The views expressed here are solely those of the author and do not necessarily represent the views of FreightWaves or its affiliates.

In 2018 there was enthusiasm about building more locomotives. In retrospect, that strategic outlook probably was not well thought out.

Planners and investors didn’t anticipate a trade war. They were not clearly computing the impact of a robust swing towards more asset shrinkage from the so-called precision scheduled railroading (PSR).

After all, it appeared statistically that both rail carload and intermodal volumes had been on something of a run-up into 2018.

There were signs at the end of 2017 of very tight trucking capacity – soon to be made worse by the regulatory requirement for electronic logs and the often-mentioned trucking industry labor shortage.

Both GE Transportation and Wabtec Corp. were optimistic as they saw the railroads pulling both freight cars and locomotives out of storage and the expectation of higher locomotive sales to the North American Class I railroads as well as to short lines.

As an optimistic sign, Omaha, Nebraska-based Union Pacific Railroad pulled 650 locomotives out of storage and added employees to the “overloaded” southern part of its network – particularly in Texas.

Progress Rail, among other locomotive builders, articulated that railroads were not just in the market for new power. They were also looking to update older locomotives of all sizes.

GE Transportation and Wabtec went ahead and announced their roughly $11 billion merger in May 2018.

What could go wrong? As it turns out, quite a lot…

The optimists discounted the trade war impacts and long period of uncertainty. They ignored the 2018-2019 resurgence of the trucking sector taking additional freight share.

They missed the risks associated with the severe flooding in 2019. They didn’t add up the number of locomotives being made surplus by the execution of longer PSR trains.

The phenomena of stored locomotives is not a new issue. We have seen this before. We saw the excess locomotive risks back in 2002 and again in 2009. The year 2020 should not be a complete surprise.

Jim Husband, president of RailSolutions Inc., had cited the previous risks. For example, he reported previously that between 2001 and about 2003, the Class I railroads stored as many as 4,000 to 5,000 locomotives. After that, they started ordering new locomotives again and largely scrapped the older stored units.

The year 2006 was the last of the really high freight volume growth years for railroads. When the Great Recession hit, the various Class I railroads stored locomotives “in droves.”

In the spring of 2009, Union Pacific had stowed 2,100 locomotives. That was 25% of its 8,400-unit fleet in that year. BNSF told its investors that it has over 900 stored or “returned” locomotives. In the east, CSX Transportation had parked 600 locomotives, or ~16% of its 3,800-unit fleet. Norfolk Southern had stored 400 locomotives or ~11% of its fleet. Canadian Pacific had stowed 23% of its fleet.

Prior to that, how many locomotives had they been ordering? Collectively, about 900 a year between about 2004 and 2008 by one estimate.

Where are we today in 2020?

Orders for new locomotives had been much lower over the period between 2016 through 2019. It wasn’t unusual to see fewer than 500 new orders each year from the seven Class I railroads.

There were multiple reasons for the order declines. One reason was the increasing fuel burn penalty as Tier 4 EPA pollution controls were imposed on the most recent locomotive types.

A look at the different EPA Locomotive Emissions Levels under 40 CFR 1033 USA rules:

As a result, several of the big railroads decided to rebuild their older Tier 1 and Tier 2 locomotives rather than buy new ones.

The price of a modernized older locomotive – with its better fuel economy – is about 30% to 40% less than an all new locomotive handicapped with Tier 4 restrictions.

Here is the current market view of freight locomotives as of the early second quarter of 2020.

Between 20% and 25% of Class I railroad locomotives might be considered surplus and “stored.”

We will learn more in the railroads’ quarterly earnings releases and conference calls. In the meantime, here are some indicators to watch for:

BNSF had 2,500 locomotives “parked” as of the end of March 2020. Union Pacific has about 3,000 to 4,000 sidelined according to several unconfirmed sources.

