Are sellers on Amazon Marketplace victims of an Amazon monopoly?

Amazon shares (black) versus the S&P 500 (blue). Amazon has a 3.1% weighting in the index. (Chart: Barchart.com Inc.)

The 172-page lawsuit filed by the Federal Trade Commission (FTC) and 17 state attorneys general last week brought to the forefront the challenges that CPG companies and other sellers face on Amazon Marketplace. Whether Amazon is abusing a monopoly or not, it’s clear that sellers face an uphill battle when attempting to sell on Amazon Marketplace profitably.

All sellers have to do is make sure that their prices on Amazon are consistent with those on other online superstores so their results don’t get buried in search results and get the “buy box” taken away. And, if there are competitors selling the same thing, be sure to win the “buy box” by purchasing enough advertising. And, don’t forget that Amazon Prime customers, who buy four times as much as non-Prime customers, are much more likely to buy an item that is an Amazon Prime product, so you better qualify. And to qualify, sellers must use Amazon’s fulfillment services, which includes paying the e-commerce giant for warehousing, pick-and-pack, and delivery. The FTC alleges that total Amazon fees can represent 50% of sellers’ gross sales.

How then, are Amazon Marketplace sellers able to turn a profit given the Amazon fees and the inability to charge higher prices on Amazon to pass along those costs? In many cases, they aren’t. Often, sellers remain on Amazon to take control of the narrative against competitors’ claims, to help consumers find information and to prevent third parties from selling their products on Amazon once they find a supply. The fact that many sellers remain on Amazon Marketplace while realizing little or no profit is something the FTC takes as support of Amazon’s monopoly status.

I recommend that consumer packaged goods companies read this white paper from Cartograph, a company that assists sellers with their Amazon strategies: “How and when emerging CPG brands should launch on Amazon.”

Highlights include:

- In the U.S., CPG companies generally need gross margins at a minimum of 70% to make the Amazon channel profitable.

- As a result of the high margins needed, CPG categories where inclusions make sense on Amazon include organic food items or those focused on specific diets (e.g., Keto).

- CPG brands see the greatest velocities in the $10-$15 range, and Amazon gives a fee break for grocery products under $15.

- Pack sizes need to be increased from those designed for grocery stores that are priced at $3-$5 — items in that range are rarely profitable in e-commerce when other costs are included.

- Consumers see value in Prime delivery and are willing to accept 10%-20% higher per-unit product costs on the channel.

Prime consumers value speed and convenience over price

The last bullet in the section above regarding Prime is an important one. The FTC alleges that it’s not just sellers on Amazon Marketplace who are hurt by the company abusing its monopoly position, but also the consuming public. According to the suit, sellers increase their prices on other sites (or even ask the other sites to take their products down) in order to maintain price parity with Amazon and comply with its “favored nation policy.” According to the FTC, that practice has boosted Amazon’s sales at the expense of consumers — whether they shop on Amazon or on competing sites.

Why then, do consumers remain so enamored with Amazon, and will that change with these issues being brought to light? Well over 100 million Americans willingly subscribe to Amazon Prime, which has about a 91% satisfaction rate and a very low cancellation rate. Maybe the consuming public is not sophisticated enough to know they’re being abused by a company with a dominant market position. Or, maybe consumers are just less concerned with price and have been conditioned to expect deliveries quickly and to the perception (incorrect, I argue) that they are not paying for shipping.

For more on the FTC Amazon complaint, check out last week’s The Stockout newsletter.

Intermodal volume up as shippers see improved service and changing market conditions

Here are three SONAR charts I highlighted on this week’s People Speaking Rail show.

Loaded containerized domestic intermodal volume has risen seasonally the past few weeks. It won’t be a seasonal peak like we saw in 2020, but on that measure of domestic intermodal volume the past two weeks is 4.7% above where it was in mid-August and up 6.3% y/y. That’s better than the 3% y/y increase in the Association of American Railroads data, which also includes international units and revenue empties. I have heard from shippers that the improved level of rail service is the primary purpose for shifting from truckload to intermodal this year.

