The highlights from Wednesday’s SONAR reports. For more information on SONAR — the fastest freight-forecasting platform in the industry — or to request a demo, click here. Also, be sure to check out the latest SONAR update, TRAC — the freshest spot rate data in the industry.

Lanes to watch

By Zach Strickland, director, Freight Market Intelligence

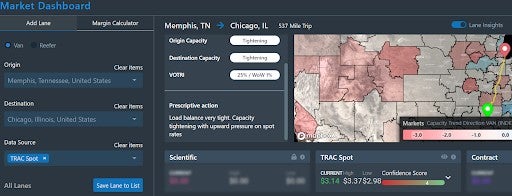

MEMPHIS to CHICAGO

Overview: Shippers should extend lead times as both origin and destination markets tighten.

Highlights

- The van tender rejection rate in the lane increased 427 basis points in the past two weeks to 24.8%.

- The van tender rejection rate in the lane is well below the 32.8% tender rejection rate for all van loads outbound from Memphis.

- The Chicago van inbound tender lead time rose from 2.5 days earlier in the month to 2.8 days in the past week as shippers have become more concerned about securing capacity during the week of Thanksgiving.

What does this mean for you?

Brokers: Prioritize covering loads in this lane given the current tightness in the Memphis market and a rising tender rejection rate for inbound Chicago loads. FreightWaves Market Dashboard shows that other brokers are paying an average of $3.14/mile, including fuel, in the lane with $3.37/mile and $2.98/mile representing buy-rates in the 67th and 33rd percentiles, respectively.

Carriers: Memphis is a tighter van market than most currently with a van outbound tender rejection rate of 32.8%. Therefore, before accepting tenders to Chicago, seek out highly rated spot loads.

Shippers: Extend lead times past the 2.8-day average for inbound Chicago loads as capacity tightens. Not only is capacity more challenging to secure during the holiday week, but Chicago has become less of a Headhaul market which may make securing inbound Chicago capacity more challenging (Chicago Headhaul Index declined from 90 in late October to 52 currently).

ONTARIO (California) to DALLAS

Overview: Capacity likely to get tighter as truckload volumes head towards their peak for 2021.

Highlights

- Ontario outbound tender volumes are up 15% week-over-week (w/w), but with massive import volumes still inbound, the upward trend is expected to continue.

- The Headhaul Index in Ontario is up over 78% w/w, signaling that capacity is likely to tighten in the coming days as volumes become increasingly imbalanced.

- Ontario outbound tender rejections are already up 253 bps w/w, and are likely to rise higher in the coming days.

What does this mean for you?

Brokers: Outbound volumes are up 15% w/w, and are expected to continue increasing as port volumes continue getting transitioned from containers to the truckload market. Even though rejections are already up 253 bps w/w, the major increase of over 78% in the Headhaul Index is a signal that rejections are likely to move even higher in the coming days. Already, spot rates to Dallas are moving higher, and the surge of volumes is not over yet.

Carriers: The surge w/w in the Headhaul Index is likely to continue causing a significant tightening in capacity. Outbound volumes are booming and could break a record high for the year. For those reasons, stay firm on your rates while keeping an eye on outbound tender rejections.

Shippers: Your shipper cohorts in Ontario are currently averaging 2.6 days in their outbound tender lead times, and have been steadily increasing them over the last few weeks. However, 2.6 days is not likely to be enough time as outbound volumes head towards their peak for 2021. Historically, 3.5 to 4 days has been the target to help offset extremely tight conditions.

ATLANTA to CHICAGO

Overview: Atlanta capacity eases into Thanksgiving break.

Highlights:

- Atlanta’s outbound rejection rate has been in steady decline since late June, falling from over 30% to near 16% over the past five months.

- Rejection rates to Chicago have followed a similar pattern until the past two weeks when rates bounced from 17.5% on November 10 to over 20% currently. This uptick has had no impact on spot rates as they have been hovering around $2.69 per mile for the past week, but with a relatively wide range according to FreightWaves TRAC.

- Chicago’s outbound rejection rates have been moving higher over the past month, increasing roughly 3 percentage points over this time.

What does this mean for you?

Brokers: Expect a slight uptick of spot volume for loads moving after the holiday with spot rates flat to lower. Atlanta is easing and this lane is stabilizing outside of the service sensitive freight. Rates above $3 per mile should be a rarity for standard freight.

Carriers: Divert more capacity to cover contract freight in this lane. Chicago is tightening while Atlanta is easing. Reload potential is on the rise out of the midwestern hub and spot rates are also on the climb unless the freight is moving back to Los Angeles.

Shippers: Expect easing conditions in this lane outside of the holiday and service critical impact. Some slight decline in compliance is evident, but not nearly as drastic as it has been in previous holidays this year thanks to easing aggregate demand and increasing lead times.

