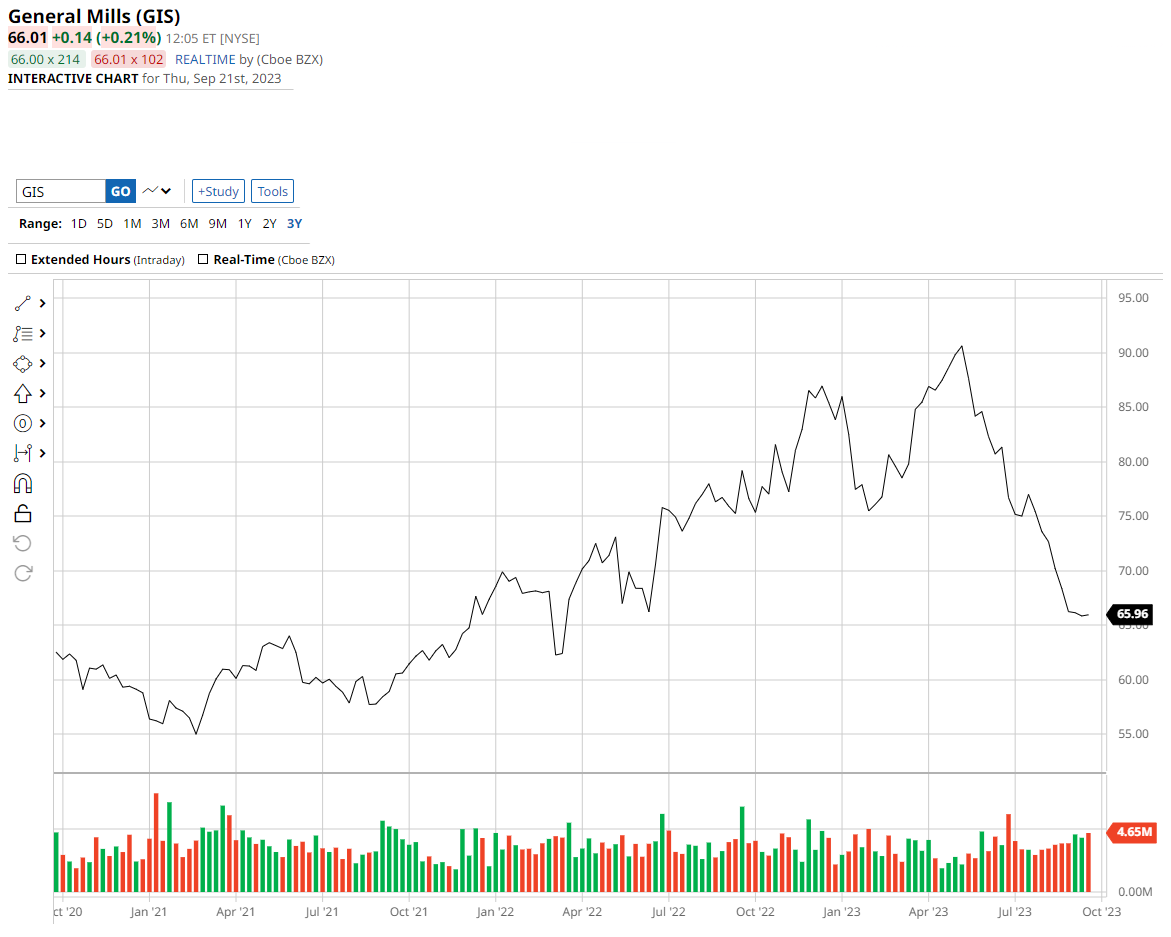

General Mills leverages newfound strategic revenue management capability to effectively balance pricing and volume

Chart: Barchart.com Inc.

General Mills on Wednesday reported its fiscal first-quarter results and the shares didn’t do much with little variance from expectations and management reiterating full-year guidance. But the company highlighted a number of CPG industry trends.

