Updated at 3:15 p.m. EST. Earnings call adds.

Cargo business fell during a challenging third quarter for American Airlines [NASDAQ: AAL], which faced operational disruptions and higher costs from labor issues, weather and the grounding of the Boeing 737 MAX.

As previewed, the Dallas-based carrier reported Thursday that cargo revenue fell 20% to $208 million in the quarter ended Sept. 30, versus the same year-ago period, primarily due to a 16.5% decrease in cargo ton miles (621 million). Cargo revenue was down 13.5% to $647 million for the first three quarters as cargo ton miles, an industry metric measuring the distance cargo is hauled, came in 14% lower.

By comparison, United Airlines [NASDAQ: UAL] saw third-quarter cargo revenue decrease of 4.7% to $282 million, while Delta Air Lines [NYSE: DAL] experienced a 17% drop to $189 million, part of a year-long downward trend for the airfreight sector overall due to international trade tensions and softer economic growth in key markets.

American’s cargo yield per ton mile — the average rate paid per mile — was 4% lower to 33.57 cents per mile and is nearly flat through three quarters at 34.24 cents per mile.

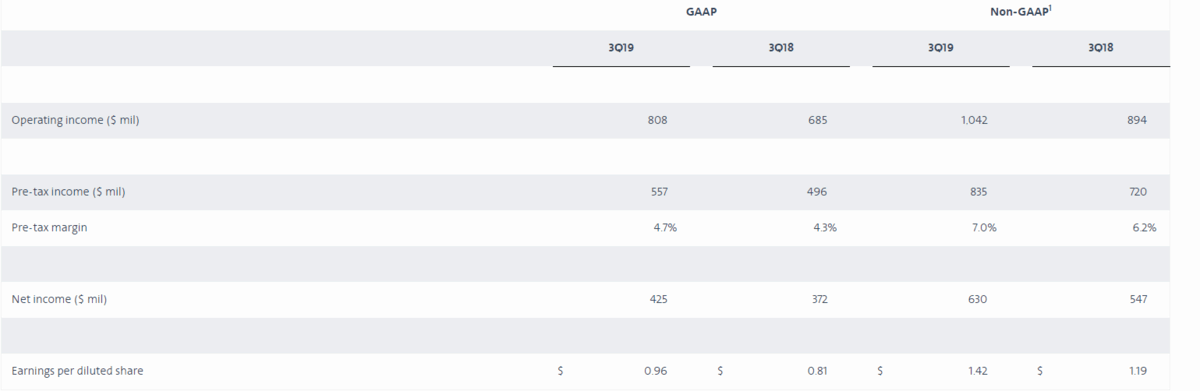

Third-quarter net income, excluding special items, grew 14.5% to $425 million, but earnings per share came in at $1.42, in line with analysts’ expectations of $1.40 per share. Operating income rose 18% to $808 million on record revenue of $11.9 billion. American achieved its 12th consecutive quarter of total-revenue-per-available-seat-mile growth, coming in 2% higher at 15.71 cents.

Company officials acknowledged the performance was disappointing and expressed confidence that corrective steps will have a positive impact in 2020. They have accused labor unions representing mechanics of an intentional work slowdown in the midst of difficult talks on a new contract, but said that since talks resumed in September following court intervention reliability has noticeably improved.

American slightly lowered its full-year earnings forecast by 50 cents at the top end to a range of $4.50 and $5.50 per share.

President Robert Isom told analysts on a conference call that American has already seen significant improvement in operational reliability since June, with on-time arrival in September representing the seventh best month in the airline’s history. The retirement of older aircraft, simplified scheduling and more resources for airport and maintenance operations is helping performance.

According to U.S. Department of Transportation for July, American was in the middle of the pack with a 75% on-time arrival rate that included flights operated by code-share partners. And it lead the domestic industry with a 3.5% cancellation rate.

“Our underlying execution is solid and we are committed to returning American to a position of operational excellence,” he said. “As a result, we expect our 2020 completion factor to increase by 1 to 2% and achieve a significant improvement in all reliability metrics, including on-time performance, baggage handling and customer satisfaction. We know we can’t allow our customers and our team members to experience another period like this past summer ever again.

“So, if for some unforeseen event, in 2020 lead us to question our ability to meet our reliability standards we will reduce our schedule, rather than let our operations become unreliable. It’s a commitment we need to make to ensure we restore operational excellence,” Isom pledged.

American repeated earlier statements that the cancellations of 737 MAX flights in the third quarter impacted pre-tax income by $140 million. American has 24 MAX aircraft in its fleet, with an additional 76 aircraft on order, of which five were scheduled to be delivered in the third quarter. The company has removed the MAX from its flight schedule through Jan. 15 and on Thursday said it now expects the cancellations to negatively impact its full-year pre-tax income by about $540 million.

American said total third-quarter operating expenses were $11.1 billion, up 2% year-over-year. Total operating cost per available seat mile (CASM) was up 1% to 14.64 cents. Excluding fuel and net special items, CASM was 11.07 cents, up 5%, due primarily to higher salaries and benefits, maintenance and regional expense, and lower-than-planned capacity.

Chairman and CEO Doug Parker said American will grow its network by about 5% next year, mostly at airports that can command higher pricing than the company’s overall system. Officials said results of the network expansion at American’s main hub, Dallas-Fort Worth, surpassed initial expectations. The company added 100 daily departures, equivalent to 9% extra capacity, resulting in a 3.5% increase in passenger revenue per available seat mile compared to 2018. It said the growth sets a positive precedent for planned expansions next year at Charlotte Douglas International Airport and Ronald Reagan Washington National Airport in 2021.

Isom downplayed the potential loss of market share as a result of LATAM Airlines leaving its loose partnership with American for a joint venture with Delta Air Lines, saying American’s extensive network in South America “will ensure we recapture the majority of the code-share revenue on our own aircraft. And that’s already proving to be the case. There has been no revenue impact since the announcement. American remains the largest U.S. carrier to Latin and S. America and we are committed to providing the best service to the region for our customers.”

American also recently announced additional frequencies between its Miami hub and Lima, Peru; Sao Paulo, Brazil; and Santiago, Chile.

Delta officials have said they won’t begin code-sharing with LATAM until December, at the earliest.