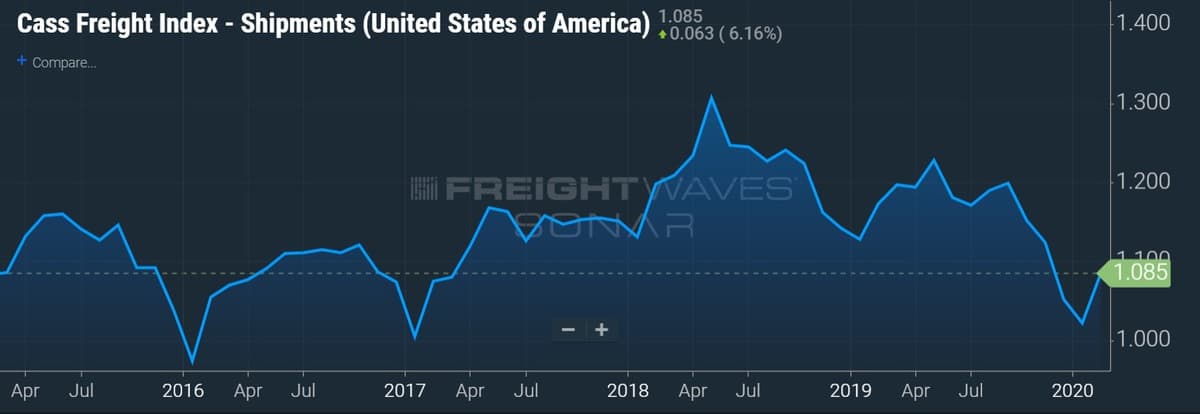

Negative trends in the transportation markets continued in February, according to freight data released by payment management solutions provider, Cass Information Systems Inc. (NASDAQ: CASS).

The Cass Freight Index fell again in February as the shipments index declined 7.5% year-over-year (y/y) with the expenditures index declining 6.8% for the month.

In January, the report’s author and Stifel Financial (NYSE: SF) equity research analyst David Ross was hopeful for a second quarter snapback as supply chains recovered from coronavirus-related disruption and import activity increased. A month later, that hope has somewhat diminished.

“This certainly puts some doubt around our view that the second quarter of 2020 could see actual y/y growth in domestic U.S. shipments and freight costs, as traditional seasonal freight patterns may not hold,” stated Ross. “We are hearing Chinese manufacturing activity is picking back up but at below-average levels. And then there is the issue of moving the goods produced out of the country and to the U.S., which may be limited by airfreight capacity, truck capacity, and/or container capacity.”

The positives, so to speak, were that the y/y declines in February were less severe than those seen in January and that shipment volumes improved 6.2% sequentially from January, which was in line with recent historical seasonality trends. For the last five years, the shipments index has improved 6.13% on average from January to February.

Further, Ross suggests that U.S. transportation markets entered 2020 with a bit of a headwind due to “elevated inventories,” which he now believes are bleeding off rapidly and may require restocking “before too long.”

Ross said that he will be looking to the airfreight markets for the first signs of recovery as retailers and manufacturers look to quickly replenish supply. Ross is calling for “at least a short period of large yield spikes for cargo capacity” as demand returns. He said that recent increases in airfreight yields have more to do with the lack of available cargo belly space throughout the market than improved demand.

While Ross suggested that January could have been the bottom for this cycle, he left open the potential for a “double dip or at least a delay in improvements,” noting a 23% y/y decline in imports at the Port of Los Angeles in February.

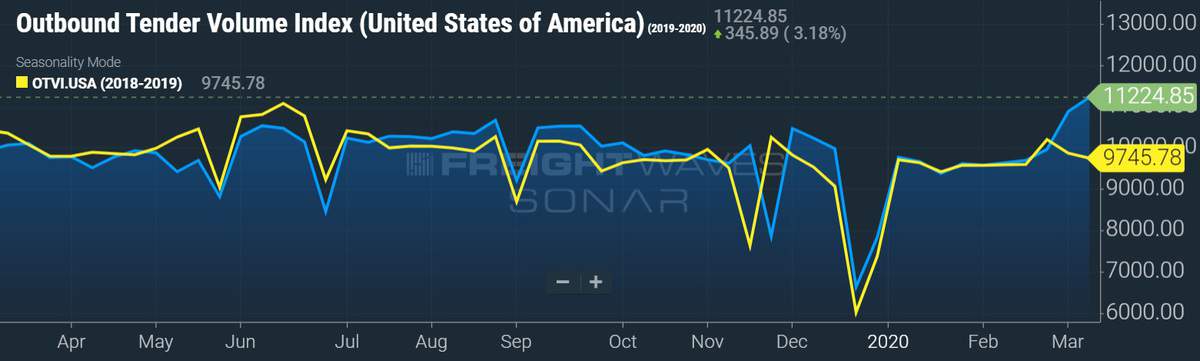

In recent days, FreightWaves has seen outbound tender truckload (TL) volumes inflect positively on a y/y comparison as many retailers have been replenishing their shelves given the run on household supplies caused by the outbreak.

The expenditures index was up 4.3% sequentially in February, but lagged the average seasonal improvement of 4.8% normally seen from January to February. Ross expects near-term pricing to remain soft, but still believes that increased regulation in the trucking industry as well as cost inflation will result in a purge of TL capacity from the market. A potential lack of capacity and the expectation for inventory restocking, should “drive rates higher again at some point this year.”

The Cass TL Linehaul Index, which measures per-mile linehaul rates, declined 6.1% y/y in February, similar to the rate of decline reported during January.

Ross said that he is now looking at demand as the driver for rate increases in 2020. He expects TL capacity to continue to exit the market, but indicated that the timing of the potential rate improvement, which many industry participants believed to be mid-2020 prior to the outbreak, is more dependent on volumes.

Further, he said that given the weakness in the linehaul index, which is closely correlated with yield results reported from the public TL carriers, it “looks like another weak first quarter ahead” for the group.

Lastly, the Cass Intermodal Price Index, which measures total per-mile cost for the “smaller intermodal market,” saw its largest y/y decline of this cycle at 5.1%. Depressed container import activity has resulted in declines in intermodal rail shipments. According to the latest weekly report published by the Association of American Railroads, U.S. intermodal rail traffic is down 7.7% year-to-date compared to the same period in 2019.

Ross expects intermodal pricing to rebound once TL pricing improves.

Cass processes more than $28 billion in freight payables on behalf of its clients annually.