This week’s FreightWaves Pricing Power Index: 75 (Carriers)

Last week’s FreightWaves Pricing Power Index: 75 (Carriers)

Three-month FreightWaves Pricing Power Index Outlook: 65 (Carriers)

The FreightWaves Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

The Pricing Power Index is based on the following indicators:

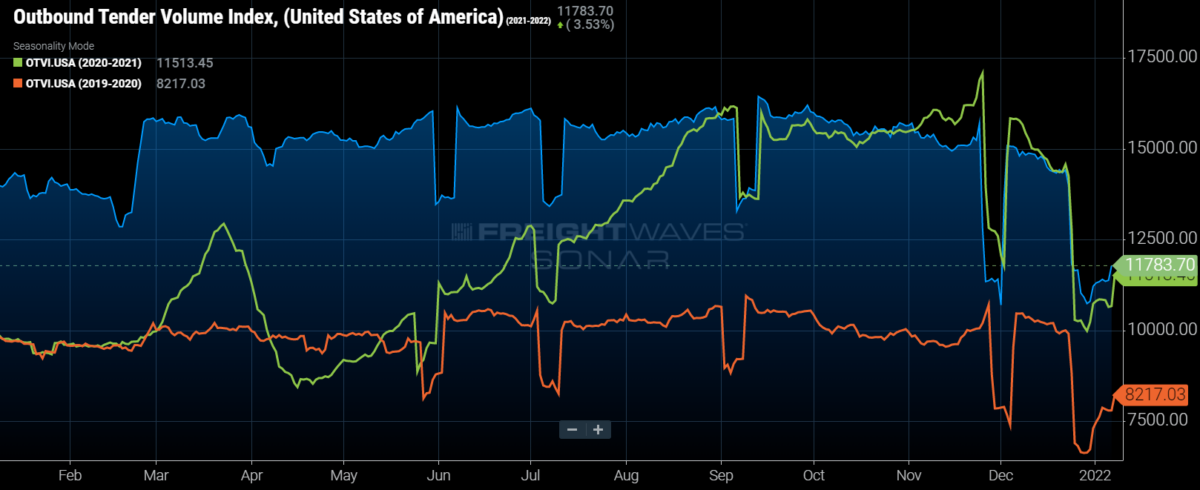

Volume levels starting to erase the holiday-affected noise

Traditional patterns are taking hold of the Outbound Tender Volume Index (OTVI). The holiday noise created by both Christmas and New Year’s is starting to erase itself in a similar fashion to the previous two years, just at elevated levels.

SONAR: OTVI.USA: 2021 (blue), 2020 (green) and 2019 (orange)

To learn more about FreightWaves SONAR, click here.

Tender volumes are outperforming 2021 levels by 2.35% year-over-year (y/y), which is a vast improvement from the previous two months, when tender volumes underperformed on a y/y basis. Compared to 2020 levels, tender volumes continue to run up by over 40%.

Over the next couple of days, the holiday noise will be completely erased from OTVI, as the seven-day moving average clears the holidays. However, this process is already to shine through as OTVI is up over 9% week-over-week (w/w). The comps for the next week will be elevated but should normalize at the beginning of the week of Jan. 17.

Accepted tender volumes, OTVI adjusted by the Outbound Tender Reject Index (OTRI), continue to hold their own. Accepted tender volumes are currently running up 12.2% over 2021 levels, the widest non-holiday gap since August. Accepted volumes are running up 8.6% w/w, as rejection rates have stayed elevated into the new year.

