year excluding fuel surcharges. The carrier posted an adjusted OR of 81.5%, 210 basis points worse year-over-year, but pretty solid considering it is still trying to integrate the Millis Transfer acquisition. Additionally, gains on equipment sales declined nearly $7 million, which is meaningful on a $27 million adjusted operating income number.

Schneider National (NYSE: SNDR)

Schneider made a splash with the announcement of a $2-per-share special dividend, answering questions from investors as to the company’s plan for its large cash balance.

However, that announcement was mostly overlooked by the rest of the in line third-quarter earnings report, which displayed relative softness in fundamentals – a decline in revenue per truck and lower operating income in the company’s intermodal and brokerage divisions – during a bull market for trucking.

The TL division reported an 11% year-over-year decline in revenue excluding fuel surcharges as the average tractor count fell 8% due to difficulty finding drivers. Pricing in the company’s one-way segment improved throughout the quarter, up mid-single digits in September, as the carrier has moved more trucks into the spot market.

Intermodal revenue was flat year-over-year as network congestion on the railroads, drayage capacity constraints and delays unloading containers at customer facilities, presented both revenue and cost headwinds. The intermodal segment recorded an 80-basis point margin decline. A similar margin decline was registered in the logistics segment but the division’s 96.8% OR was better than most asset-based brokerage operations during the quarter.

Management narrowed its 2020 adjusted EPS guidance range with the high end of the range level with consensus at the time of the report.