The highlights from Monday’s SONAR reports. For more information on SONAR — the fastest freight-forecasting platform in the industry — or to request a demo, click here. Also, be sure to check out the latest SONAR update, TRAC — the freshest spot rate data in the industry.

After the first month of the year, the demand for trucks hasn’t slowed down one bit. There hasn’t been a dip in volumes since the beginning of the year and it likely won’t come this month as retailers prepare their spring and summer merchandise.

Capacity is still tight in most markets, spot rates are elevated to inflationary levels, and for what are usually the two calmest months of freight, we are seeing record high levels of volumes.

The snow storm essentially shutting down several Midwestern states will surely take a week for shipments to get back on track, which only exacerbates the problem.

As we move further into February, shippers need to remember to ship early and ship often. February has been known for major winter storms, and with market conditions as tight as they are, shippers should pay close attention to tender lead times in their area and ship as early as they can to maintain reasonable transportation spend.

Watch: Carrier Update

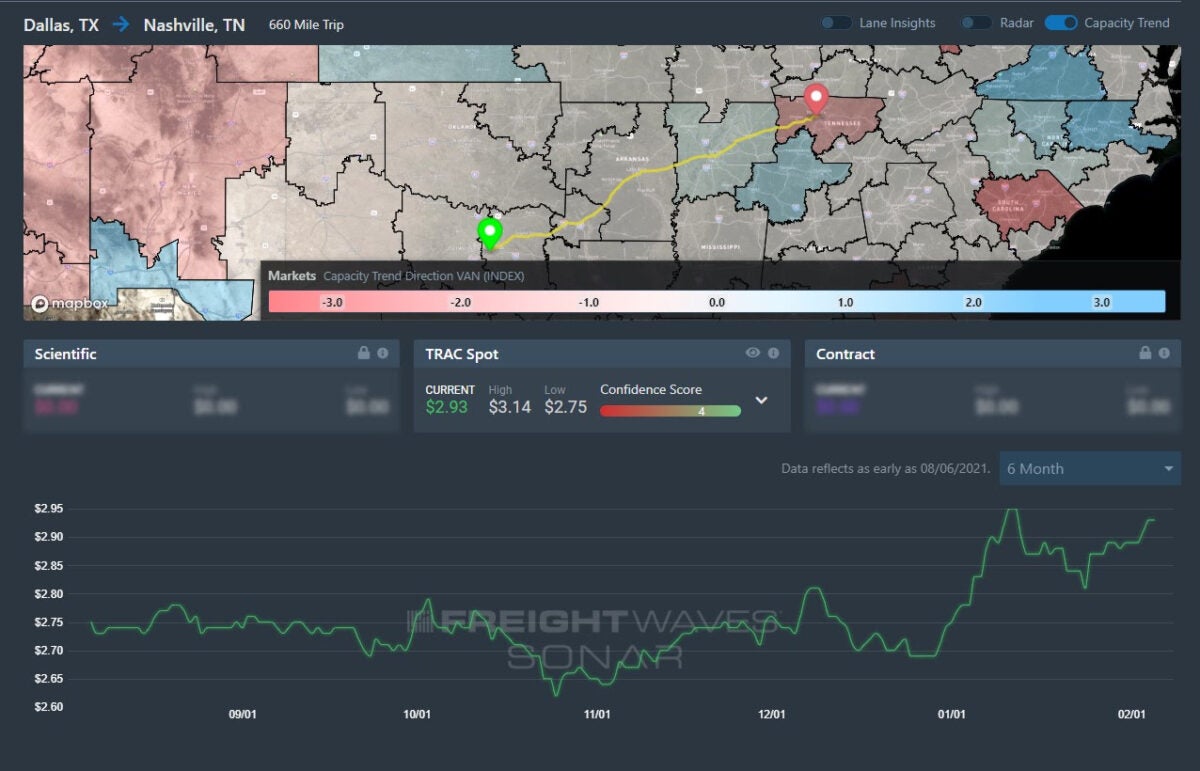

Lane to watch: Dallas to Nashville (Tenn.)

Overview: Spot rates rise amid increasing tender rejections in the Nashville market.

Highlights:

- FreightWaves TRAC spot rates have climbed to $2.93 per mile in the Dallas to Nashville lane, approaching the 6-month high rate of $2.95 per mile that occurred on Jan. 12.