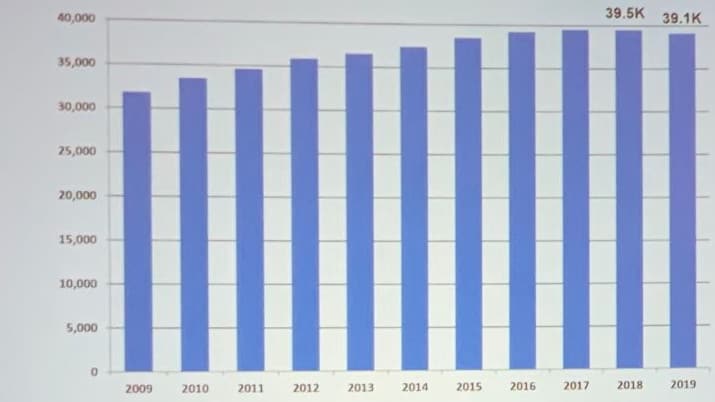

There were 39,100 locomotives registered in the North American official UMLER fleet file as of the end of December 2019. A 20% stored estimate would be ~7,820 units. A 30% stored estimate would be about 11,700 units.

Here in a graph is how big the fleet of UMLER active locomotives is as of year-end 2019.

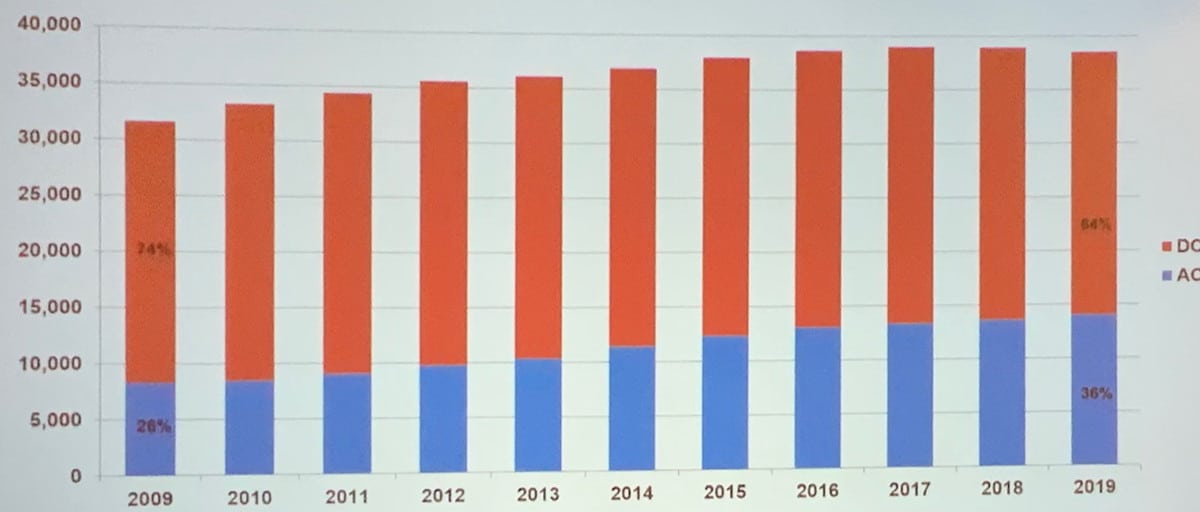

Over the past two decades, most of the main line locomotives switched from direct current (DC) power to more efficient alternating current (AC) power. The next graph shows the distribution between DC and AC units.

What’s an older locomotive worth? Norfolk Southern is selling or otherwise disposing of a combined 700 locomotives. A simple calculation suggests that the 700 units are about 20% of Norfolk Southern’s active fleet of 3,900 locomotives reported at year-end 2019.

If we use the Norfolk Southern estimated $385 million accounting charge for that, it suggests a $550,000 or so write-off per unit.

Those locomotives do have a potential resale or lease value. However, that value is realistic only if there are buyers. Are there enough buyers this spring of 2020?

