Ocean shipping spot rate indexes are still falling. But after months of steep declines, they’re dropping much less rapidly than before. It could be just a temporary plateau before the next leg down. Or it could be something more significant: the first sign of the market bottom, the post-pandemic “new normal.”

Different spot rate indexes publish different numbers, and critics contend that indexes don’t reflect actual rates. But the consensus is that indexes are a good indicator of the general direction of pricing. And the direction spot indexes are headed lately is more sideways than down.

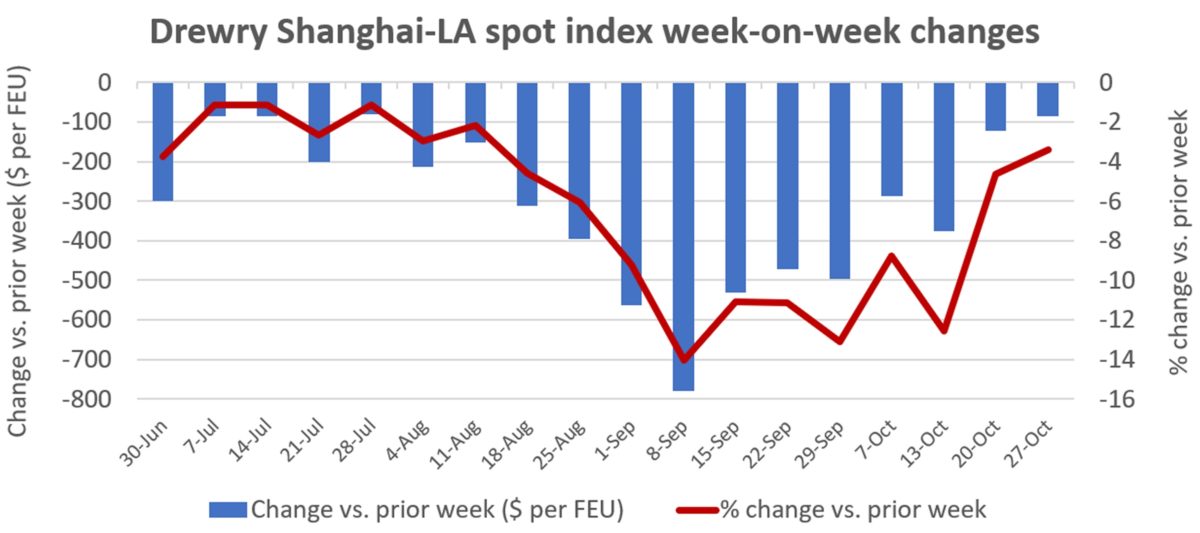

Drewry World Container Index

On Thursday, Drewry reported its World Container Index Shanghai-Los Angeles assessment at $2,412 per forty-foot equivalent unit. That was down only 3% or $85 per FEU week on week (w/w). Drewry’s Shanghai-New York spot estimate came in at $6,034 per FEU, down 3% or $180 w/w.

This is a big change from recent trends. Between mid-August and mid-October, the w/w decline in Drewry’s Shanghai-Los Angeles index averaged $468 per FEU, 5.5 times higher than in the most recent week. The largest w/w decline was recorded on Sept. 8: $780 per FEU, nine times higher than the latest drop.

Drewry’s current Shanghai-Los Angeles spot rate assessment is still 54% higher than in the same week in 2019, pre-COVID. The Shanghai-New York rate as well as Drewry’s global composite index are still more than twice as high.

Freightos Baltic Daily Index

The Freightos Baltic Daily Index (FBX) is showing a similar easing of the declines. According to Judah Levine, head of research at Freightos, “The transpacific ocean rate slide slowed this week as prices to the East Coast stayed level, [which] could be an early sign that the recent increase in canceled sailings by carriers is starting to have an impact on rates.”

For the FBX, the lull in declines goes back more than a week. The FBX China-West Coast index has plateaued for much of this month. It was at $2,494 per FEU on Wednesday, on par with rates on Oct 3. The FBX China-East Coast index was at $5,713 per FEU, unchanged since Oct. 18 and down only 5% from Oct 6.

