The quarterly call of DHT Holdings (NYSE: DHT) was easy listening for its investors. Not so for stockholders of DHT’s competitors, which are much more exposed to spot rates.

DHT, unlike almost all other public crude-tanker owners, is heavily shielded from spot downside by time charters. Now, it’s prepping to buy tankers as spot rates slump, ship values fall, and owners without period coverage get hammered.

“We expect the next leg in the market to have attractive investment opportunities,” DHT co-CEO Svein Moxnes Harfjeld said on Tuesday — a polite way of saying there’s pain ahead for other owners.

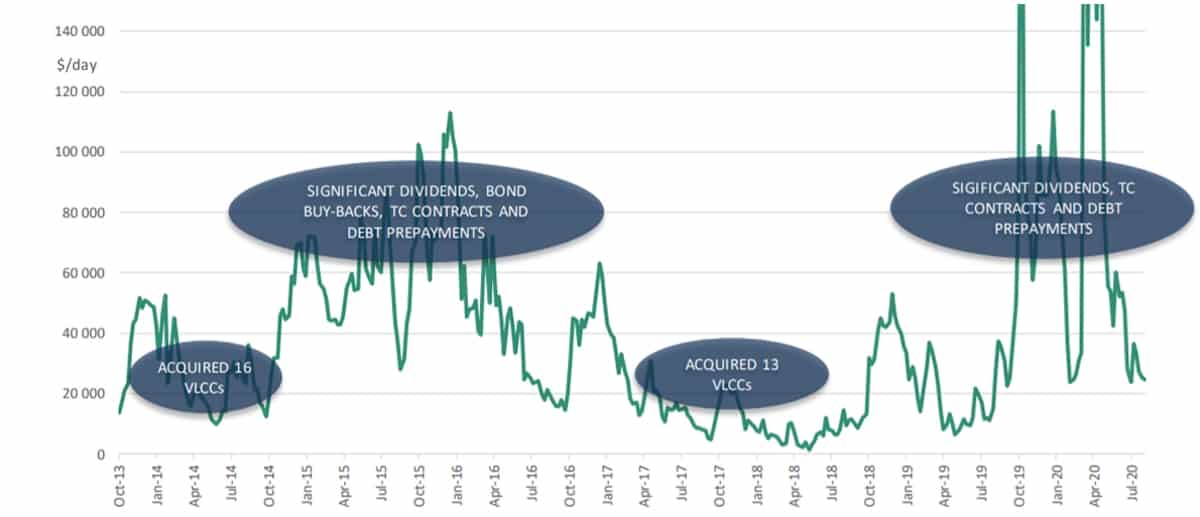

DHT behaves in a predictable countercyclical pattern: When markets are bad, it starts buying. It bought 16 very large crude carriers (VLCCs; tankers that carry 2 million barrels of crude oil) from Samco during the 2014 rate trough and an additional 13 from the BW Group in the 2017 downcycle.

“We haven’t been in investment mode now for three years,” Harfjeld continued. DHT is back in buying mode, albeit in no rush. “We still think it may be a bit early. This might be a next-year event,” noted Harfjeld.

Because DHT has time charters on 10 of its VLCCs, its remaining 17 VLCCs in the spot trade only have to earn $2,800 per day for the company to break even for the remainder of this year. They only have to earn $11,400 per day to cover cash costs next year. Current rates are $22,500 per day.

“If you look over the past 25 years, the worst three years had average earnings of about $18,000-$19,000 per day. And those were extremely bad years. We’re not suggesting that’s representative of what’s to come. But even in that market, we would generate cash,” said Harfjeld.

Newbuildings are not off the table

“One key parameter to look at is the yards,” he continued. “In general, they have very, very little business. That might drive them to reduce their pricing and that would also impact opportunities for secondhand ships. That’s what we really need to watch carefully now.”

Asked whether newbuilds are an option, DHT management did not dismiss the possibility if the price is right (it isn’t yet).

“In the past, we have done M&A [mergers and acquisitions]. We have done newbuilds. We have picked up distressed assets. It could be a mix of those things,” said Harfjeld, who stressed, “Again, we are not ‘trigger eager’ right now.”

“Another aspect [of the next investment] is there will be some sort of fleet renewal,” added DHT co-CEO Trygve Munthe. “The preference clearly will be ships built since 2015 or [newbuild] resales. We’re not buying 18-year-old ships and gambling on an immediate spike in freight rates.”

Preparing for the next step

That rate weakness could persist well into next year and that yard rates could fall low enough to spur orders are not pleasant prospects for tanker-stock investors.

DHT’s call comments were not necessarily a new warning on market conditions. Harfjeld said they were meant “to explain why we have done the things we’ve done [time charters, debt repayments] to prepare for what we expect will be the next significant activity in the company.

Rates could unexpectedly rise. “Our industry is not only cyclical. It is also very volatile and impacted by curveballs and political decisions. It is very hard if not impossible to have credible rate predictions. The way we manage DHT is to be able to withstand any tough market without giving away the upside.”

Last week’s quarterly call by crude-tanker owner Euronav (NYSE: EURN) similarly highlighted the need to prepare for M&A.

“We don’t have a shopping list,” said Euronav CEO Hugo De Stoop. “You don’t have a target fleet because that’s not how the market works. Some people suddenly change their position and decide to sell their fleet. And it comes onto your desk. And when you have the capacity and the management time to act upon those opportunities promptly, you can seize those opportunities.”

In the past few days, potential consolidators have been publicly lining up, with Star Bulk (NASDAQ: SBLK) on the dry side and Euronav and now DHT on the tanker side.

Record quarterly results

DHT reported record results: net income of $135.8 million for the second quarter of 2020 (Q2 2020) compared to a net loss of $10.5 million in Q2 2019. Adjusted earnings per share of 83 cents were in line with Wall Street consensus.

DHT’s spot VLCCs earned $92,100 per day in Q2 2020 and its time-chartered VLCCs earned $62,700, for a blended average of $83,000 per day.

So far in Q3 2020, the company has booked 61% of its spot days at an average of $51,400 per day. Including time charters, DHT has 75% of 3Q 2020 available days booked at $51,200 per day.

DHT is “really managing the cycle well,” affirmed Evercore ISI analyst Jon Chappell. “Indeed, DHT is the only tanker company for which we presently forecast a profit in 2021.” Click for more FreightWaves/American Shipper articles by Greg Miller

MORE ON TANKERS: How are tanker owners coping with the floating-storage hangover? See story here.Tanker rate puzzle gets even harder to solve: see story here. How badly did tanker stocks perform in the first half? See story here.