A predictive rate index released Tuesday showed truckload pricing “tumbling” further in the second quarter while less-than-truckload rates stabilize from a “sharp drop” in the first quarter.

The TD Cowen/AFS Freight Index — a compilation of data from third-party logistics provider AFS Logistics and investment bank TD Cowen (NYSE: TD) — showed excess truck capacity and soft demand had carriers competing for loads, driving rates lower during the first quarter.

The index captures trends from AFS Logistics’ freight audit, payments and transportation management platform that sees more than $11 billion in transportation spend across all modes annually.

Per-shipment linehaul costs were down 13.8% sequentially during the first quarter, 19.1% lower year over year (y/y). This was the first y/y decline recorded by the index since the third quarter of 2020. The spread between costs and miles per shipment has been narrowing since the second quarter of last year, “a strong indication that carriers are using rates as a primary tool to gain volume,” the report said.

Costs were also impacted by a shift toward shorter-haul shipments. The mix of local loads in the quarter increased 3.4 percentage points to 81%. The mix change may be indicative that shippers’ efforts to rightsize inventories are working.

“A greater share of short-haul shipments could indicate normalizing inventory levels and placement, with businesses no longer so desperate for inventory that they pay for longer, less-efficient shipments to move loads,” said Andy Dyer, president of transportation management at AFS.

A survey of shippers released Monday by Morgan Stanley (NYSE: MS) also highlighted similar inventory trends. The number of respondents saying they would maintain current inventory levels increased 10 percentage points to 38%. The report showed a decline in the number of shippers saying they needed to draw down merchandise levels for the first time since the third quarter of 2021.

However, Dyer countered that demand for many goods, especially consumer durables, may not be poised to improve as “interest rate hikes and inflation continue to impact purchasing power.”

Looking forward, the TD Cowen/AFS index for per-mile TL rates is expected to fall 13.1% y/y in the second quarter to just 6.6% above the index’s January 2018 baseline. That’s a modest step down from the 7.5% level recorded in the first quarter but a steep decline from 22.8% (above the baseline) during the 2022 second quarter.

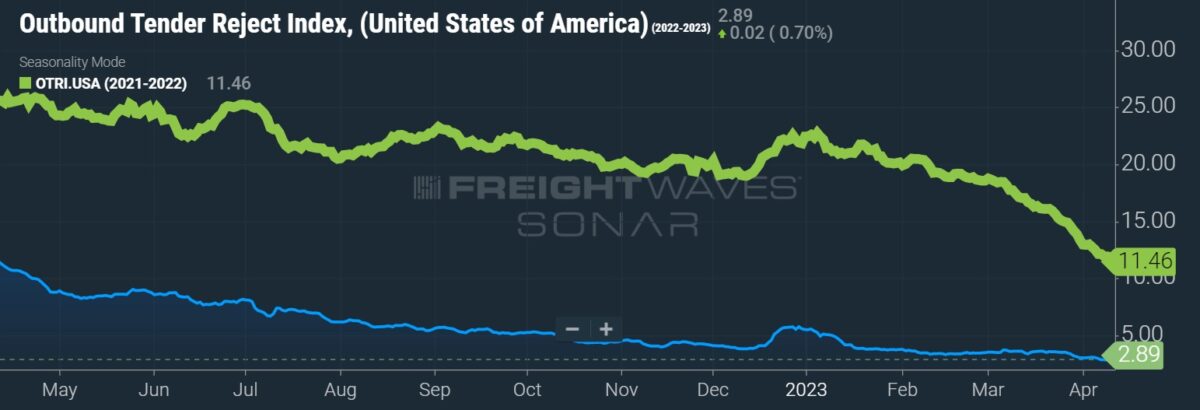

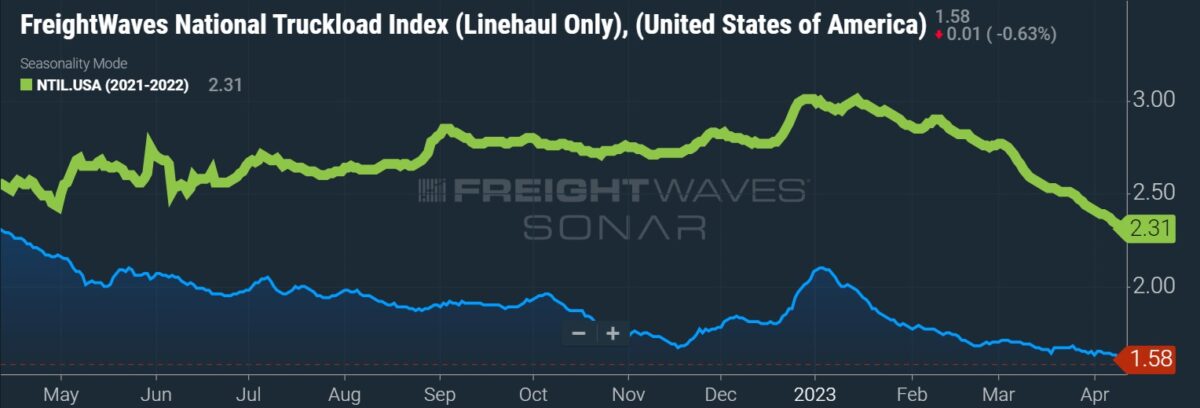

Lackluster TL trends continue to be seen across FreightWaves data sets as volumes, tender rejections and spot rates have yet to inflect positively.

Outlook for LTL, parcel more subdued

LTL rates fell at the fastest pace recorded by the index in the first quarter.

The rate-per-pound index fell 7 percentage points from the fourth quarter to 57% above the January 2018 baseline. Declines in fuel prices, additional capacity and the highest-ever comp established in the fourth quarter were the primary reasons for the drop. The index was essentially flat y/y.

Cost per shipment was down 4.6% from the fourth quarter as fuel costs paid by shippers were down 15.7% and weight per shipment was flat. On a y/y comparison, LTL cost per shipment was up 5.4%, the lowest increase recorded since 2021.

Looking forward, the rate index is expected to step up 130 basis points in the second quarter, with prices 58.3% higher than the 2018 baseline. However, even with the expected sequential increase the index is expected to be negative y/y.

“As carriers look to fill excess capacity and maintain revenue, prudent shippers can find major cost saving opportunities by looking beyond traditional LTL services,” said Kevin Day, AFS Logistics’ president of LTL. “Volume LTL is a tool for carriers to get some incremental revenue out of backhaul lanes that would otherwise have them moving empty trailers, while giving shippers the opportunity to take advantage of significantly lower rates and avoid the added sting of steep accessorial charges.”

The report showed that ground parcel rates were up 4% sequentially in the first quarter on higher package weights. Fuel surcharges are outpacing the actual declines in fuel prices. The implementation of multiple fuel surcharges last year along with general rate increases were credited with keeping yields up. Also, the current mix has more small and misize shippers, which do not get the same discounts large shippers do.

Ground parcel rates expected to step 1.7% higher sequentially in the second quarter to 31.7% above the 2018 baseline.

Express parcel rates were up 4.6% from the fourth to the first quarter and are expected to increase 1.1% sequentially (4.6% above the baseline) in the second quarter. The report said express parcel rates will be reflective of the volume declines the industry’s largest parcel carriers are seeing.

More FreightWaves articles by Todd Maiden

- Morgan Stanley sees freight upcycle nearing

- Forward Air adds drayage outpost to serve Port Newark

- ArcBest names new CFO