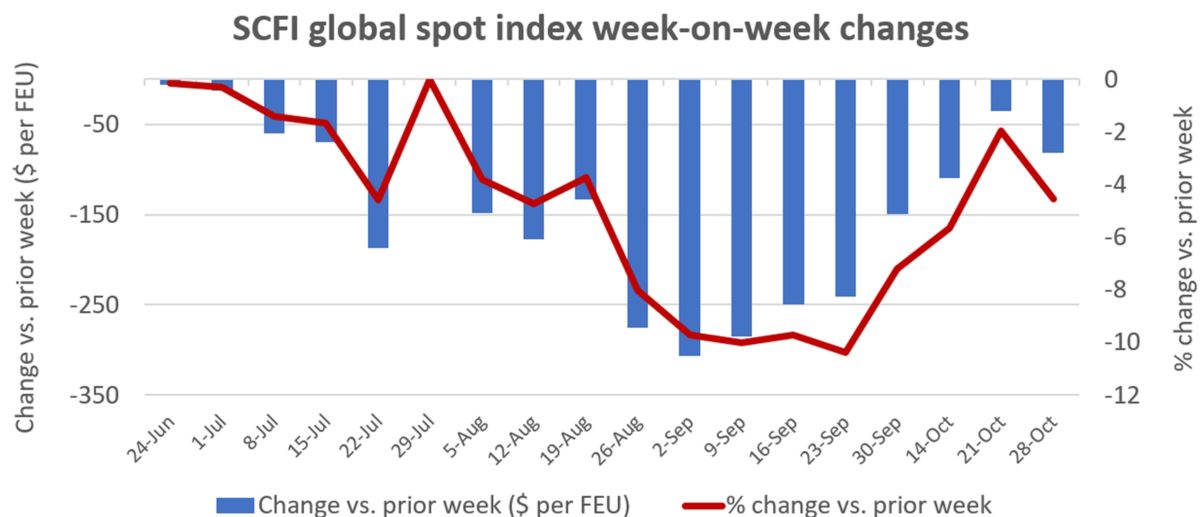

Shanghai Containerized Freight Index

The global composite of the Shanghai Containerized Freight Index (SCFI) shows roughly the same pattern as the other indexes: a sharp fall followed by lesser declines.

The scale of the SCFI’s weekly drops peaked in September and have since reverted to the more modest w/w pullbacks seen in July. The pace of w/w declines was over 10% throughout September. Over the past two weeks, the index has fallen by an average of 3.3%.

And even after all of this year’s steep declines, the SCFI global composite is still double pre-pandemic levels.

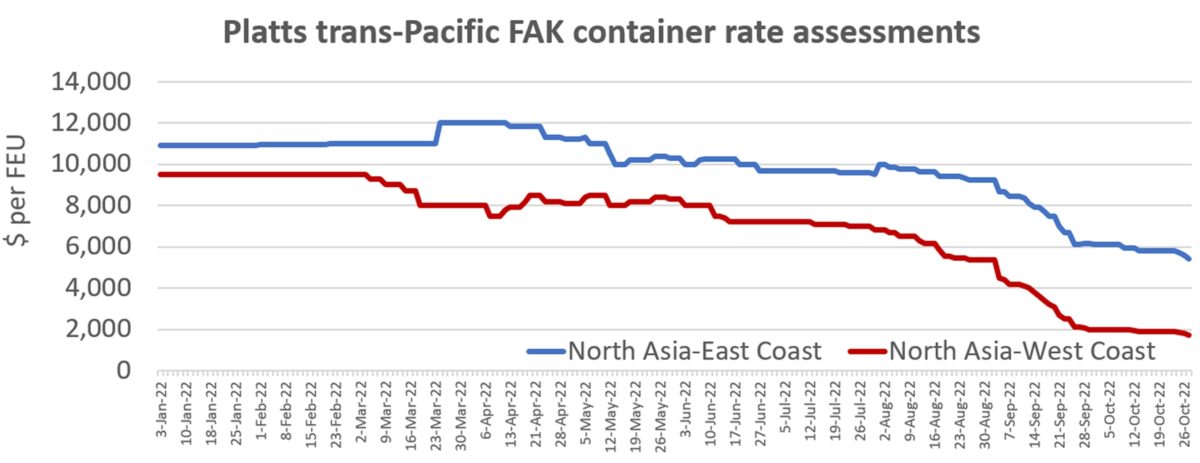

Platts FAK indexes

The Platts daily assessment by S&P Global Commodity Insights also shows a leveling off. Over the months of August and September, Platts’ North Asia-East Coast Freight All Kinds (FAK) assessment sank 39% and its North Asia-West Coast FAK assessment plunged 71%. For much of this month, declines have been in the single digits.

George Griffiths, managing editor of global container freight at S&P Global Commodity Insights, told American Shipper: “It does appear the market is heading toward a new level of normality. This return to normality comes on the back of void sailings and capacity management methods that have enabled carriers to preserve some of the rates they have in the market.”

