Following dismal first-quarter results, heads of two of the nation’s largest truckload fleets provided constructive market commentary at a Wednesday investor conference. That said, the long slog back to market equilibrium continues as the industry slowly purges the excess capacity added during the freight boom.

“By no means am I here saying I think we’re at a turning point or an inflection point, but I do believe, just like it took a long time to get this low and we stayed this low for this long, it’s taken us awhile to maybe pick up on some of the signals that are out there in front of us that seem to be more positive,” said Derek Leathers, chairman and CEO of Werner Enterprises (NASDAQ: WERN), at Wolfe Research’s annual transportation and industrials conference in New York.

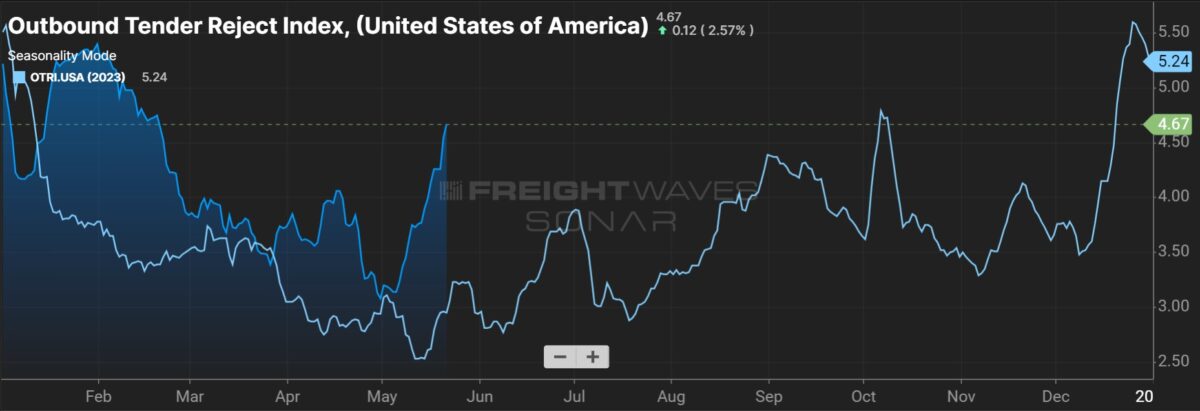

Leathers pointed to a notable decline in the number of trucks posted on load boards during the past two months and a more normal tightening in capacity during International Roadcheck, an annual 72-hour inspection blitz by law enforcement, held last week. He also said recent customer conversations have been positive and that all the discount retailers Werner serves under dedicated contracts have increased their truck counts this year.

Mark Rourke, Schneider National’s (NYSE: SNDR) president and CEO, said the company has been able to capture low-single-digit price increases on contractual renewals in its one-way TL business.

“We think that’s some place that we can build upon as we get through the rest of the allocation season,” Rourke said.

He noted that some of the price increases corresponded to lost share within certain customer accounts but that overall, the company has been able to positively navigate bid season thus far. Schneider has completed roughly 40% of its one-way contractual negotiations this year.

Werner has seen some price renewals move higher but “not across the board.” However, it is seeing less pressure from shippers to reduce rates, a decline in customer churn and improved bid compliance for previously awarded freight.

“This time around, we’re not seeing that same level of dislocation,” Leathers said. “We signal with pricing what we want to retain, and we’ve been able to do it.”

Werner’s bid season will be half-complete by the end of the second quarter.

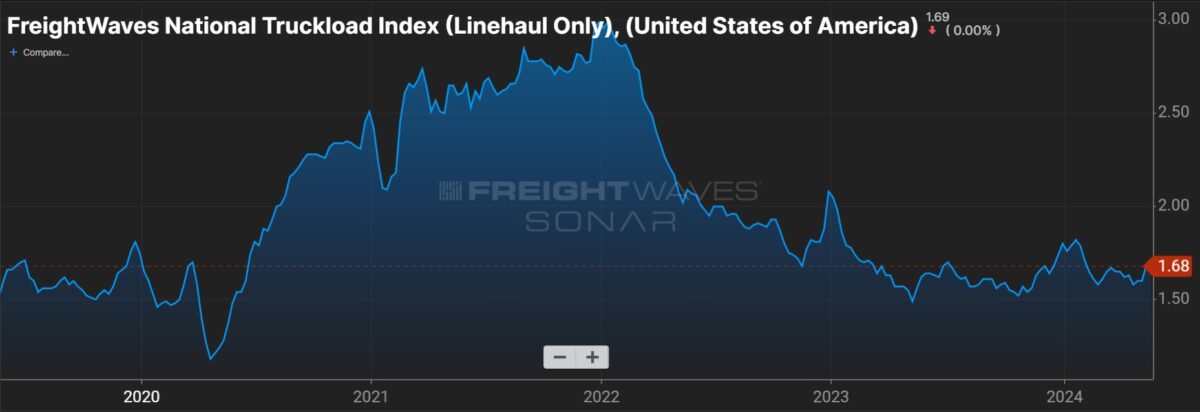

The company reiterated rate guidance when it reported first-quarter results on April 30. It expects revenue per total mile in the one-way segment to be down 6% to down 3% year over year (y/y) in the first half of the year, with revenue per truck per week in the dedicated unit flat to up 3% y/y for the full year.

Leathers said most spot freight is on load boards and not reflective of the drop-trailer and other engineered solutions the big carriers offer. As such, he doesn’t think contract rates need to reset lower than spot rates for the cycle to turn.

“I don’t think that you’ll need to see spot supersede contract to see it become meaningfully obvious that this market has turned,” Leathers said.

Both carriers have more than 60% of their trucking assets placed under contractual dedicated agreements.

Asked about margin improvement, Leathers said Werner likely won’t see a “pronounced step up” in margins from the first to the second quarter as previously renegotiated rates are still being implemented on some business. However, he expects margins to improve throughout the year, noting that recent utilization increases (one-way miles per truck up 11% y/y during the first quarter) have come on the downside of the rate cycle, implying favorable leverage when the market turns as the higher level of miles garners better rates.

He said the dedicated fleet also has leverage when demand improves as truck counts will increase on a per-account basis. Additions to existing fleets already operated by Werner won’t accompany incremental startup costs.

Rourke expects operating margin improvement throughout the year even if the market doesn’t improve. He said the company’s long-term TL margin target of 12% to 16% remains but noted it may take awhile to get there on a full-year basis. He said Schneider will be “much, much closer” to the target run rate next year.

Schneider posted a 97.2% adjusted operating ratio (inverse of operating margin) during the seasonally weakest first quarter. That will likely prove the trough for this cycle.

Werner’s 12% to 17% long-term adjusted operating margin guidance also remains intact, but Leathers sounded a little less optimistic about hitting that range by year-end as previously hoped. The company’s 95.3% adjusted TL OR in the first quarter was also a cycle worst.

Both companies see an opportunity for large, transformational acquisitions.

Rourke said the M&A market should improve into the back half of the year and that it could take on something on a “much broader basis than [the] $200 to $250 million acquisitions” it has executed in recent years.

Leathers said he expects to see more consolidation among freight brokers. He also said “larger is actually not harder” when it comes to acquisitions, and that Werner may pursue a larger deal with robust integration synergies.

Shares of WERN closed up 2.4% on Wednesday while shares of SNDR were up 3.4%. The S&P 500 was down 0.3% on the day.