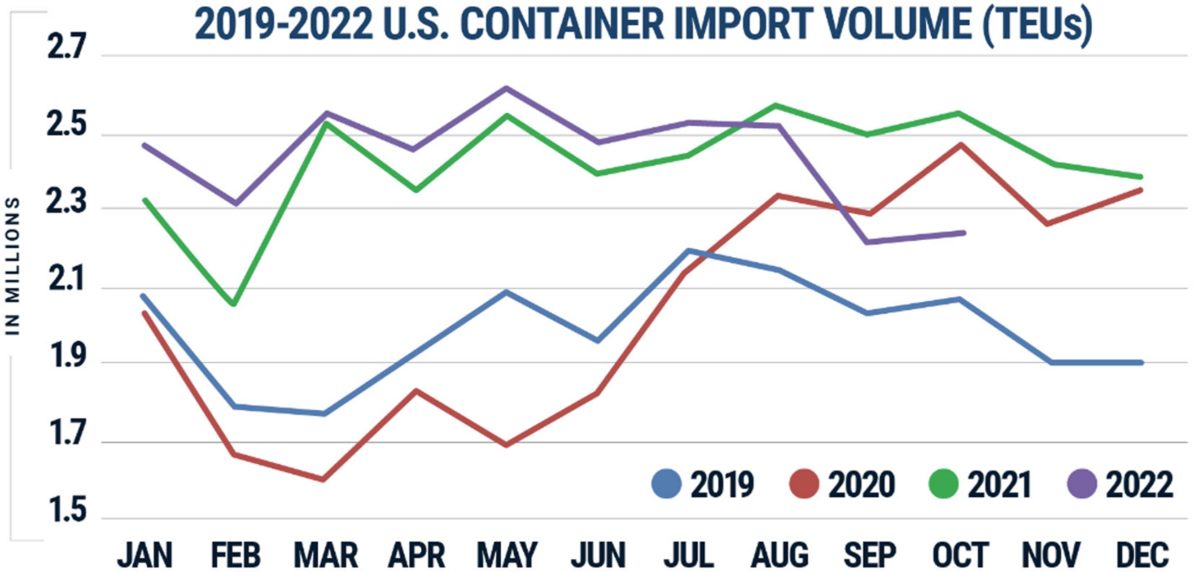

The outlook for U.S. imports looked ominous in September, when volumes plummeted double digits, both year on year and compared to August. If imports had continued to collapse at September’s pace, they would have sunk below pre-COVID levels in October.

But imports didn’t continue to plunge in October, according to data released Monday by Descartes Datamyne. Last month’s volumes were effectively flat versus September. The reversion toward pre-pandemic volumes is taking a more gradual path.

According to Descartes, U.S. ports handled 2,220,331 twenty-foot equivalent units of imports in October, effectively unchanged (up 0.2%) versus the month before. Volume was down 13% year on year yet still up 7.2% versus October 2019, pre-COVID.

Savannah rebounds, NY/NJ pulls back

September’s plunge was driven by exceptionally large declines at the ports of Los Angeles and Long Beach, California, and Savannah, Georgia. In October, Descartes reported much smaller month-on-month drops at the two California ports: 9,241 TEUs in Long Beach (down 2.7% versus September) and 12,105 TEUs in Long Beach (down 3.9%).

Savannah was a special case. September volumes were pushed down over 20% by the Hurricane Ian closure. The latest Descartes numbers show an increase of 11,958 TEUs or 5.3% for Savannah in October versus September. (Descartes derives its data from customs filings; its numbers differ from official port numbers that are released later each month.)

In addition to Savannah, month-on-month gains were recorded for Houston; Charleston, South Carolina; Oakland, California; and Seattle and Tacoma, Washington.

The biggest surprise in the numbers was a large drop for New York/New Jersey, which recently surpassed Los Angeles to become America’s busiest container port. According to Descartes, New York/New Jersey imports fell 26,972 TEUs or 6.3% in October versus September.

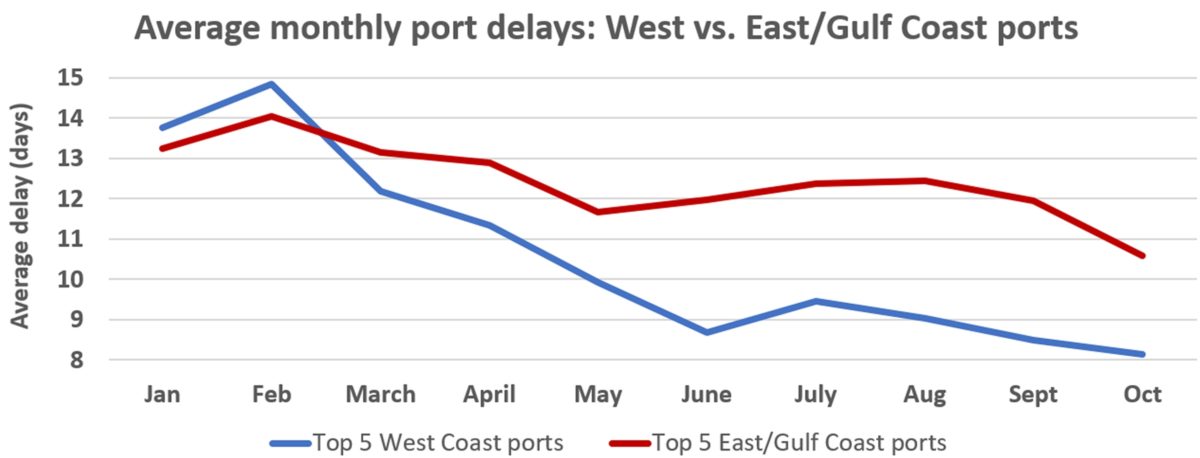

East Coast delays still high but easing

Shippers have shifted significant volumes from West Coast ports to East and Gulf Coast ports due to concerns over West Coast port labor negotiations. A new labor contract has still yet to be negotiated, more than four months after the last one expired.

This shift led to a drop in vessels at anchorage or loitering offshore of West Coast ports and a rise of ships waiting off the other coasts.

According to American Shipper surveys of MarineTraffic ship-position data and port queue lists, the total number of ships waiting off North American ports rose to around 150 in January and then fell below 100 in the spring as the Los Angeles/Long Beach queue cleared. It then rebounded back over 150 in late July, driven by queues off the East and Gulf coasts.

Since then, as inbound volumes have declined, queues have gradually cleared. The tally fell below 100 by mid-October. As of Tuesday morning, there were 87 ships waiting, 14% off the West Coast and 86% off the East and Gulf coasts. That’s still very high: Pre-COVID, the number was in the single digits.

Descartes data on average port delays shows the same divergence between the coasts.

This data shows that the average delays at the top five West Coast ports fell 40% from January through October. In contrast, average delays in the top ports on the other two coasts fell at half that pace — by 20% — over the same period.

Click for more articles by Greg Miller

Related articles:

- US imports sink in September, suffer steepest drop since 2020 lockdowns

- Container-ship logjams off US ports finally easing as imports fall

- Shipping rates are no longer plunging. Is ‘new normal’ near?

- Did US slash imports too much, setting stage for shipping rebound?

- Container imports to Los Angeles and Long Beach are plummeting

- Global trade at the crossroads: Risks from geopolitics, inflation loom