However, Griffiths does not see a bottom as of now, and expects some further rate declines.

While rates to the West Coast are nearing pre-pandemic levels, he said that “the East Coast is still seeing significant strength, owing not only to capacity management, but largely to the ongoing delays at East Coast ports taking capacity out of the market and maintaining stronger rates. Many still expect there to be some [additional rate] falls on the East Coast lanes, bringing these levels closer to pre-pandemic levels.”

In light of weakening demand, Griffiths said that ocean carriers “have two simple choices: continue to employ capacity management and hope that rates bottom soon, or compete for the last scraps of spot cargo and see rates fall further.”

‘The jury’s still out’

During a presentation on Thursday, Simon Heaney, senior research manager at Drewry, addressed the sharp decline in spot rates in recent months, as well as the moderation more recently.

“Carriers probably waited too long to stop the rot,” he said, referring to the “precipitous” declines that occurred previously. Carriers “definitely ceded bargaining power to shippers and harmed their potential returns in the next round of long-term contracts. They put short-term greed or opportunism ahead of longer-term profitability.

“The challenge is to predict how far rates will fall and where they will settle,” said Heaney, who believes recent rate stabilization reflects carriers’ move to reduce capacity and bring it in line with reduced demand. “I think we’re starting to see carriers turning the corner slightly and getting a bit more control.”

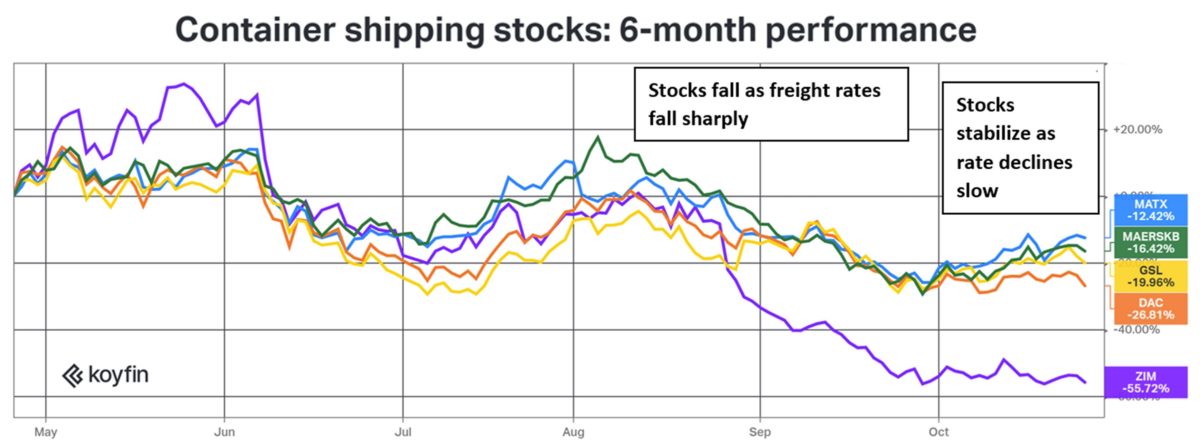

Whether spot rates are bottoming or not is important to container shipping stocks — not just liner stocks, but also ship-lessor stocks. (Lessors earn from ship charter rates, which are affected by freight rates.)

During an interview with American Shipper on Oct. 19, Jefferies shipping analyst Omar Nokta said: “Investors don’t want to be involved right now as freight rates are still declining. But the moment we start to see some stability in freight rates, I think buyers are going to be flocking into this sector because of the value these stocks hold.”

This may already be starting to happen. Container shipping stocks are not falling to the extent they were in prior months. “It’s still very early days, but freight rate declines are less aggressive and people are wondering if this is in response to the blank [canceled] sailings we’re seeing and other counter-maneuvers liners are doing to support pricing,” said Nokta.

“It seems to be working. But whether it’s the long-term solution or will just last a couple of weeks or months, we’ll see. The jury’s still out.”

Click for more articles by Greg Miller

Related articles:

- Did US slash imports too much, setting stage for shipping rebound?

- Here’s how container shipping lines can escape a crash in 2023

- Shifting tides: The fall of container shipping stocks, the rise of tankers

- Container imports to Los Angeles and Long Beach are plummeting

- Container-ship logjams off US ports finally easing as imports fall

- Global trade at the crossroads: Risks from geopolitics, inflation loom

- US imports sink in September, suffer steepest drop since 2020 lockdowns

- Fall in container spot rates ‘much steeper,’ ‘less orderly’ than expected