The $8 billion acquisition of experience management software startup Qualtrics, announced in January, has led SAP (NYSE: SAP) to underperform Wall Street expectations and post an operating loss for the first quarter of 2019.

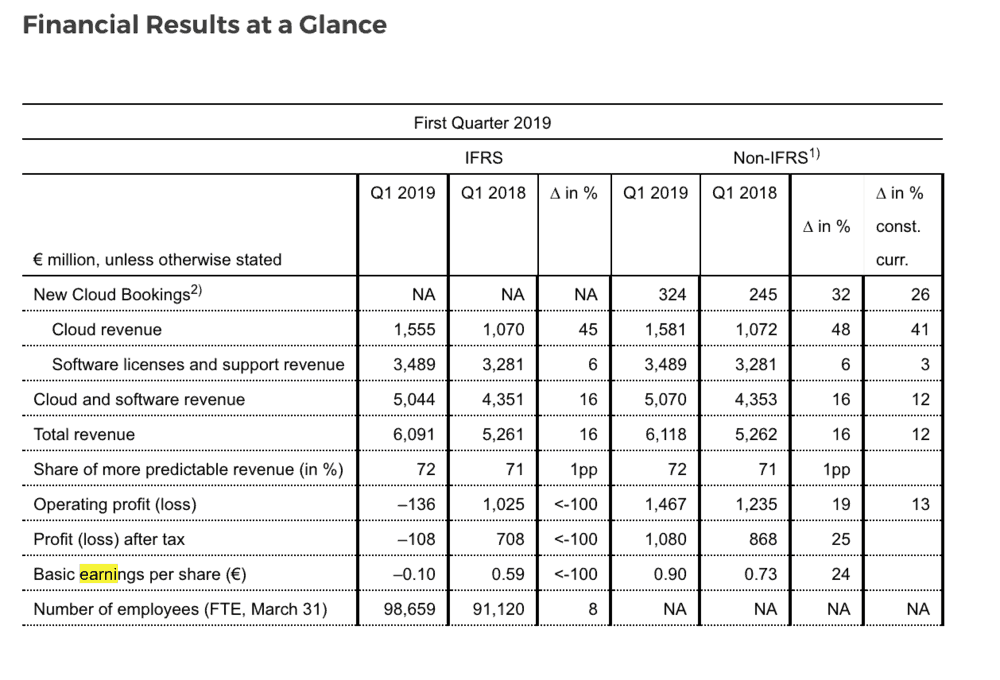

The enterprise software giant posted earnings per share of -€0.10 according to International Financial Reporting Standards (IFRS), and €0.90 per share on a non-IFRS adjusted basis. In the first quarter, SAP’s non-IFRS revenues amounted to €6.11 billion (non-IFRS), representing 16 percent growth year-over-year.

The first quarter is normally the weakest for SAP in terms of cloud revenue and new software licenses, but, including the acquisition, SAP managed to grow cloud revenue by 48% year-over-year to €1.58 billion in the first quarter, exceeding J.P. Morgan’s expectations of 46% growth.

“SAP’s results are another illustration that we are a rarity in the enterprise applications software industry,” said CEO Bill McDermott in a statement. “We have a strong core business, the fastest growing cloud at scale in enterprise software and impressive non-IFRS operating profit growth. We are focused on leading a best-run SAP so we can drive significant margin expansion in the quarters ahead.”

SAP’s core enterprise resource planning (ERP) system, S/4HANA, launched in 2015, has achieved significant traction. S/4HANA is the first version of SAP’s ERP that is optimized for and runs only on SAP’s database platform. That software comes in both on-premise and cloud versions, though the company is encouraging its clients to shift to its higher operating margin cloud business.

Enterprise software companies deploy large amounts of capital in research and development of new products and features, funded by stable, annually-recurring revenue from subscriptions. SAP reports the proportion of its revenue that is ‘more predictable’, i.e., recurring: more predictable revenue represented 72% of total revenue in the first quarter of 2019, up 1 percent year-over-year.

In theory, the acquisition of Qualtrics will help SAP understand and serve its customers better. Qualtrics canceled an initial public offering that would have valued the company at $4.21 billion in January 2019 and instead sold to SAP for $8 billion. Despite the high multiple paid, Qualtrics’ leadership in the ‘customer experience’ category should eventually allow SAP to refine the way it retains and upsells customers based on their actual use of the platform.

“Experience data (X-data) focuses on obtaining and tapping the value of outside-in customer, employee, product and brand feedback. Combining Qualtrics’ experience data and insights with unparalleled operational data (O-data) from SAP software will enable customers to manage supply chains, networks, employees and core processes better,” SAP said in a statement announcing the acquisition.

SAP had warned last quarter that the earnings hit from the Qualtrics acquisition and a subsequent company-wide restructuring (including loss of senior management and headcount reduction via buyout in SAP’s database business) would largely be confined to the first quarter of 2019, and in many analysts’ view, the market had digested and priced in the news.

“We think a lot of the bad news that had surfaced in the last six months has been FY digested by the market, and although the shares have performed well YTD, this has been largely driven by a beta rally, and in fact SAP has underperformed vs. SX8E and peer Oracle,” wrote J.P. Morgan equities analyst Stacy Pollard in an April 18 client note. “We therefore see SAP shares as back in line with the broader market – which admittedly has less upside than four months ago.”