Even as DAT spot rates start to slide from their recent highs, and analysts on earnings call ask executives if they believe the freight market may have peaked, another market index shows all green lights.

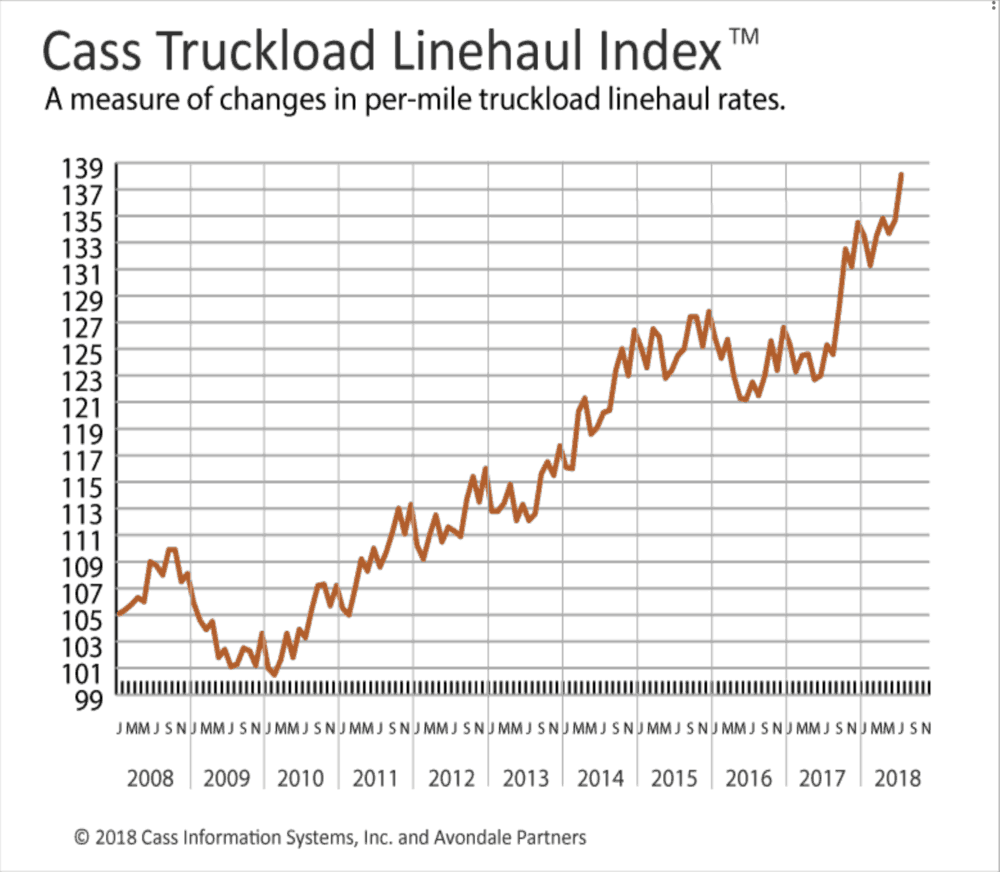

The July Cass Truckload Linehaul Index published Wednesday had its first double digit year-on-year increase since the pre-Great Recession boom of 2008. The index in July was 138.1, 10.2% more than the level of a year ago. Even in this current runup in freight rates, there has not been a year-on-year double digit increase in the Cass Linehaul Index before the July number. The index of 138.1 is the highest ever in the history of the index, which goes back to January 2005, the base year.

The Cass Intermodal Index was also up double digits year-on-year, though that is not as unique; the June index also was up by double digits, but not as much as the 12% posted for July. The rate of growth in July increase was described as the biggest year-on-year increase since July 2011.

The Truckload Linehaul index has now risen year-over-year for 16 consecutive months, though there have been some months sequentially lower than the prior year. July was not one of them; the 2.5% increase over June was one of the larger monthly gains during this bull market run. “Last month we increased our realized contract pricing forecast for 2018 from a range of 6% to 8% to a range of 6% to 12%, and current data is clearly signaling that the risk to our estimate may still be to the upside,” Donald Broughton, the principal managing partner of Broughton Capital and the official commentator for Cass said in the release accompanying the indexes. “We believe that this is the strongest normalized percentage level of truckload pricing achieved since deregulation.” He defined “normalized” as “except for extreme periods of recovery from recession.”

The Intermodal Index hasn’t had a year-over-year decline in almost two years. At 139.2, it is not at its all-time high, which was 143.2 recorded in March. But its 12% year-over-year gain does mark the biggest comparative 12-month increase since the index began its rise from its most recent 121.1 low of June 2016.

The 139.2 for July was 1.8% more than June 2018.

“Tight truckload capacity and higher diesel prices are creating incremental demand and pricing power for domestic intermodal,” Broughton said in his comments regarding intermodals. The Cass forecasts are for crude oil in a $45 to $65 range and diesel in $2.50 to $3.25. With average retail diesel in the U.S. at about $3.20, according to the EIA, and WTI crude at about $65—the top end of the Cass estimate—movement in the range can mostly only go down, which presumably would be bearish for intermodal. But that is movement in the range; prices can obviously go higher and wouldn’t need much to break out of the estimated range.

Cass defines the methodology on the intermodal index as being drawn from the actual invoices of its clients, for whom it is the initial payer. It is described as an “accurate, timely indicator of market fluctuations in per-mile U.S. domestic intermodal costs.” The costs are all-in: linehaul, fuel and accesorials. But the Truckload Index is based on movement in per-mile truckload linehaul rates, “independent of additional cost components such as fuel and accesorials.”

The strong Linehaul and Intermodal numbers were not the only healthy indices published by Cass this week. On Tuesday, the broader Cass Freight Index was published with 1.245 for its shipments index and 2.901 for expenditures. That expenditures index was a record for the index, which goes back to 1999. The shipments number was not, but it is the highest since 2007. Cass defines these indices as representing “monthly levels of shipment activity, in terms of volume of shipments and expenditures for freight shipments.”

Suggestions that the freight markets may have hit a peak—though not necessarily headed for a significant fall—have been fueled in part by weekly DAT spot rates. In the last four weeks, DAT average spot dry van rates have dropped to $2.18 per mile from $2.37; flatbeds have declined to $2.69 from $2.79; and reefer vans have fallen to $2.51 from $2.65.