Watch: Tender rejection rates

Passport Research on … US import demand

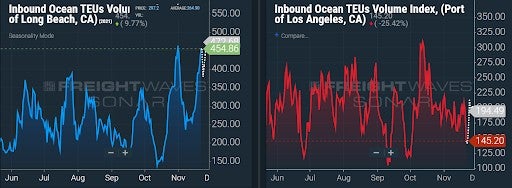

In the most recent week, the Port of Los Angeles reported normalizing levels of TEUs being processed within the nation’s busiest port. The port reported just north of 467,000 TEUs for the month of October, an 8% decline from October 2020. The ports of LA and Long Beach combined for 852,000 TEU during the month, down 13% from peak levels experienced back in May.

In the next seven days, volumes departing from any country of origin to the ports of LA and Long Beach seem to be trending in different directions. Coming off of the mid-October booking spike, the Port of LA has experienced stabilizing and seasonally normalized levels of confirmed TEU bookings set to depart their port of origin. On the other hand, the Port of Long Beach has continued to trend upward from October’s spike, stabilizing in the next seven days at near- record levels.

Despite October’s subdued volumes to the ports, vessels at anchor within San Pedro Bay continue to trend at above 80 container vessels per day, with around five vessels arriving daily. Equipment shortages and domestic capacity limitations continue to plague port throughput within the San Pedro Bay complex, further extending waiting times for container vessels. The average time from anchorage to berth for vessels calling upon the Port of Los Angeles has continued to trend upward, now at nearly 19 days.

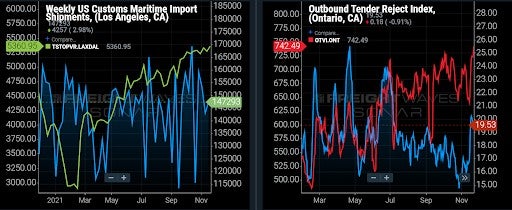

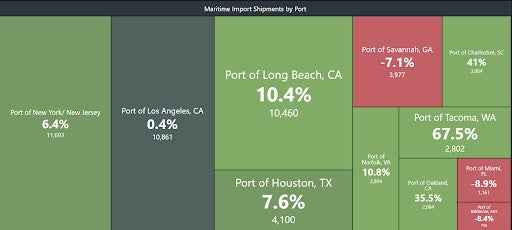

Extended wait times at the ports of Los Angeles, Long Beach and Savannah continue to call for shippers to divert their ports of entry to mitigate any disruptions. In the last week, ports within close geographic proximity to the San Pedro Bay port complex have seen a significant uptick in maritime shipments clearing U.S. Customs. The ports of Tacoma, Washington and Oakland, California have now seen consecutive weeks of double-digit growth, as they remain key relief valves for shippers looking to divert from congestion and still service domestic supply channels along the West Coast.

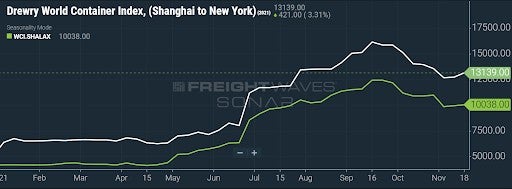

Despite showing some relief to shippers in recent weeks, eastbound maritime trans-Pacific spot rates have begun to move away from their downward trend. Spot rates per 40’ container, according to the Drewry World Container Index, have now experienced two sequential weeks of increases, signalling that a fall from sky-high ocean spot rates is still in the not-so-distant future. The index’s Shanghai to New York assessment has ticked back up to $13,139/FEU, a 3% increase from the previous week and now up 164% y/y. The Shanghai to Los Angeles assessment, which had fallen below $10,000 for the first time since July, jumped back to $10,038/FEU, a 1% w/w increase, putting the index up 149% y/y. Even with stabilizing levels of U.S. imports, clogged ports continue to plague available vessel capacity, mitigating any form of rate relief for heavily impacted spot shippers.

This post originally appeared in a Passport newsletter. Sign up here

Watch: What are predictability models?

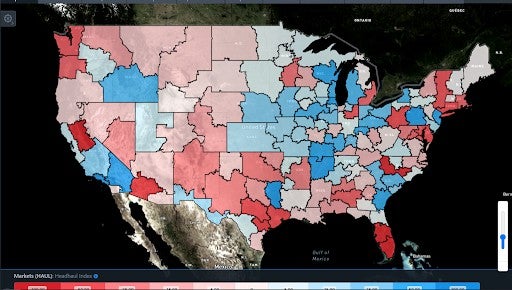

Focus on … Headhaul Index map

By Zach Strickland

The Headhaul Index (HAUL) shows the strongest outbound markets are positioned around the nation’s largest ports.

Southern California, Elizabeth, and Savannah all show having a strong outbound freight flow in relation to the inbound flow.

Rates tend to be higher out of these markets versus the inbound heavy markets, represented by the darker shades of red.

The Chicago area markets have had significant growth in HAUL values over the past few months, which has pushed spot rates higher. The Atlanta market has fallen into a negative HAUL value, leading to lower outbound rates.

The Headhaul Index is calculated by subtracting the In bound Tender Volume Index (ITVI) from the Outbound Tender Volume Index (OTVI).