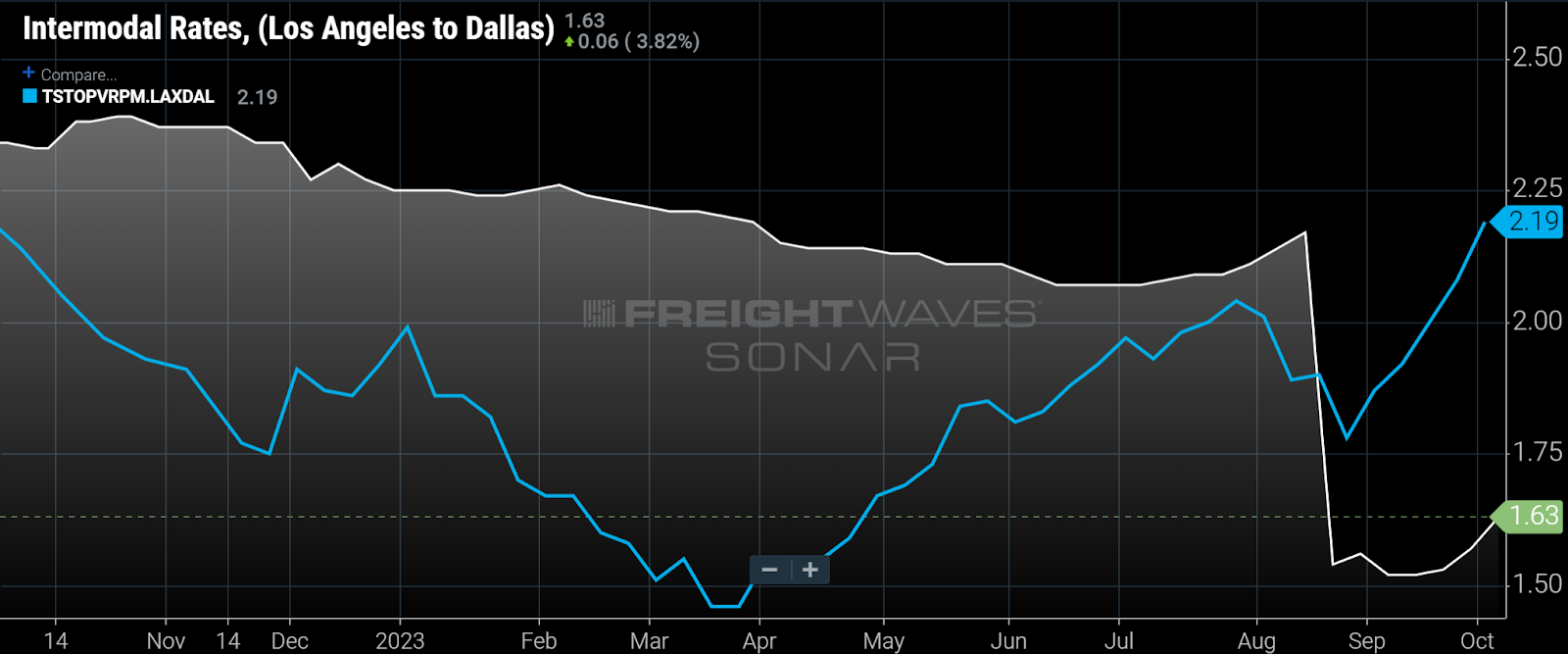

Meanwhile, intermodal contract rates are down double digits compared to the year-ago period — the chart above shows average domestic intermodal rates excluding fuel surcharges. Relative to truckload, intermodal contract rates respond more slowly to market conditions (e.g., fewer quarterly contracts), and capacity excesses remain in the domestic intermodal segment especially with carriers having taken delivery of containers in recent months without a fully commensurate increase in volume.

In some lanes and markets, the domestic truckload and domestic intermodal markets have been going in divergent directions, with some evidence of tightening (or at least evidence of markets becoming less loose) in truckload in certain locations without the same dynamic in intermodal. The chart above compares the door-to-door intermodal spot rates (white) with the truckload spot rates (blue) in the LA-Dallas lane.

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.