In early March 2020, three different Railway Finance La Quinta (REF20) presenters discussed the market outlook for new locomotives. The message was that at best fewer than 250 all new freight locomotives would be built for the North American market this year.

Given the extreme low prices of diesel fuel and the current outlook for U.S. gross domestic product for 2020, the March expectations may no longer be valid.

Rebuilding as modern units on old frames and body shells might be the more likely outcome, since the relative costs would be much lower than new locomotives.

Is there a market for selling and buying older stored units? Yes, that’s possible.

Multiple speakers at the REF20 show suggested how much more affordable used units are than new ones. The buyers? They would be short lines and some industrial railroads. Or possibly overseas buyers that are looking for a great bargain price.

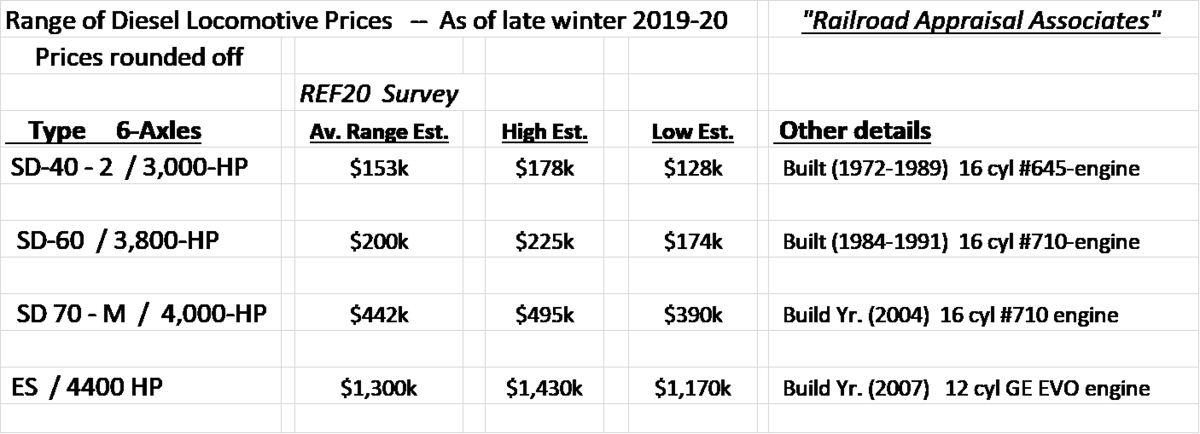

Here are just a few examples of the resale prices as of late winter 2019-20. Prices might be even lower now in the spring. The price estimates are for units still in good physical condition.

Prices are a broad estimate and not necessarily statistically accurate as to sample size. It is an attempt to discover the range of reasonable market values.

Remember that multiple brokers who specialize in these types of transactions should be consulted for more accurate estimates and negotiations with sellers.

Note that the cost to modernize these units as extensive rebuilds with new electrical and traction control upgrades would involve additional capital investment.

The four diesel-electric locomotive types shown are typically among the most used locomotives in the North American market. Each type has its own strengths and weaknesses.

Given the recognized long life of railroad locomotives (40 to 50 years – and sometimes beyond), these units were selected as ones to consider instead of buying a new mainline road unit at $2.5 to $3.2 million price ranges. A modernized and rebuilt unit price is perhaps in the $1.5 to $2 million range.

My personal favorites as a rail economist are the SD 40-2 type and the SD-70 series. Others I recommend considering include the GE Dash 9 units. There are more than 10 other types a regional railroad or a short line might consider.

If experienced in such transactions, what’s your favorite type?

Selected references:

- Progressive Railroading – Report by Pat Foran, editor; June 2009

- Patrick Mazzanti, President – Railroad Appraisal Associates

- Steven Beal, President – National Railway Equipment

- Tom Chenoweth, Assistant Vice President of Product Development – National Railway Equipment

- Greg Schmid, Managing Director Rail Marketing – Residco

- Jason Kuehn, Vice President – Oliver Wyman

- Glen Rees, Rail Business Director – North America – Cummins