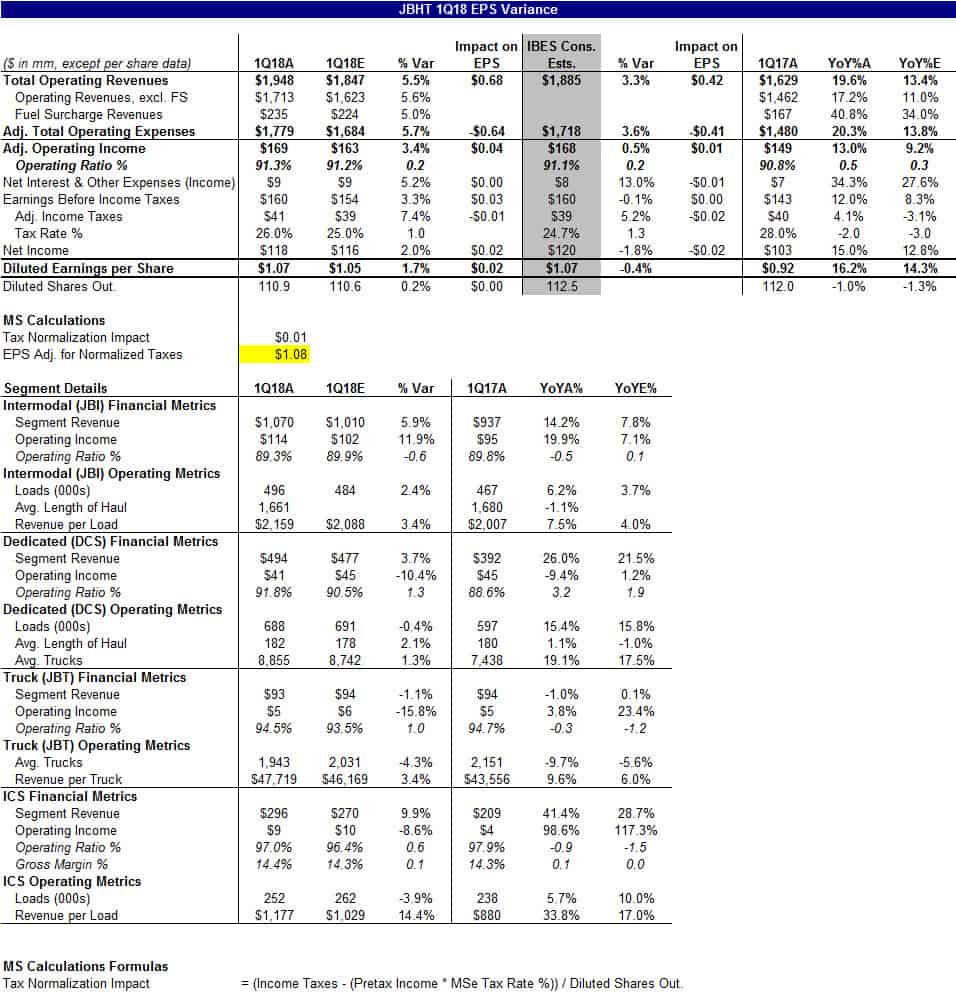

The first major transportation provider out of the box with first-quarter earnings has posted a better-than-expected result in revenues with J.B. Hunt Transport Services reporting total operating revenue of $1.95 billion, beating analyst estimates of $1.88B, this morning. The company said first-quarter net earnings were $118.1 million, or diluted earnings per share of $1.07, vs. 2017 first quarter results of $102.7 million or 92 cents per diluted share.

J.B. Hunt reported operating income rose from $149M in the first quarter of 2017 to $169M in 2018, benefiting from volume and rate growth. In a release, the company also noted a “vibrant spot pricing market” that was partially offset by “increased purchased transportation costs; lower intermodal network utilization; lower productivity in winter weather affected regions; higher driver and non-driver salaries, wages and benefits; higher Final Mile Services (FMS) network facilities costs; higher maintenance costs on equipment scheduled to be traded in 2018; increased technology spend on legacy system upgrades; continuing branch network expansion; increased equipment ownership costs and increased insurance and claims costs.”