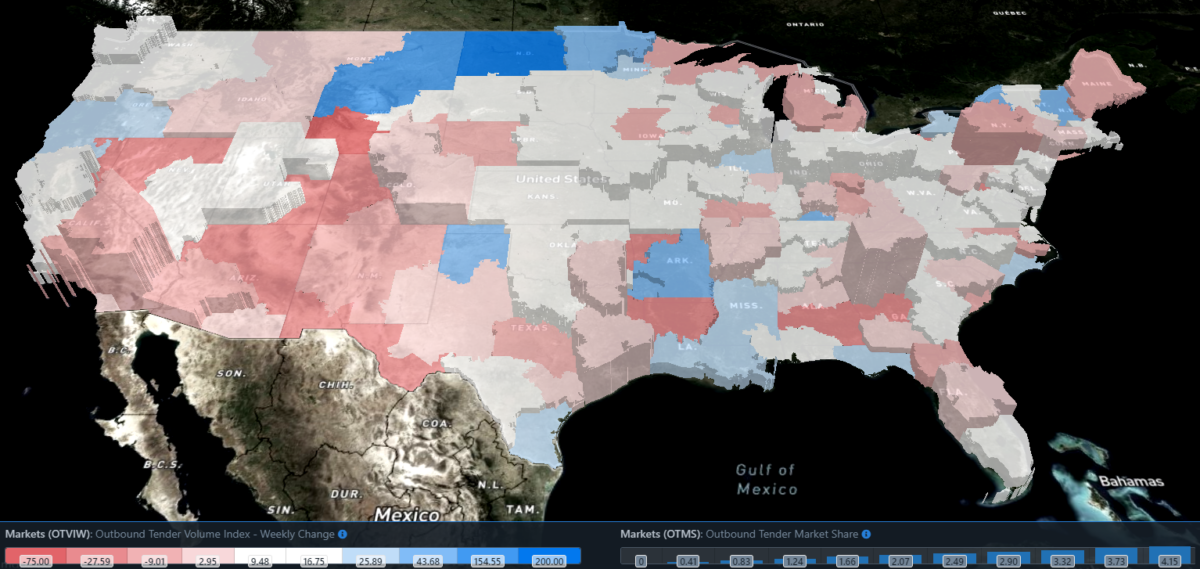

SONAR: OTVIW (color) and Outbound Tender Market Share (height).

To learn more about FreightWaves SONAR, click here.

Since OTVI is being affected by holiday noise, over the course of two weeks, looking at OTVIW this week is applicable, whereas next week the comps will be nearly irrelevant. Of the 135 freight markets, 102 experienced upticks in tender volumes over the past week, including the largest two markets in the country.

Ontario, California, the largest market in the country by outbound volume, experienced tender volumes increase by 1.29% w/w. Ontario’s neighboring market, Los Angeles, did experience a slight dip in tender volumes, falling 3.22% w/w.

Atlanta, the second-largest market in the country, experienced tender volumes increase by 3.22% w/w.

Expect that tender volumes across the vast majority of the country are well higher w/w, as the New Year’s holiday is removed from the index.

By mode: The Reefer Outbound Tender Volume Index (ROTVI) took a 10% w/w jump and continues to climb despite the holiday noise. For the first time since September, reefer tender volumes turned positive on a y/y basis during the holiday-affected weeks. The outlook for reefer volumes continues to be relatively strong, especially as the winter months are in full swing.

The Van Outbound Tender Volume Index (VOTVI) experienced a more moderate increase, rising 7.72% w/w. Van volumes have actually declined on a y/y basis, now down 1.78% y/y but are still holding up better than at any point during the past two months. With ocean bookings remaining near peak-season levels, demand for dry vans will be strong at least during the first quarter, even if VOTVI is negative y/y, due to the difficult comps of 2021.

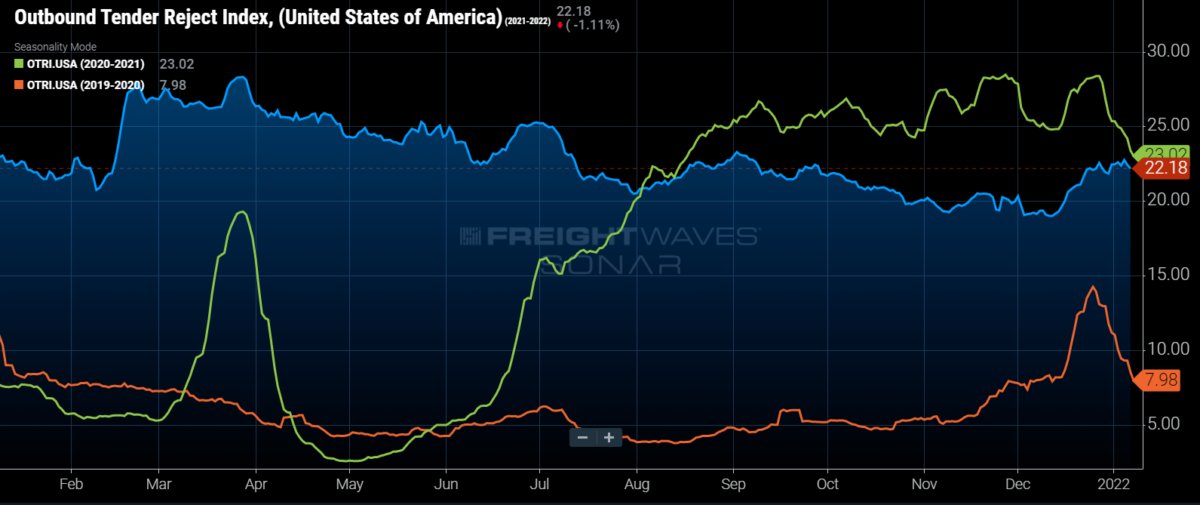

Rejection rates trending sideways despite the holiday season being over

Carriers are enjoying a vacation period after generating record revenues throughout 2021.