- Pricing strategies have become more sophisticated. According to management, a major difference between this year and last is that both retailers and CPGs have built more effective price elasticity models to predict changes in volume in response to changes in pricing (referred to as strategic revenue management or SRM). That pertains not just to listed prices but also promotions and end-of-aisle displays. The goal is to know how aggressively to push pricing, and on which products, to maximize margins while also maintaining or growing market share.

- Elasticities have risen from last year’s level. That suggests that consumers are under more pressure than they were and that is impacting CPG sales after a period in which CPG sales seemed to defy gravity. However, CPG elasticities remain manageable — in its fiscal Q1, General Mills’ volume declined 2% year over year (y/y) on a 7% increase in price and mix.

- Maybe pet food isn’t as bulletproof. While pet food and fresh/organic pet food have been growth areas, and while many pet parents feed their animals better food than they feed themselves, General Mills saw consumers trade down in wet food and treats in its fiscal first quarter and expects those trends to persist throughout its fiscal year. Sales of Blue Buffalo pet treats, a discretionary category, declined double digits.

- Disinflation is here but input costs are still rising. Input cost inflation is expected to be 5% in General Mills’ fiscal 2024, driven largely by labor inflation that impacts ingredient sourcing and manufacturing costs. In general, the costs to produce processed food is still rising even if the prices of some commodities that serve as ingredients have come down.

- Gross margins are recovering gradually. General Mills’ adjusted gross margin increased 50 basis points to 35.4% in its fiscal Q1. During periods of disinflation, most CPGs should be able to regain margin points that were lost during the past two years as price increases catch up to recent cost increases. Still, the decline in General Mills’ adjusted operating margin — which declined 60 basis points y/y — reflects ongoing increases in selling, general and administrative expenses.

- Pandemic-era supply chain issues are in the rearview mirror. Customer service levels were back to the mid-90s for General Mills’ just-reported fiscal Q1 versus the mid-80s and high 80s in the company’s fiscal ’22 and ’23, respectively. In other words, there are fewer stockouts to discuss in The Stockout.

- Advertising spending is returning. Many CPGs had cut back on marketing when supply chain issues were impairing service levels. Now, strong service levels are encouraging more advertising spending and General Mills expects to keep advertising growth rates at least in line with sales growth rates going forward. As advertising returns, look for this area to get more sophisticated as well — e-commerce and web tracking are enabling targeted advertising and promotions, opening up a new, high-margin revenue stream for retailers.

- CPGs are looking to grow through acquisition. CPGs that have developed innovative brands or that are in fast-growing areas are the most attractive acquisition targets.

Rail intermodal contract rates under pressure

(Chart: SONAR – IMCRPM1.USA Seasonality)

Despite the recent comment from J.B. Hunt, the largest truckload-based domestic intermodal provider, that we are coming out of the freight recession, domestic rail intermodal is one segment where rates are still falling. The SONAR chart above shows that intermodal rates (not including fuel surcharges) rose double-digit percentages first from 2020 to 2021 and again from 2021 to 2022. This year, rates have fallen throughout the year by double-digit percentages and have stairstepped down from the first quarter as more contracts have come up for renewal.

This week, we heard an anecdote from a major CPG company that intermodal volume it recently put out to bid resulted in rates that declined double-digit percentages. Asset-based intermodal carriers appear to be chasing volume more aggressively than non-asset-based carriers. That difference likely reflects the heavy investment that the asset-based intermodal carriers made in containers, which, so far, has exceeded demand.

GXO Direct leverages its tech and scale to deliver flexible warehousing solutions

(Image: FWTV)

Grace Sharkey and I interviewed Steve Lewis, division president at GXO Direct, on Monday. GXO’s warehousing and fulfillment solutions for shippers range from handling a specific node to handling the client’s entire supply chain. Clients include many small and midsize shippers that are looking to expand sales quickly (often from direct to consumer only to also selling through retailers) while also serving large enterprise shippers.

Fulfillment has grown in complexity with the expansion in e-commerce and the demand for omnichannel fulfillment. GXO offers warehousing space on a flexible basis so shippers only purchase what they need; its scale and location density within key freight markets, such as having six facilities in the LA area, are key enablers of that flexibility.

See the full interview here.

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.