Freight shipments and costs saw more subdued changes in July, according to data provided by Cass Information Systems on Monday.

The shipments subset of the Cass Freight Index inched 0.4% higher year over year (y/y) during the month and was 0.6% higher than June on a seasonally adjusted basis.

“Freight demand has flattened out this year with inflation near 9% and significant substitution from goods back to services,” ACT Research’s Tim Denoyer concluded. “Considering the extraordinary goods consumption during the pandemic, a reversal as services have reopened shouldn’t be much of a surprise.”

The y/y increase in volumes during the month was the first since March. However, Denoyer expects shipments to see a modest y/y dip during the third quarter, followed by a 4% to 5% decline in the fourth quarter, assuming normal seasonality holds. The November and December comparisons to 2021 are formidable, as shipments accelerated to close the year. Those two months registered the highest two-year-stacked increases of all of 2021.

Retail inventories, a major watch item for truckload carriers and often a signal for future freight demand, are not overly concerning at this juncture according to Denoyer. “Inventory to sales ratios are still below historic norms, so this major tailwind for freight demand over the past 18 months is likely fading but has not turned to a headwind at this point.”

| July 2022 | y/y | 2-year | m/m | m/m (SA) |

| Shipments | 0.4% | 16.1% | -1.7% | 0.6% |

| Expenditures | 28.2% | 83.5% | -3.6% | -2.4% |

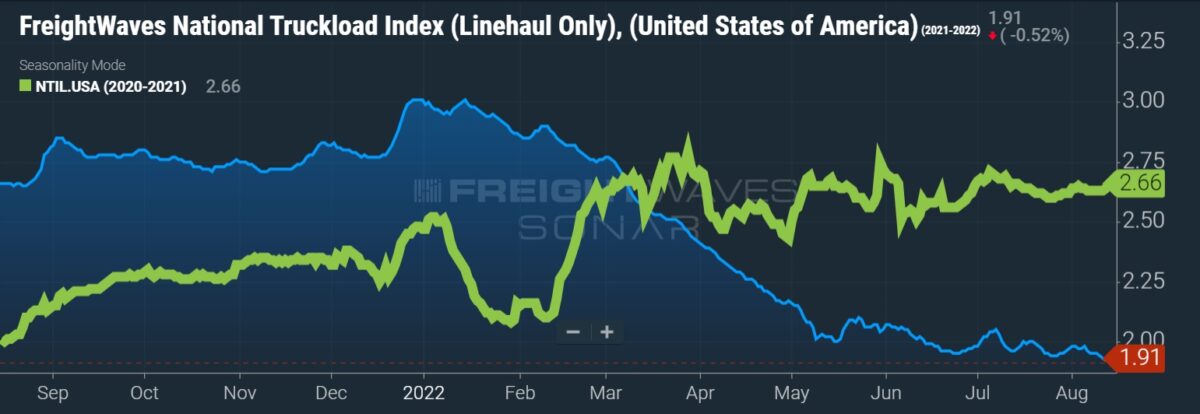

| TL Linehaul Index | 10.5% | 25.3% | -1.8% | NM |

Freight costs continued to increase substantially. Cass’ expenditures data set slipped 2.4% seasonally adjusted from June but was 28.2% higher y/y. The all-in index includes fuel costs, which began to retreat during the month, explaining some of the sequential decline.

Diesel fuel prices remained elevated in July, more than 60% higher y/y according to the Department of Energy. Roughly 8 to 10 percentage points of the y/y increase in the expenditures index are tied to higher fuel costs, the report said.

July was the first time since February the y/y increase accelerated from the prior month, although the report noted this is “likely short-lived.”

Normal seasonality for the remainder of the year implies a 23% y/y increase for the expenditures subindex in 2021, with December likely marking the first y/y decline in costs since August 2020.

The TL linehaul index, which excludes fuel and accessorial surcharges, was up 10.5% y/y in July, the smallest increase of the year. The index fell sequentially for the second straight month, down 1.8% from June.

“After an extraordinary truckload rate cycle over the past two years, the market balance has shifted, with capacity now growing briskly and demand falling slightly year to date,” Denoyer said. “Similar to what has occurred in the spot market, the surge in fuel costs to shippers, which are excluded from this index, will also likely act as a brake on linehaul rates.”

The index is only off 3.5% from the all-time high established in May.

Inferred rates, or expenditures divided by shipments, increased 27.6% y/y in July. The index was 2.9% lower seasonally adjusted from June. A modest step down in fuel prices and a looser TL market were the catalysts for the sequential decline.

“With the tight supply/demand balance in U.S. trucking markets easing considerably this year, industry rates are topping out and set to slow sharply in the months to come,” Denoyer continued. “While shippers aren’t seeing any real savings yet, such relief is now highly probable, which is welcome news for the broader inflation picture.”

Data used in the Cass indexes is derived from freight bills paid by Cass (NASDAQ: CASS), a provider of payment management solutions. Cass processes $37 billion in freight payables annually on behalf of customers.

More FreightWaves articles by Todd Maiden

- Transportation capacity rises again in July, pricing declines, report says

- Schneider sees moderating demand, expects ‘constructive’ back half

- Forward Air CEO: ‘If there is a recession, bring it on’