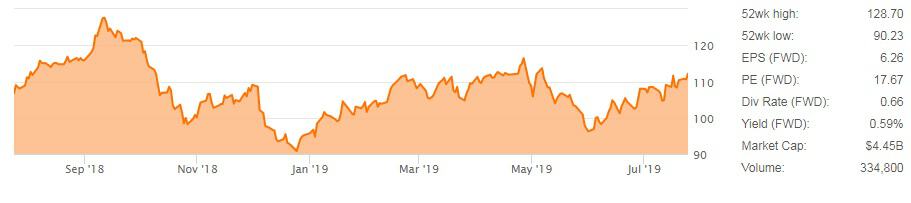

Landstar System, Inc. (NASDAQ: LSTR) reported second quarter earnings per share (EPS) of $1.53, in-line with analyst expectations and $0.02 higher than the 2018 second quarter.

However, this result was worse than the company’s initial second quarter 2019 guidance, which called for truck revenue per load to decline in the high single-digit percentage range year-over-year, total revenue of $1.075 to $1.125 billion and EPS of $1.56 to $1.62.

In early June, the asset-light provider of transportation solutions warned that there was risk to the bottom-end of its guidance range at an investor conference. At the time, Landstar’s President and Chief Executive Officer Jim Gattoni said weak truckload spot market fundamentals resulted in a 1 percent year-over-year decline in volumes and a low double-digit decline in truck revenue per load through the first two months of the second quarter.

Takeaways from the call

On its earnings call, management said that it believes the third and fourth quarters of 2019 will look similar to the second quarter of 2019, with sluggishness in the manufacturing sectors continuing to weigh on freight demand. They noted that platform (flatbed) business is doing well, but that the relative outperformance compared to dry van demand is due to heavy haul, large project freight. They believe truck capacity will remain flat for the rest of the year because it’s not entering the market currently, but “it’s not getting any lower.” Further, they said “another catalyst,” like another decline in rates, may be needed to force excess capacity to leave.

Management said that they have seen more seasonality in pricing recently. Truck revenue per load is 1 to 2 percent higher in July compared to June, but is still down year-over-year in a similar range to that of June (down 13 percent). All in, management describes the current market as a “relatively healthy freight environment,” and noted that its financial results are still well ahead of 2017.

The potential negative margin impact from digital freight brokers was discussed on the call. Digital freight brokers provide an automated service in which loads are matched with truck capacity, significantly reducing overhead as human touch is minimized. This allows the digital brokers to capture market share by pricing freight at a modest discount to the market.

Management said that they are simply “playing a pricing game.” They expect pricing pressure over the next few years as digital freight brokers build scale, but noted that this has not had a negative impact on LSTR’s margins yet. Management believes that 70 percent of its business is “sticky” and that digital brokers struggle to compete with LSTR for platform, automotive, government, time-definite and cross-border freight. They believe that their relationships are strong with these customers and that the intricacies in the movement of some of this freight will always require human touch.

Management acknowledged that there is the potential for margins to be negatively impacted longer-term, but said that they would just have to push more volume through their system to offset margin erosion. Currently, they believe a significant amount of freight could be pushed through the LSTR network without adding to headcount.

Guidance

LSTR issued third quarter 2019 guidance that calls for a low single-digit decline in loads hauled via truck, a low double-digit decline in revenue per truck load, revenue of $1.01 to $1.06 billion and EPS of $1.48 to $1.54, lower than the current consensus estimate of $1.55.

Earnings results

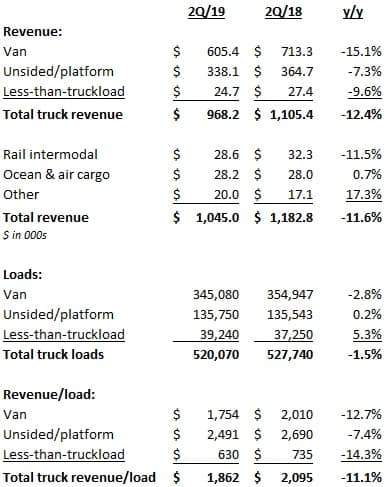

LSTR reported an 11.6 percent revenue decline year-over-year to $1.045 billion, with gross profit (revenue less the cost of purchased transportation and commissions to agents) down 7.8 percent to $158 million in the period.

“Landstar’s business model performed very well in the 2019 second quarter given the significant change in U.S. freight dynamics from 2018 to 2019. We entered 2019 knowing we would face very difficult year-over-year comparisons after a record-setting 2018. The freight environment softened further from the 2019 first quarter to the 2019 second quarter, putting additional downward pressure on rates, especially in the spot market where the company primarily operates,” said Gattoni.

The company’s truck revenue declined 12.4 percent year-over-year as total truck loads were down 1.5 percent and revenue per truck load declined 11.1 percent in the second quarter 2019. The revenue per load declines increased as the quarter progressed with declines of 8 percent in April, 11 percent in May and 13 percent in June.

Gattoni continued, “the pricing environment for our truck services continued to drive truckload rates in the 2019 second quarter below the 2018 second quarter, as industry-wide truck capacity was more readily available than during the 2018 second quarter.”

Dry van revenue was down 15.1 percent and platform revenue declined 7.3 percent. Dry van loads declined 2.8 percent with revenue per load declining 12.7 percent. Platform loads were basically flat year-over-year with revenue per load down 7.4 percent.

Lastly, loads via railroads, ocean cargo carriers and air cargo carriers were 8 percent lower year-over-year in the quarter.

Gross profit margin increased 60 basis points to 15.1 percent in the period and operating margin (LSTR calculates operating margin as operating income divided by gross profit) increased 250 basis points year-over-year to 51.2 percent. Lower insurance and claims expenses and lower selling, general and administrative (SG&A) expenses led to the increase. SG&A expenses declined as variable bonuses and stock compensation expense declined on lower earnings.

The company also announced that its Board has increased its regular quarterly dividend by 12 percent to $0.185 per share.