Hutchison Port Holdings Trust (SGX: NS8U), a Singapore Stock Exchange-listed container terminal operator active in Hong Kong and mainland China, has reported a small decline in unaudited revenues for the nine months to September. That led to a 5% fall in profit after tax.

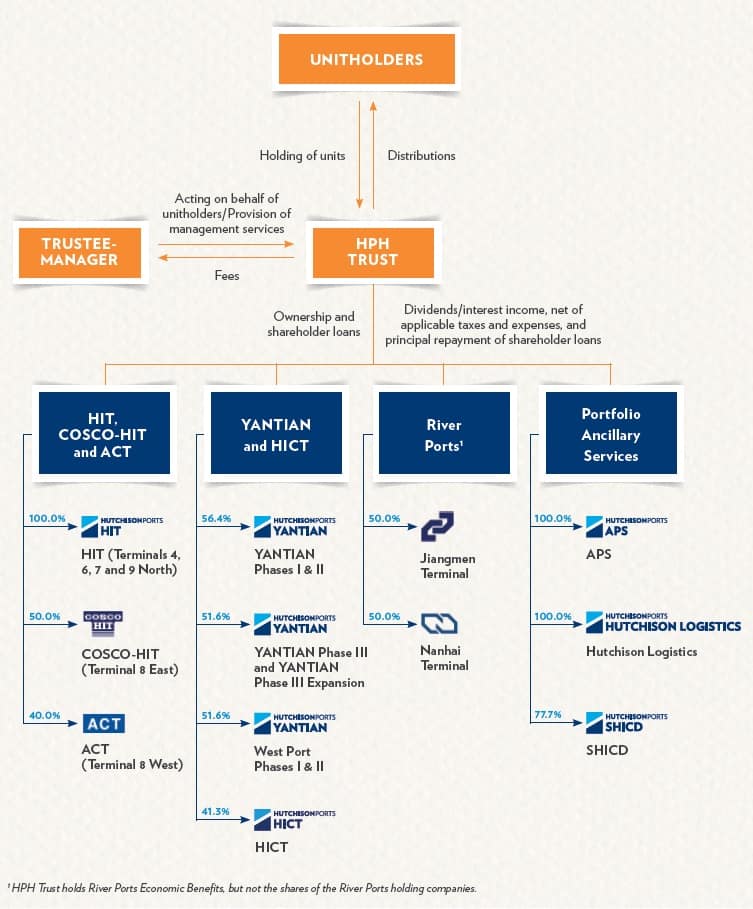

HPH is an equity holder in several container terminals in Hong Kong and mainland China. These are the Hong Kong International Terminals, the Cosco-HIT Terminals and the Asia Container Terminals, all of which are in Hong Kong. In mainland China, it is the majority equity holder in the Yantian International Container Terminals and the Huizhou International Container Terminals. It also owns equity in a couple of Chinese river ports and it owns several ancillary ports businesses (see graphic).

Nine months to September 2019

Revenues declined from just over Hong Kong $8.48 billion to HK$8.45 billion (US$1.103 to US$1.099 billion), which is a 0.36% fall, at the end of the nine months to September 2018 to the end of the nine months to September 2019. At the time of writing, one Hong Kong dollar is worth 13 cents U.S.

Operating expenses incurred by HPH were largely flat, declining by about 1% from the HK$5.83 billion recorded at the end of the nine months to September 2018 to HK$5.77 billion in the same period this year.

Operating profit increased marginally, up by 1% to stand at HK$2.68 billion in the current period, but there were other finance-related costs that dragged profit before tax down by 1% to stand at HK$1.83 billion. Profit after tax declined by 5% to HK$1.46 billion.

Three months to September 2019

On a third-quarter (July to September) basis, HPH generated a small increase in revenues. It generated a 0.08% rise from HK$3.027 billion to HK$3.029 billion (US$393 million to US$394 million). Most of the individual lines in HPH’s operating expenses accounts were marginally down, leading to a 1% fall in total operating expenses to HK$1.96 billion. Third-quarter profit before tax was HK$795.1 million (US$103 million), which is a 3% increase on the corresponding period last year. Profit after tax was flat at HK$640 million in both the 2019 and 2018 third quarters.

Current assets, liabilities and ratio

As of Sept. 30, HPH had HK$9.48 billion in current assets, which is about two-thirds comprised of cash. The other third is trade and other receivables. Its current liabilities were just under HK$10.20 billion and were mostly comprised of trade and other payables (about 56%) along with bank and other debts (about 40%). Current tax bills make up the rest of the current liabilities.

As of Sept. 30 last year, HPH had just over HK$8.31 billion of current assets, of which about two-thirds was comprised of cash and the other third was comprised of trade and other receivables. Current liabilities were just under HK$9.44 billion.

Although HPH’s current assets are increasing, so are its current liabilities. As of Sept. 30, HPH’s current ratio (which is an indication of the company’s ability to pay short-term bills) was 0.92. As of Sept. 30, 2018, that current ratio was 0.88.

A current ratio rising toward the number 1 indicates that the company is becoming more capable than it was of meeting its short-term obligations.

Container throughput

HPH also detailed its container throughput for the period of nine months ending Sept. 30. In that time HPH handled over 17.4 million twenty-foot equivalent unit (TEU) shipping containers. By way of comparison, for the full years of 2018 and 2017, it handled 24.02 million and 24.28 million TEUs, respectively.

HPH noted that despite an 8% decline in outbound cargo to the U.S. in the third quarter of 2019, outbound cargo to the European Union grew by 6% when compared to the previous year.

“Outbound cargoes to the U.S. remained weak and slipped in the third quarter of 2019 amid [the] trade dispute between the U.S. and China. Whilst the bilateral trade talk between the U.S. and China resumed, it is not expected the trade dispute can be fully resolved shortly and will continue to weigh on HPH Trust’s performance. Given the uncertainties in the global trade outlook, HPH Trust management remains cautious about future cargo trends,” the trust said in a statement.

It added that global trade “remains sluggish” because of intensifying trade tensions along with slowing manufacturing and business activity. HPH Trust also pointed to “elevated” geopolitical and economic risks, including Brexit and Middle East tensions, as having the potential to “stymie the global economic growth.”

Looking forward, the trust stated that it anticipates ocean container shipping companies will likely “continue to drive cost efficiencies and promote fleet and capacity optimization” because of the effects of uncertainty in global trade and an increase in op-ex from the low-sulfur fuel regulation, IMO 2020.