Ranked 39th on the Transport Topics list of top brokerage firms, Axle Logistics takes a consultative and streamlined approach to your shipping needs. Email sales@axlelogistics.com to connect with the team today!

Retail rout

This week saw a rout in retail stocks with shares of Walmart and Target down 21% and 31%, respectively, during the past five trading sessions. The retailers have January fiscal year-ends so the just-reported quarter includes February-April, a period that had more than its share of challenges between the ingredient inflation that was exacerbated by the Ukraine invasion and the historic run-up in fuel prices. What surprised the Street was the degree to which the rapid increase in costs, and the shift in consumer spending to lower-margin categories, led to margin contraction and reduced profitability.

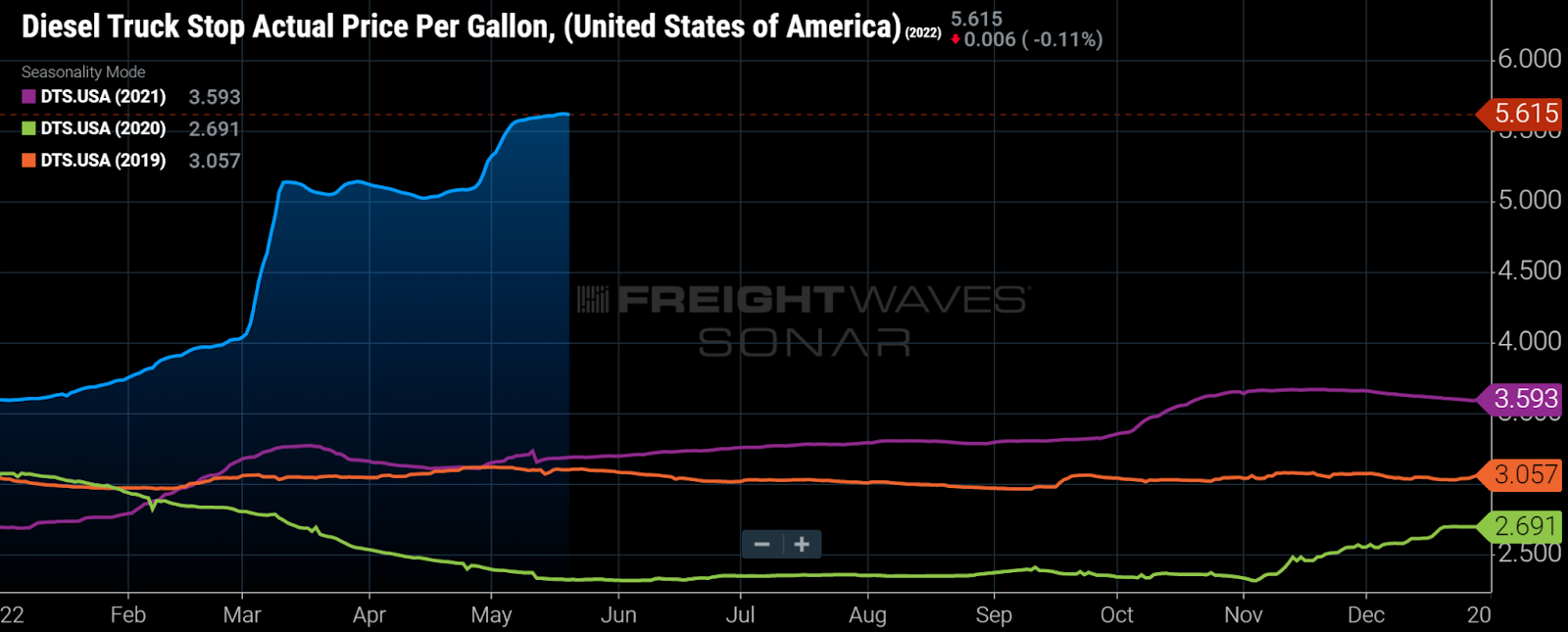

That has caused many observers to ask, as if they knew six months ago that diesel prices would hit $5.62 a gallon in May, “How could the largest retailers be surprised by these trends?” Basically, cost pressures escalated very quickly, and it takes time for retailers or other large companies to fully mitigate price shocks through a combination of efficiency gains and passing on costs. Still, Target’s operating income margin of 5.3% was dismal compared to 9.8% a year ago.

Inventories are very heavy, but not for food

Walmart and Target had inventory levels at the end of the quarter that were 33% and 43% higher than a year earlier, respectively. Those data points support the thesis that a freight demand slowdown is coming. At first glance, they also seem to support a thesis that inflation pressures may ease, and Walmart said it intends to cut prices (rollbacks, as they call them) to thin out bloated inventories.

But those thoughts pertain to general merchandise, which is largely discretionary, and not to food and consumable products. Food and consumables remain highly inflationary due to the cost of ingredients, materials and fuel, which retail prices do not yet fully reflect. That is consistent with a comment from Walmart management on its earnings call — it doesn’t expect inflation to ease in food. So, inflation may ease on products that consumers don’t really need while rising on products they do need. Clearly, CPGs would prefer that inflationary pressures ease in consumables so there is time for prices in contracts with retailers to catch up to CPG companies’ cost pressures, but that doesn’t seem likely near term.

Higher food prices really are crowding out discretionary purchases

Just looking at overall revenue and same-store sales posted by Walmart and Target, one would think that the consumer is still healthy and confident. But the detail reveals that consumers haven’t really spent less at the store. It’s just that after buying essentials, there was less for other items. Whether one wants to call those other items general merchandise, consumer-discretionary or just random crap, consumers are buying less of them.

That’s bad news for retailers because, just like traditional grocery stores, food has thinner margins than nonfood items. For CPG companies, the picture is more complicated. Consumers, by and large, cut back on nonconsumables before they cut back on CPG items. But a slowdown in buying power will eventually make its way to the more discretionary subsegments of CPG.

Consumer behavior varies widely by demographic

Walmart has seen more trading down to private-label brands in the past quarter. Target has seen consumers cut back on hardlines, a segment that includes discretionary categories, such as furniture, appliances and electronics. Yet Walmart is still seeing strength in big-ticket products like video game consoles and some seasonal and discretionary merchandise like grills and patio furniture. I don’t consider those statements to be contradictory. Inflation in food and energy hits lower-income consumers and those on a fixed income the hardest. As a result, the CPG companies likely to weather the current economic conditions the best are those that cater to affluent consumers. Categories that fit that description include health foods, vitamins and fresh pet food.

Discount and big-box retailers could become bigger players in grocery

The trading down that Walmart is seeing to private-label brands also suggests that Walmart is likely to take share from traditional grocers as consumers look for ways to mitigate rising food prices. On its earnings call, Walmart made clear that it intends to remain a low-price leader, where it maintains a competitive advantage due to its scale and logistics capabilities. That could present a challenge for CPGs if they see a sales mix shift toward big-box, because no one negotiates harder than Walmart.

Labor headaches aren’t just about worker shortages anymore

At times, Walmart had too many workers because too many decided to return from their COVID-related hiatus at the same time. Rather than terminating excess employees, the company managed headcount lower through attrition.

Freight costs remain a headwind

For all the discussion of falling truckload spot rates and weakening fundamentals in the truckload industry, freight costs remain a headwind for large contractual shippers, even before considering the massive run-up in fuel prices. Walmart noted that three-quarters of its gross profit decline was due to higher-than-expected supply chain costs, including fuel and e-commerce fulfillment.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, please click here.