On its second-quarter earnings call with analysts, members of truckload (TL) carrier Schneider National’s (NYSE: SNDR) management team said they expect TL volumes to be higher year-over-year in the third quarter.

Prior to the market open on Thursday, the Green Bay, Wisconsin-based company reported second-quarter 2020 adjusted earnings per share (EPS) of 26 cents, 7 cents better than consensus but 8 cents lower year-over-year.

Currently, the carrier is seeing daily freight tenders exceed available capacity as the bulk of its customer base — retail consumables, food and beverage — continues to benefit from the stay-at-home environment created by COVID-19. This customer base has also indicated to Schneider the trend should continue.

Management said based on conversations with customers, they see a “decent chance” for rates to be net positive for all of 2020, an inconceivable scenario just one quarter ago. While the carrier has completed 80% of this year’s bids, management said some prior contract negotiations completed earlier in the year may have to be addressed as those deals were inked well under current market rates.

The carrier reinstated full-year 2020 earnings guidance to a range of $1.10 to $1.25 per share. The new guidance is higher than the current consensus estimate of $1.05 but below the original $1.25- to $1.35-per-share range.

Given the improvement in trends, the conversation on the call quickly turned to the company’s growing cash balance.

Future cash deployment

The company’s cash balance improved to $714 million at quarter’s end. The primary drivers were lower capital expenditures (capex) as the original equipment manufacturers (OEMs) couldn’t keep delivery schedules intact during the height of the COVID lockdowns; a modest increase in cash flow from operations year-over-year; and deferrals of payroll taxes afforded under the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

However, management expects the company to be a net user of cash in the second half of 2020, ending the year with a cash balance around $700 million. The carrier has roughly $180 million in net capex remaining as 2020’s tractor purchasing is now back-half weighted. Changes in working capital are expected to consume cash, and the company plans to pay off a $30 million note.

Asked about potential uses of cash, management said they are looking to deploy cash in the next four to six quarters, retaining at least $250 million on the balance sheet. They are actively pursuing M&A, likely dedicated or specialty asset-based operations, but tempered expectations as they are looking for a perfect fit and many of the opportunities recently vetted have been small.

In addition to acquisitions, management has talked about internal organic initiatives, share repurchases and maybe raising the dividend in the past.

Asked if there was the potential for the company to repurchase shares controlled by the Schneider family and their trusts, management said there has been no development on that front. The company’s common stock structure consists of two classes, with the family owning 100% of the “A” shares and 43% of the “B” shares. According to the company’s annual filing, the family owns approximately 70% of the total common stock outstanding and represents 94% of total voting power.

In recent weeks, other predominantly family-owned, publicly traded trucking companies have announced secondary offerings to allow their controlling family interests to be unwound.

Last week, Heartland Express (NASDAQ: HTLD) announced the Gerdin family was selling a less than 5% stake in the company. In June, Werner Enterprises (NASDAQ: WERN) announced its founder, C.L. Werner, was stepping down from his role as executive chairman of the board and would sell nearly 20% of the company’s stock.

Second-quarter results

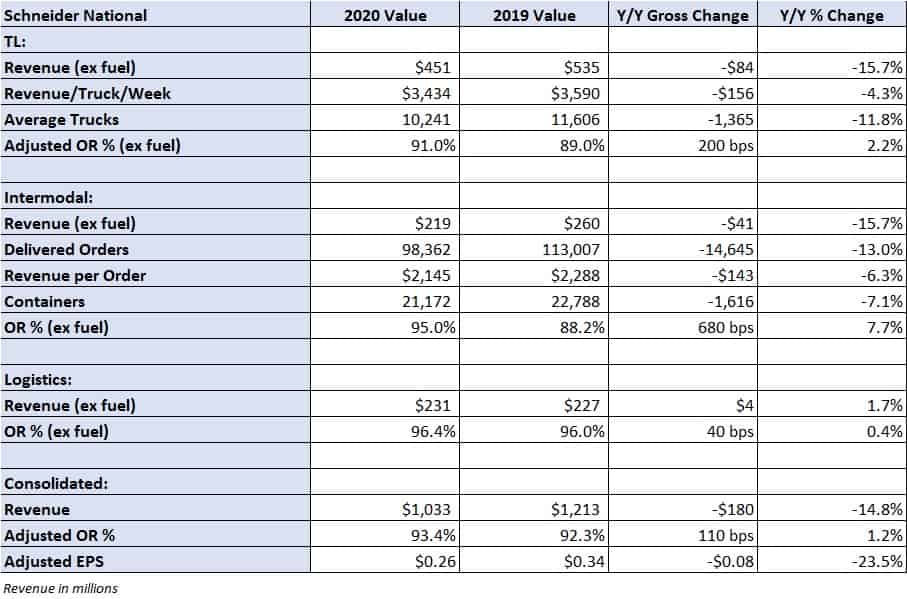

Consolidated revenue declined 14.8% year-over-year to $1.03 billion, with an adjusted operating ratio (OR) of 93.4%, 110 basis points worse. As a percentage of revenue, salaries, wages and benefits, and operating supplies expense each increased 40 basis points.

Health care costs were lower as frequency of doctor visits and procedures declined and lower driver turnover reduced driver cost per new hire in the period. The company incurred $3 million in incremental expense for personal protective equipment for drivers and increased cleaning. This expense is expected to recur quarterly for the rest of 2020. Management noted driver cost per hire is ticking higher as well, as volumes increase.

Other cost inflation was seen. Purchased transportation and depreciation and amortization expenses were up 80 basis points each, with fuel costs providing some offset, down 220 basis points as a percentage of revenue.

TL revenue declined 15.7% year-over-year to $451 million as revenue per truck per week declined 4.3%. The closure of its final-mile unit presented a revenue headwind along with lower volumes and pricing. Schneider reported an improvement in volume as the quarter progressed, with June ending near 2019 levels.

Intermodal revenue fell 15.7% year-over-year, with orders down 13% and revenue per order down 6.3%. An imbalanced network from weak Asia imports and the closure of nonessential retail were cited as the reasons for the decline. A mix shift to favor East Coast ports reduced the average length of haul, driving revenue per load lower. Management said their volume in the East was up in the high-single-digit range during the quarter.

Schneider’s intermodal volume decline was in line with the decline seen in U.S. intermodal volumes on the Class I railroads. Schneider’s rail partner in the West, BNSF Railway (Berkshire Hathaway Inc. NYSE: BRK.A) and its rail partner in the East, CSX Corp. (NASDAQ: CSX), reported 11% year-over-year declines in intermodal traffic during the second quarter.

The division reported 680 basis points of OR erosion to 95%. Management reiterated the long-term goal for intermodal margins to reach 10% to 12%. The third quarter is expected to see a better margin performance as volumes continue to improve, new contract awards are implemented and equipment in the network is better positioned.

Shares of SNDR are down 3% in midday trading compared to the S&P, which is down 0.5%.