Net interest expense for the quarter increased 34% from 2017 due to higher interest rates on the company’s debt, which totaled $1B, up from $951M as of March 31, 2017 but down slightly from Dec. 31, 2017’s total of $1.09B.

Total operating revenue for the current quarter was $1.95B compared with $1.63B in the first quarter of 2017. Excluding fuel surcharges, current quarter total operating revenue increased 17%.

Within its operating divisions, Intermodal load growth was 6% and revenue per load excluding fuel surcharges increased approximately 4% over first quarter 2017 levels, the company said. Dedicated Contract Services (DCS) segment revenue increased 26% over prior year, primarily from additional customer contracts from a year ago and customer rate increases. Integrated Capacity Solutions (ICS) load growth was 6% and revenue per load increased approximately 34% over the same period in 2017. Truck (JBT) segment revenue decreased 1% primarily from fewer seated trucks compared to a year ago.

In the Intermodal division, revenue grew approximately 14% to $1.07B and operating income increased 20% to $114M.

Follow J.B. Hunt’s stock price on FreightWaves’ Stock Watchlist

“Benefits from volume growth, customer rate increases and freight mix were partially offset by an increase in rail purchased transportation costs; reduced network utilization and lower dray efficiency created from rail congestion, customer equipment pool utilization and a tight third party dray market; higher equipment ownership costs; increased driver wages and recruiting costs; increased costs for onboarding and integration of container tracking technologies and insurance and claims costs compared to the same period in 2017,” J.B. Hunt said in a release.

The company ended the first quarter with approximately 89,500 units of trailing capacity and 5,450 power units assigned to its dray fleet.

J.B. Hunt’s Dedicated Contract Services (DCS) performed well in the quarter with revenue climbing 26% to $494.5M and operating income dropping 9% to $41M. Productivity (revenue) per truck was also up approximately 5%. Within DCS is the company’s Final Mile Services (FMS) segment, which posted a $35M, or 75%, increase in revenue compared to first quarter 2017. Twenty-five million of that is related to a July 2017 acquisition.

DCS saw fleet growth of 1,329 additional revenue producing trucks in the quarter compared to Q1 of 2017. Approximately 55% of these additions were private fleet conversions, the company said, with 32% representing FMS vs. traditional dedicated capacity fleets. Customer retention in the division is above 98%, J.B. Hunt said.

The company’s Integrated Capacity Solutions (ICS) division also posted big gains, with revenue climbing 41% to $296.1M and operating income up 99% to $9M. Volumes in the division were up 6% while revenue per load increased 34% due primarily to the spot market pricing.

“Spot volumes increased 43% and contractual volumes decreased approximately 7% from a year ago,” J.B. Hunt said. “Contractual business represents approximately 67% of total load volume and 44% of total revenue in the current period compared to 76% and 63%, respectively, in first quarter 2017.”

The company noted that $96M of the total revenue came through its J.B. Hunt 360 marketplace. The continued rollout of the platform, though, also drove up costs. Gross profit margin inched up 0.1% to 14.4% in the quarter, which the company attributed to higher spot market pricing.

ICS increased its carrier base 15% over first quarter 2017 and added 14% more employees.

In its Truck division, J.B. Hunt was hit by the driver shortage with an average of 162 unseated trucks during the quarter, higher driver and independent contractor costs per mile, and higher recruiting costs per driver and contractors. The division posted revenue of $92.7M, down 1% from 2017 Q1 and operating income of $5M, up 4%.

J.B. Hunt experienced a 15% decrease in load count and saw a 10% decrease in tractor count to 1,926 units. Revenue per load excluding fuel surcharges increased 14%, primarily from a 10% increase in rates per loaded mile and 3% increase in length of haul compared for the first quarter of 2017.