SONAR: OTRI.USA: 2021 (blue), 2020 (green) and 2019 (orange)

To learn more about FreightWaves SONAR, click here.

Unlike the previous two years, drivers haven’t returned to the road following Christmas. In both 2020 and 2019, rejection rates rapidly declined immediately following the holiday. In 2021, rejection rates have stayed relatively stable, increasing 32 basis points (bps) over the past week.

The gap with year-ago levels is now the narrowest that it has been since August. OTRI is just 84 bps below year-ago levels and may inflect positive in the coming days as rejection rates have been propped up during the past two weeks.

Why are rejection rates staying elevated for longer than the two previous years?

Carriers likely set record revenue numbers in 2021, due to rising rates throughout most of the year (both contract and spot). Add in unabating freight demand. When carriers do return, they will be keeping upward pressure on rates throughout the first part of the year. So while record rejection rates were unlikely during peak season, the period of elevated rejection rates extending into 2022 was very likely to happen.

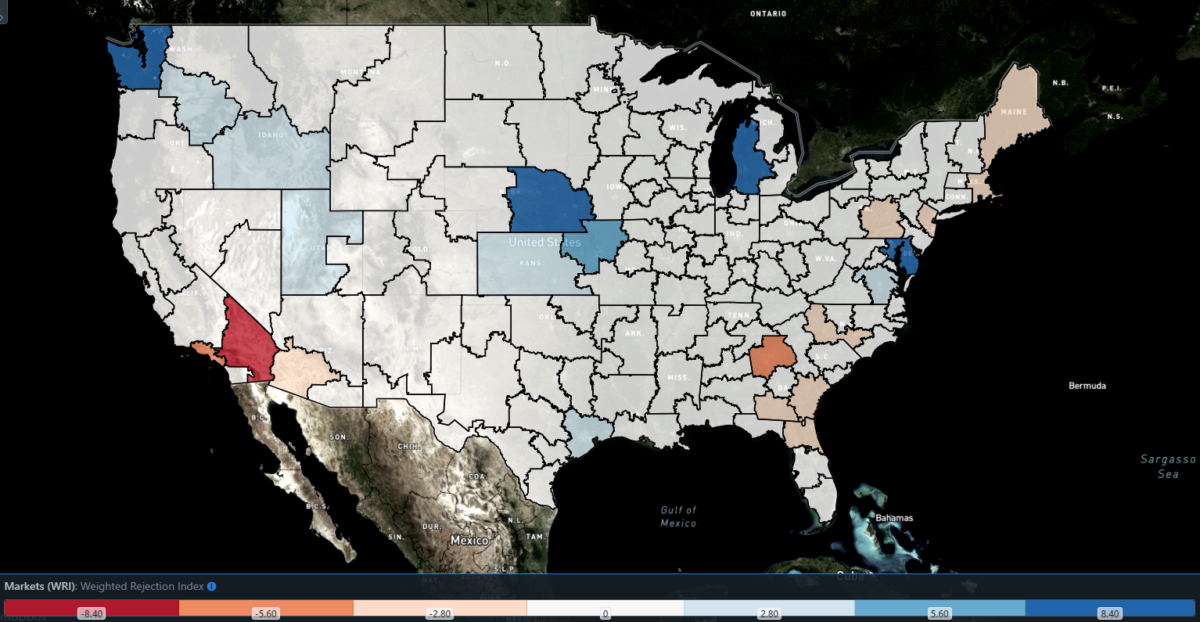

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

Of the 135 markets, 69 experienced rejection rates move higher this week.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. With capacity tightening around the country, there are a lot of blue markets, which are the markets to focus attention on.

It’s no surprise that following a holiday that pulls capacity off the road, the Ontario market is loosening faster than others as carriers are returning to the market. Rejection rates in the Ontario market have fallen by 238 bps over the past week. OTRI in the market currently sits at 15.53%, 176 bps below the year-ago level.

To learn more about FreightWaves SONAR,click here.

