A strong economy, little available capacity, and a lack of drivers combined with the requirement of electronic logging devices (ELDs) have contributed to skyrocketing shipping rates. Spot rates are hovering near record highs and contract rates saw steady increases late last year during bid season, even double digit increases according to some carriers.

For fleets that spend time operating on load boards, it’s been a good time to be in business. For shippers, though, it’s been a challenging time as they have been forced to adjust to a new era in trucking.

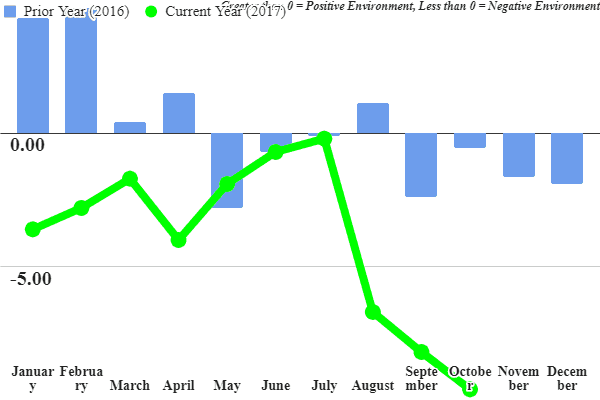

According to FTR, its latest Shippers Conditions Index (SCI), released in late December, showed an October reading of -9.6. What does that mean? According to the firm, any reading below zero represents pessimistic conditions for shippers. At -9.6, it is suggesting a significant problem for shippers, bordering on operating change levels.

“Conditions for trucking and shipping have been diverging dramatically since the hurricanes hit in August. The hurricanes highlighted the lack of extra capacity available in the system. This has been followed by continued strong freight conditions in Q3 and into Q4,” explains Eric Starks, chairman & CEO. “Shippers are really feeling the pinch right now, and there is fear that the ELD mandate will impact capacity in the spring. We have essentially hit the 100% capacity mark. There is little, if any excess truck capacity. Add in regulations, continued freight growth or winter storms, and we could be pushing that above 100%. That would leave shippers scrambling to get loads delivered. And that means paying premium rates for those deliveries. It may be a tough first half of 2018 for shippers.”

FTR said that the tight capacity could ease somewhat in the first quarter of this year, but “there is additional downside risk to the SCI for early 2018 if contract rates jump substantially or the electronic logging device (ELD) effects are more pronounced than expected.”

A Morgan Stanley survey of carriers, brokers and shippers in the fourth quarter found that shippers believe brokers and carriers are trying to take advantage of the current market. While prices are up, some believe there is plenty of capacity available and that rates shouldn’t continue rising.

“Pockets are starting to soften. I would expect the market to take a winter lull before ramping up to current levels in spring. The one thing that could throw off the market again would be another natural disaster,” said one shipper.

Another believes brokers are trying to take advantage of the market. “Seeing capacity tightness only in certain markets. Brokers seem to be trying to milk more margin out of every load by taking advantage of an unstable market,” the shipper complained.

One thing seems to be real, if evidence of fleet trailer orders is any indication, there is a capacity crunch happening. Orders for December reached a record of 47,000 units, up some 10% over November and 38% year-over-year. Total trailer orders for 2017 were 308,000 units, FTR said, which attributed the rise to the strong economy and tight capacity driven in part by the electronic logging device mandate. The group noted that carriers may be switching to more drop-and-hook operations where possible to maximize driver productivity, necessitating the need for more trailers.

“December was just an awesome month for trailer orders. We have seen pressure build on equipment markets for several months, and this shows Q1 is going to be hectic as fleets scramble to keep up with freight demand,” said Don Ake, vice president of commercial vehicles.

Tractor order numbers were also high in 2017, suggesting fleets are looking for the good times to continue.

Capacity crunch or not, for shippers with product to move, they need space. C.H. Robinson recently produced a whitepaper with suggestions on how to obtain that needed capacity in a tight capacity market.

Among the Robinson tips, be flexible on pickup dates and hours, understand current market conditions, maintain a stable set of service providers and don’t try to time the market. Shippers who have trouble securing capacity are often looking for below-market rates, provide short lead times or have a reputation for lengthy loading times, something that many fleets are more conscious of in an ELD rule.

“When a preferred carrier rejects a load, forcing the shipper to delve into their routing guide, transportation spend tends to rise and budget overrun occurs,” the company wrote. “Typically, as a shipper delves deeper into their routing guide, they experience a higher rate per mile. Overall, with each step down the routing guide, shippers pay about $26.00 more per shipment in rates. Research proves that longer lead times can improve carrier acceptance rates.”

With ELDs now strictly monitoring driving hours, fleets have little room for delay. Shippers who provide flexible pickup options can benefit from better rates and consistent service. And finally, “timing the market” can backfire, Robinson said.

“Shippers who try to lock in rates when they believe rates are absolutely at their lowest point often experience other challenges. For instance, research shows that if pricing is below market, on time delivery suffers,” it wrote.

The time may not be right for shippers, but trucking is a cyclical business. Currently, carriers have the leverage, but that can quickly turn, and may if the economy slips at all and current equipment buying cycles prove too ambitious.

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.