Less-than-truckload carrier Yellow Corp. booked operating and net losses in the first quarter as it remains hopeful of working out a deal with its union employee base.

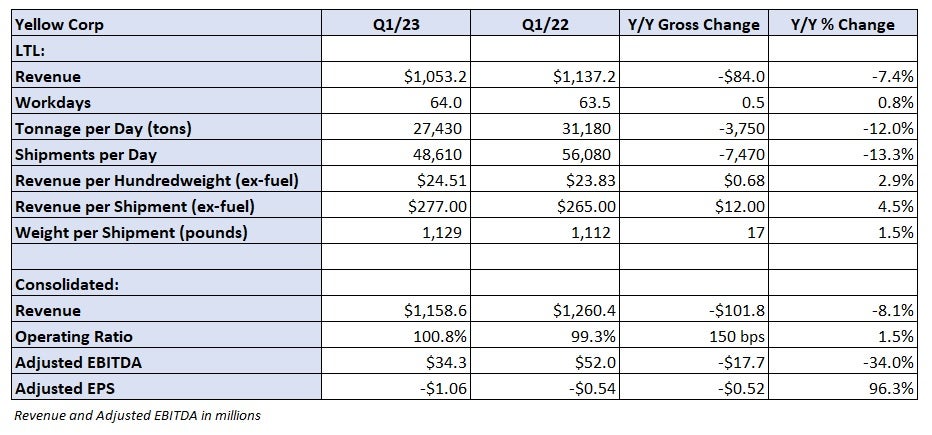

Yellow (NASDAQ: YELL) reported a first-quarter net loss of $54.6 million, or $1.06 per share, Wednesday after the market closed. The result was 22 cents worse than the consensus estimate and nearly double the loss booked in the year-ago quarter. An increase in interest rates pushed interest expense $8.8 million higher even though total debt was reduced by $98 million.

Management said costs associated with a companywide restructuring dubbed “One Yellow” weighed on results. The overhaul includes the consolidation of its regional carriers onto one platform as well as eliminating redundant terminals in some markets.

The first phase included 20% of its network and was implemented at YRC Freight and Reddaway facilities in the West last year. The second phase impacts roughly 70% of Yellow’s coverage map at YRC Freight, Holland and New Penn terminals in the Midwest, Northeast and Southeast. However, the Teamsters union has rejected those proposed changes. The two parties instead have agreed to reopen their labor contract a year early in hopes of finding common ground.

“It is imperative that we complete our One Yellow strategy, which will strengthen the Company, protect 22,000 union jobs and ensure that our customers are well cared for and receive the range of services that today’s market demands,” CEO Darren Hawkins stated in a news release.

Management said residual costs from the first phase and expenses incurred planning the second phase contributed to an operating loss in the quarter. Yellow recorded costs repositioning employees and equipment, the latter of which totaled between $4 million and $6 million.

Yellow posted a 100.8% operating ratio (inverse of operating margin),150 basis points worse year over year (y/y). Most expense lines were up as a percentage of revenue. However, purchased transportation expense declined 160 bps y/y.

Total LTL revenue was down 7.4% y/y to $1.05 billion. Tonnage was down 12% y/y, which was the combination of a 13.3% decline in shipments partially offset by a 1.5% increase in weight per shipment.

Management noted that demand remains soft and that there was no seasonal uptick in the last few weeks of the quarter. Further, the weak trends carried into April, which saw tonnage down 16% y/y.

On a two-year stacked comp, Yellow’s tonnage was down in a mid-20% to mid-30% range for each of the first four months of the year. The declines are due to the restructuring as well as efforts to raise yields and ultimately its financial performance.

Typically, the carrier sees a 6% sequential increase in tonnage from the first to the second quarter, but with the muted results in March it likely won’t achieve that result this year.

Revenue per hundredweight, or yield, was up 2.9% y/y excluding fuel surcharge revenue. The metric was down 3.5% from the fourth quarter, but a 2% increase in weight per shipment was a drag on the calculation.

Revenue per shipment (excluding fuel) was 4.5% higher y/y in the period.

Year to date, contractual renewals are up between 2% and 3% y/y.

The company normally sees between 300 bps and 400 bps of margin improvement sequentially in the second quarter. Weakened demand, an approximately 3% wage increase in April and moderating contractual rate increases will reduce the improvement this year. Lower fuel surcharge revenue will also be a headwind.

Management said full-year 2023 union wages and benefits increases will be 4% to 5%.

Total liquidity declined 40% y/y to $167.5 million as cash was used to pay down debt.

The company’s lone debt covenant — adjusted earnings before interest, taxes, depreciation and amortization of at least $200 million over the past 12 months — was met in the quarter as it generated $325 million in adjusted EBITDA. However, the carrier has generated just $89 million in adjusted EBITDA over the past six months.

Management said once it comes to terms with the Teamsters and finishes the restructuring, it will look to again refinance its capital structure. The bulk of its $1.5 billion in debt matures next year.

“At the end of the day, I’m confident in this process because both sides are determined to get a deal done that works for everyone involved,” Hawkins said.

Shares of Yellow were off 2.9% in after-hours trading on Wednesday.

More FreightWaves articles by Todd Maiden

- Teamsters add seat on Yellow’s board

- Yellow, Teamsters to hash out operational changes by reopening NMFA early

- Teamsters tell Yellow no more purchased transportation