The worst linehaul data in 15 years may suggest the bottom of the freight cycle

Payment management solutions provider Cass Information Systems’ (NASDAQ: CASS) freight index fell mightily in April as expected. The shipments component of the index dropped 22.7% year-over-year with the expenditures component off 18.2% as the U.S. economy felt the brunt of a full month’s worth of lockdowns.

The report’s author, Stifel Financial (NYSE: SF) equity research analyst David Ross, said April marks the bottom. “May should be better, as the U.S. economy slowly begins to reopen and some manufacturing plants turn back on (many automotive OEMs are targeting plant reopenings in the next week or two).”

The chorus of an April bottom is growing. Many trucking execs were on hand at the Bank of America Transportation and Industrials Conference earlier this week, voicing optimism around the pending economic restart.

Support for the thesis suggesting a bounce off the bottom is visible in FreightWaves’ Outbound Tender Volume Index (SONAR: OTVI.USA) as well. After bobbling along in the back half of April, May demand appears to have firmed.

Cass shipments data showed that April volumes fell 15.1% from March even as many “essential” goods providers — grocery, e-commerce, home improvement, etc. — remained operational. The index now stands in 2009 territory.

The 20%-plus drop in shipments is similar to what some public truckload (TL) and less-than-truckload (LTL) carriers have reported in recent days and weeks, and a little worse than what others have seen. Trucking hasn’t been the only mode to see the declines. Container imports on the West Coast were off a similar amount in April and U.S. weekly rail carloads continue to see 20% year-over-year declines. Intermodal traffic was down 16% year-over-year in the week ended May 9, according to the Association of American Railroads.

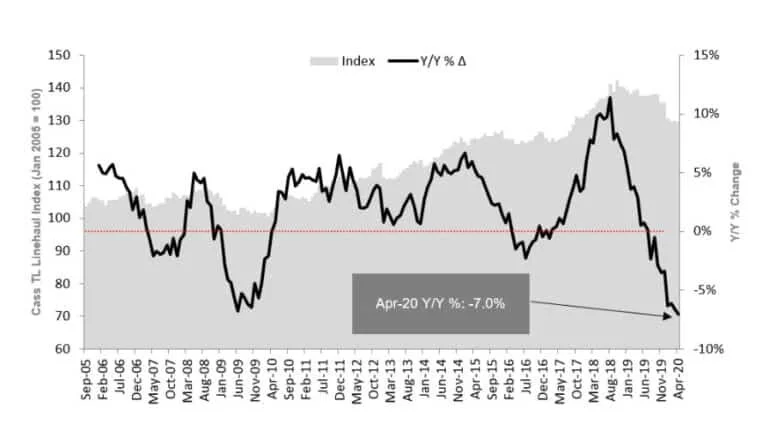

The Cass expenditures data was down 10.3% from March. The 18.2% year-over-year decline in April lagged the erosion in volumes even as diesel prices were 20% lower year-over-year on average, the TL linehaul index (which excludes fuel and accessorial charges) was down 7% and the intermodal price index fell 7.1%.

Ross chalked it up to a mix issue. He believes that longer lengths of haul drove revenue per shipment higher, softening the decline in expenditures relative to shipments. On a per-mile basis, TL linehaul rates recorded “the worst comp reported in the last 15 years,” down to “global financial crisis levels.”

“Supply and demand determine truckload rates, and there’s really nowhere to hide when volumes take a step down as dramatically as we saw in April,” Ross stated. “From here, the question is whether this negative industry pricing is enough to flush out capacity. And if so, how much?” Ross added that carrier failures need to exceed volume declines to make any impact on rates, noting that volumes “could stay down 10% or more.”

Of note, the TL linehaul index was only off 0.3% in April compared to March.

“We expect the spot market to bottom out soon,” Ross said, but he noted that how much and how quickly “will depend on the strength of the recovery coupled with the pinch of industry supply.”

Lastly, Ross believes the intermodal price index, down 3.3% sequentially in April, has reached the bottom as year-over-year declines in intermodal volumes are less severe currently than they were in April.

Cass processes more than $28 billion in freight payables on behalf of its clients annually.