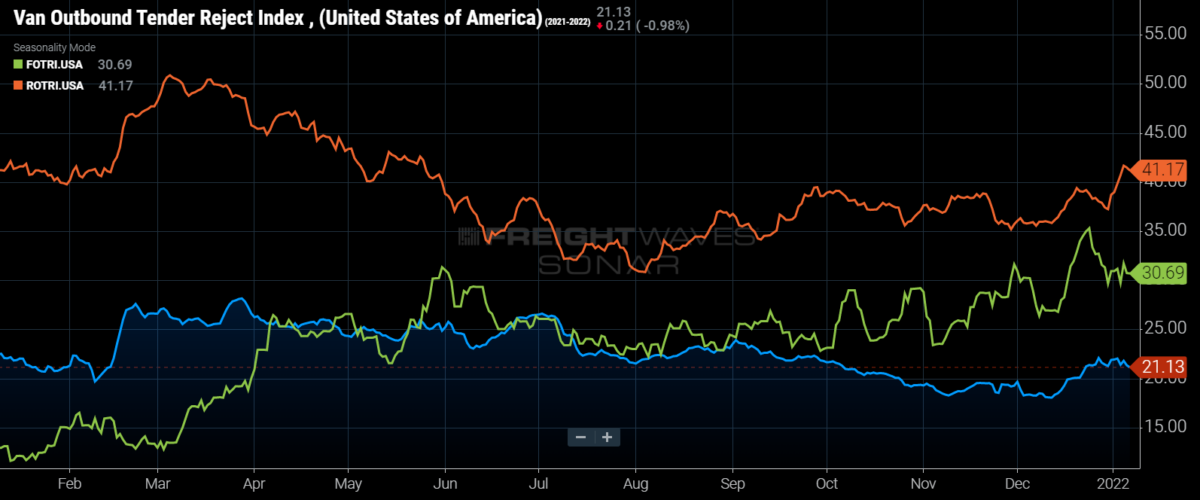

By mode: Reefer capacity tightened significantly over the past week as the Reefer Outbound Tender Reject Index (ROTRI) bounced above 40% again. ROTRI increased by 393 bps over the past week to 41.17%, the highest level since early June. Don’t expect the reefer market to loosen in any significant fashion, especially if winter weather intensifies during the next couple of months.

Van rejection rates have been pretty stable over the past week. The Van Outbound Tender Reject Index (VOTRI) fell just 14 bps over the past week to 21.13%. Expect that there will be a decline in van rejections in the coming weeks as capacity does return to the market following the holiday period.

The Flatbed Outbound Tender Reject Index (FOTRI) experienced a slight increase over the past week, rising by 104 bps w/w. FOTRI is off the recent all-time high but remains above 30%, signaling that securing flatbed capacity is still quite tedious.

Spot rates rebound as capacity comes offline

The spot rate data available in SONAR from Truckstop.com is updated every Tuesday with the previous week’s data.

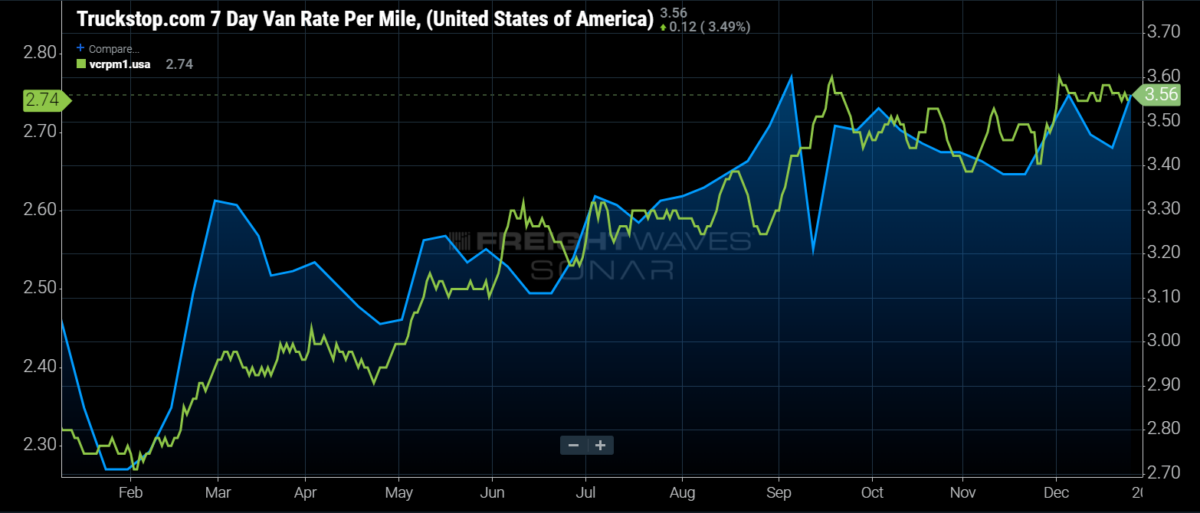

SONAR: Truckstop.com’s national spot rate (blue, right axis) and dry van contract rate (green, left axis).

