Guest post by FreightWaves’ Todd Maiden

The Cass Freight Index Report showed further deceleration in the freight markets in May. Donald Broughton, Founder and Managing Partner of Broughton Capital and author of the report, warns an economic contraction could be underway.

Cass’ May 2019 report shows signs of weakness with both the shipments and expenditures data sets seeing year-over-year declines. The shipments index declined 6 percent year-over-year in May and the expenditures index (or the total amount spent on freight) declined 1 percent compared to May 2018.

In the report, Broughton lays out the change in his view of the economy since the beginning of 2019.

In the beginning of the year, he attributed the weak data to tough comparisons from prior periods and moved to being “more alert” to each incremental data point by the February report. The decline in the shipments index in March led Broughton to suggest a potential “change tack” approach to the data. April’s decline in shipments led him to say, “we see material and growing downside risk to the economic outlook.”

With a 6 percent decline in May, Broughton believes the market has shifted from “warning of a potential slowdown” to “signaling an economic contraction.” Further, he questioned if the May reading was significant enough to ponder second quarter 2019 GDP in the negative territory.

Broughton acknowledges that the monthly readings are up against tough comparisons and that the index has gone negative before without being followed by negative GDP.

“The weakness in spot market pricing for many transportation services, especially trucking, is consistent with the negative Cass Shipments Index and, along with airfreight and railroad volume data, strengthens our concerns about the economy and the risk of ongoing trade policy disputes. Weakness in commodity prices and the decline in interest rates have joined the chorus of signals calling for an economic contraction,” said Broughton.

Pricing was still in positive territory as the Cass Truckload Linehaul Index (measures linehaul rates excluding fuel) was up 1.2 percent year-over-year in May and the Cass Intermodal Price Index (inclusive of fuel) increased 4.2 percent.

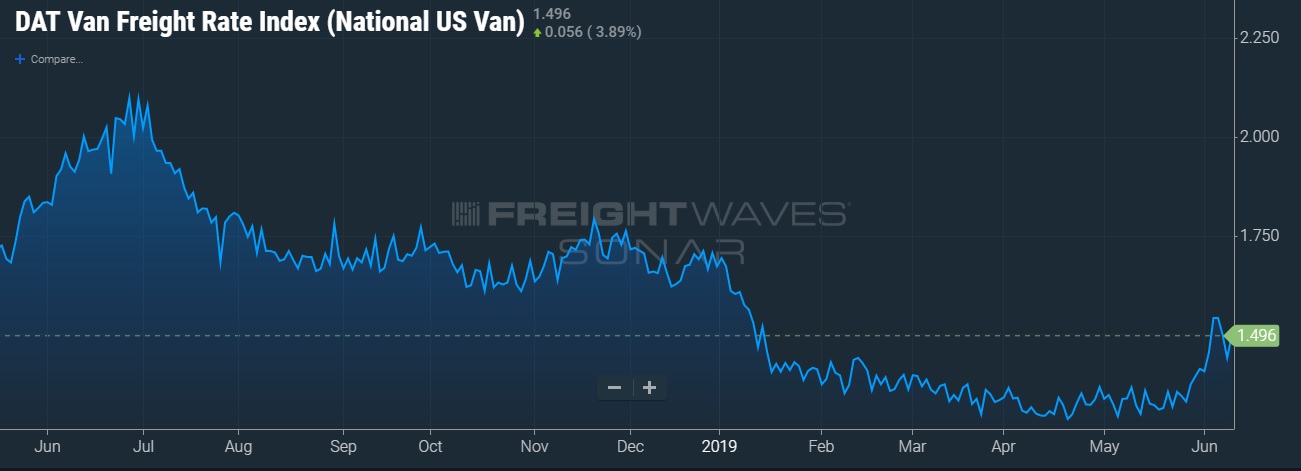

However, Broughton cautioned that the linehaul index “appears poised to go negative in coming months” and the intermodal price index “is also showing signs of significant sequential retreat.” FreightWaves has seen continued weakness in intermodal volumes as seen in the Intermodal Outbound Tender Rejection Index (USA).

Chart: FreightWaves’ SONAR

The Cass report follows a recent negative news cycle for the trucking and intermodal markets. In recent weeks earnings estimates have been lowered on the public truckload (TL) carriers, negative volume trends by the less-than-truckload carriers have been confirmed and the market has seen continued TL spot pricing weakness.

Chart: FreightWaves’ SONAR

Broughton continued, “We are concerned about the severe declines in international airfreight volumes (especially in Asia) and the ongoing swoon in railroad volumes, especially in auto and building materials. As volumes of chemical shipments have lost momentum in recent weeks, our concerns of the global slowdown spreading to the U.S., and the trade dispute reaching a ‘point of no return’ from an economic perspective, grow.”