Year-over-year (y/y) declines in freight shipments and spend continued to taper during December, according to data compiled in the Cass Freight Index.

December shipments outperformed normal sequential seasonal changes, up 2.1% seasonally adjusted. That followed a 0.3% sequential increase in November. Compared to a year ago, volumes captured by the data set were off 7.2%, which was 170 basis points better than the rate of decline in November.

Stripping out seasonal adjustments, December was weak with the shipments index at its lowest absolute level since July 2020 and 10.8% lower than it was in December 2021. If normal seasonal patterns hold, volumes are forecast to decline 8% y/y in January.

| December 2023 | y/y | 2-year | m/m | m/m (SA) |

| Shipments | -7.2% | -10.8% | -1.6% | 2.1% |

| Expenditures | -23.7% | -26.9% | -3.0% | 0.1% |

| TL Linehaul Index | -6.1% | -4.5% | 0.4% | NM |

The expenditures subcomponent, which measures all dollars spent on freight (including fuel surcharges and accessorials), was down 3% from November but basically flat when seasonally adjusted. The data set was 23.7% lower y/y, marking the seventh straight month of mid-20% declines.

For all of 2023, expenditures were down 19% y/y, but that change rate followed increases of 23% and 38% in 2022 and 2021, respectively. The index is expected to be down an additional 14% in the first half of 2024.

Netting the decline in shipments from the decline in expenditures implies actual freight rates, or “inferred rates,” were off roughly 18% y/y. Inferred rates are expected to decline 11% y/y in the first half of the year.

Spending on truckload shipments accounts for more than half of all dollars recorded in Cass’ expenditures index.

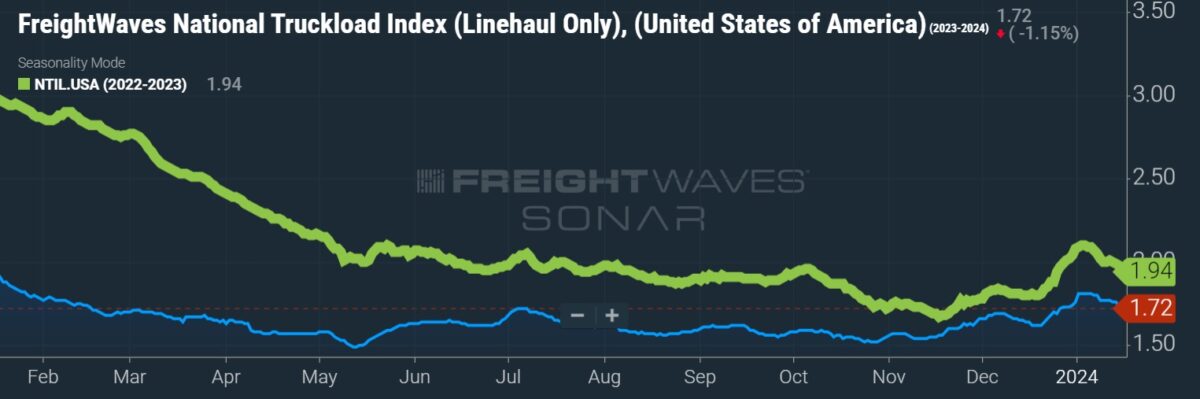

Cass’ TL linehaul index provides a cleaner look at TL rates as changes in fuel and accessorial charges are excluded. The index inched 0.4% higher from November to December, which was just the second sequential increase in 19 months. The index was down just 6.1% y/y, the smallest decline since February.

Cass’ linehaul rates have continued to stabilize, with the index now on par with August and just 1% lower than May. The index captures both spot and contract rates.

“With spot rates steady over the past several months, downward pressure on the larger contract market is lessening, with some instances of contract rate increases bucking the downtrend of late,” stated ACT Research’s Tim Denoyer in the report.

While rates are stabilizing at lower levels, truck capacity remains high. But carrier exits are increasing.

Carrier exits totaled 4,860 in December, which was 52% higher than the average monthly level of closures recorded during 2023, according to data from fleet solutions provider Motive. New registrations were down for a fourth straight month at 6,503. That put December registrations 18% lower y/y and 43% below December 2021.

Total new registrations in 2023 were 21% higher than in 2019, which was also a down year for the industry.

“Destocking and declining goods consumption have been key features of the freight recession, but both cycle drivers seem to be starting to reverse course,” Denoyer said. “Real retail sales recently turned positive after a year of declines, and after 18 months of destocking, a restock is drawing near, likely spurred by ocean risks — [conflict in the Red Sea and low water in the Panama Canal].”

Data used in the Cass indexes is derived from freight bills paid by Cass (NASDAQ: CASS), a provider of payment management solutions. Cass processes $44 billion in freight payables annually on behalf of customers.

More FreightWaves articles by Todd Maiden

- Court OKs second Yellow terminal sale; liquidation only half complete

- PS Logistics acquires flatbed, dedicated hauler Buddy Moore Trucking

- Morgan Stanley sees inventory restock producing freight upcycle soon