To learn more about FreightWaves SONAR,click here.

The Truckstop.com national spot rate, based on the top 100 lanes on Truckstop.com’s load board, bounced back as capacity tightened. The national spot rate increased by 12 cents per mile to $3.56, including fuel surcharge and other accessorials, erasing all of the previous week’s increase. Even with the recent pullbacks, Truckstop.com’s national spot rate has maintained a near 20% gap with 2020 levels.

Of the 102 lanes from Truckstop.com’s load board, 80 reported increases last week. The Los Angeles to Portland, Oregon, lane took another large increase over the past week, increasing by 33 cents per mile to $4.96.

Contract rates were flat over the past week at $2.74. Contract rates are reported on a two-week lag, thus the impacts of the holidays have yet to be seen. Expect that contract rates will experience another uptick ahead of the first quarter of the year.

Contract rates, which are the base linehaul rate excluding fuel surcharges and other accessorials that are included in spot rates, are maintaining a similar gap as spot rates, running up 18% y/y.

FreightWaves’ Trusted Rate Assessment Consortium (TRAC) spot rate from Los Angeles to Dallas fell over the past week. The FreightWaves TRAC rate in this dense lane decreased by 5 cents per mile to $4.03. The falling spot rates are a result of capacity returning to Southern California following the holidays.

To learn more about FreightWaves TRAC, click here.

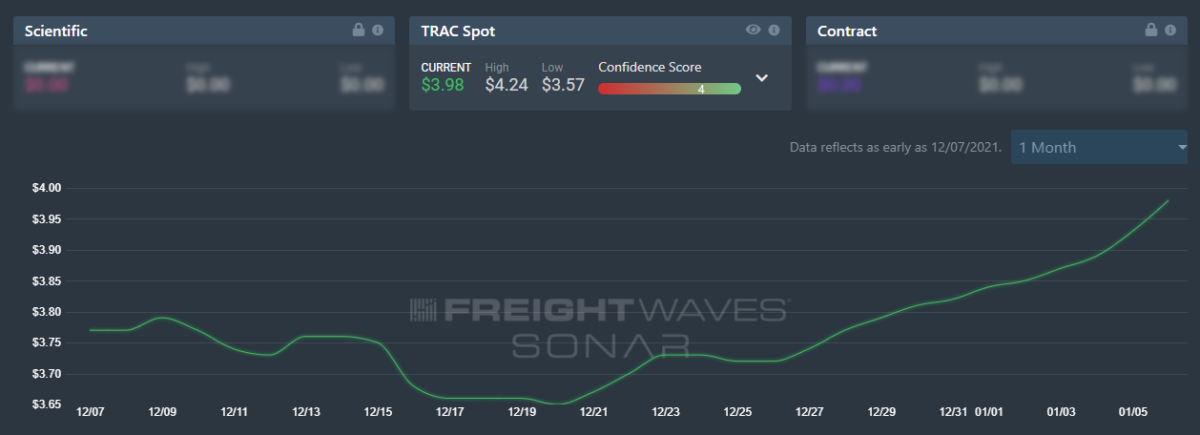

FreightWaves’ TRAC spot rate from Atlanta to Philadelphia has started to ramp up. The FreightWaves TRAC rate increased by 19 cents per mile to $3.98 over the past week. As capacity tightened, upward pressure on spot rates in this lane intensified.

To learn more about FreightWaves TRAC, click here.

As drivers return to the road following the holiday season, some of the upward pressure on rates will alleviate itself. Ultimately, pricing power will reside with the carriers, despite capacity being added to the market, as freight demand is unrelenting and the impacts of increased ocean bookings will keep demand elevated throughout the first quarter.

For more information on the FreightWaves Freight Intel Group, please contact Kevin Hill at khill@freightwaves.com or Tony Mulvey at tmulvey@freightwaves.com.

Check out the newest episodes of our podcast, Great Quarter, Guys, here.