- Outbound tender rejections for the Nashville market have increased to 26.4% amid volatility from winter weather systems and increasing outbound tender volumes.

- Outbound tender rejections from Dallas declined to 14.92% (a 6-month low) against a backdrop of elevated volumes, indicating more capacity entering the market.

What does this mean for you?

Brokers: Rising outbound tender rejections in Nashville and greater volatility represent a chance to take advantage of the price movements for greater margins. While committed freight may be priced lower, ad hoc opportunities should allow you to increase margins due to the rise in spot rates relative to tender rejections.

Carriers: Examine if extra capacity in the Dallas market can be used for spot quotes, as the rise in rates may create greater revenue opportunities compared to contractual commitments. Due to lower outbound tender rejection rates from Dallas and rising tender rejections in Nashville, there may be a chance to source with shippers directly for last-minute loads while providing cheaper rates compared to using a broker.

Shippers: Focus on tender compliance for both brokers and carriers, as contracted rates may remain lower than the recent surge in spot prices. Avoid last-minute shipments if possible and communicate with carriers and brokers regarding increasing tender lead times to reduce transportation costs and service disruptions.

Watch: Shipper Update

Lane to watch: Indianapolis to Elizabeth (N.J.)

Overview: Rejections spike out of Indianapolis after the winter storm.

Highlights:

- Indianapolis’ outbound rejection rate spiked from 25% to 28% last week after the city was hit by a strong winter storm. The rate began to stabilize slightly over the weekend.

- Rejection rates to Elizabeth increased similarly (but at a slightly lower level than the market). FreightWaves TRAC spot rates leveled off at $4.89 per mile.

- Elizabeth’s outbound rejection rates have fallen significantly over the past two weeks – from 20% to 15.6%.

What does this mean for you?

Brokers: Expect rates to stop increasing by late week as the market recovers from the winter storm. This lane was tightening prior to the winter weather, but there are early signs of stabilization.

Carriers: Divert capacity to the spot market in this lane with Elizabeth’s rejection rates dropping quickly. Rates should be well above $4 per mile, which should help pay for the declining reload potential.

Shippers: Consider a rate increase in this lane if your compliance levels are below 75% and your contract rates are well below the going spot rate. This lane is prone to numerous weather disruptions for the next few months and carriers still have plenty of options to move in more favorable directions.

Truckload capacity stabilized slightly last week as national rejection rates dipped briefly below 19% for the first time since mid-December. This was followed by a slight uptick as another weather system hit the Midwest with snow and ice.

Some of the impacts of this system will not be fully felt until next week as service delays work their way through networks, but by and large there were no significant large-scale changes to national capacity over the past week.

Weather should not play as big a role in influencing capacity over the next week because of a moderating trend in the forecast.

National imbalance will return as the biggest factor plaguing shippers’ compliance rates and keep capacity relatively tight. Demand remains steady with no sign of slowing.

Lane to watch: Harrisburg (Pa.) to Dallas

Overview: Rejections are likely to rise as the Headhaul Index surges 16% w/w.

Highlights:

- Harrisburg outbound tender volumes are up 7% w/w, signaling that demand for capacity is increasing.

- The Headhaul Index in Harrisburg is up 16% w/w, signaling that capacity is likely to tighten.

- Harrisburg outbound tender rejections are only up 75 basis points (bps) w/w, but expect them to increase due to the growing imbalance between inbound and outbound volumes.

What does this mean for you?

Brokers: You are likely to see capacity tighten significantly throughout this week. Outbound tender rejections are only up 7% w/w , but the increase of 16% w/w in the Headhaul Index is signaling that there are fewer trucks hauling freight into Harrisburg, so any further increases in outbound volumes (highly likely) will put greater pressure on capacity and spot rates.

Carriers: Harrisburg’s pricing power will be shifting further in your favor for the remainder of the week. If you have capacity in that market, you should increase your rates for the week. Most brokers and shippers are likely feeling capacity tighten, so stay firm on your rates and capitalize on your spot market opportunities.

Shippers: Your shipper cohorts in Harrisburg are averaging 3.3 days in tender lead times, but if the Headhaul Index continues to increase, you will need to have your tender lead times between 3.5 and 4 days to ensure that you are able to source capacity effectively during these tightening conditions.