Conagra sees evidence of continued consumer caution

Conagra shares are down 26% in the past year. (Chart: Barchart.com Inc.)

One of the biggest CPG events of 2023 was Conagra Brands highlighting a shift in consumer behavior last spring. At that time, it became increasingly evident that inflation was pressuring grocery store purchases, such as consumers making meals from scratch instead of more convenient ready-made meals that Conagra sells. Management considers those shifts temporary. On Thursday’s analyst call, while still labeling those shifts temporary, management said it sees lingering evidence of consumer caution and that shift back to “normal” has been slower than expected. Accordingly, management cut sales guidance for its fiscal year to a decrease of 1%-2% from guidance of a 1% increase. Even so, the company put a positive spin on volume declines by citing a narrower year-over-year volume decline in fiscal Q2 of 3.5%, relative to year-over-year volume declines of 7%-9.9% the prior three quarters. CEO Sean Connolly said, “the supply chain is humming again, especially on key brands and around merchandising windows.” In addition, its now-fluid supply chains mean there are more opportunities for new product introductions, such as canned Wendy’s chili. Management also cut margin guidance — to 15.6% from 16%-16.5%; the company is expecting 3% cost inflation this year with inflation in tomato-based ingredients more than offsetting deflation in edible oils.

Health to be major CPG focus this year

These two Just Food articles (here and here) described that trend well and also challenged my thinking on plant-based foods. Rather than being dead in the water, the possibility remains for the category to recover from the past two years’ challenges by adjusting formulas. The misstep wasn’t just that plant-based alternatives offered worse taste at higher prices (a tough sell in any environment, but particularly when living costs rise), but also that the demographic interested in plant-based alternatives wants to avoid ultraprocessed foods. In short, consumers were unconvinced that plant-based alternatives were any healthier. Food companies could shorten their ingredient lists and remove ingredients that are difficult to pronounce, a tip of the hand that the food is ultraprocessed.

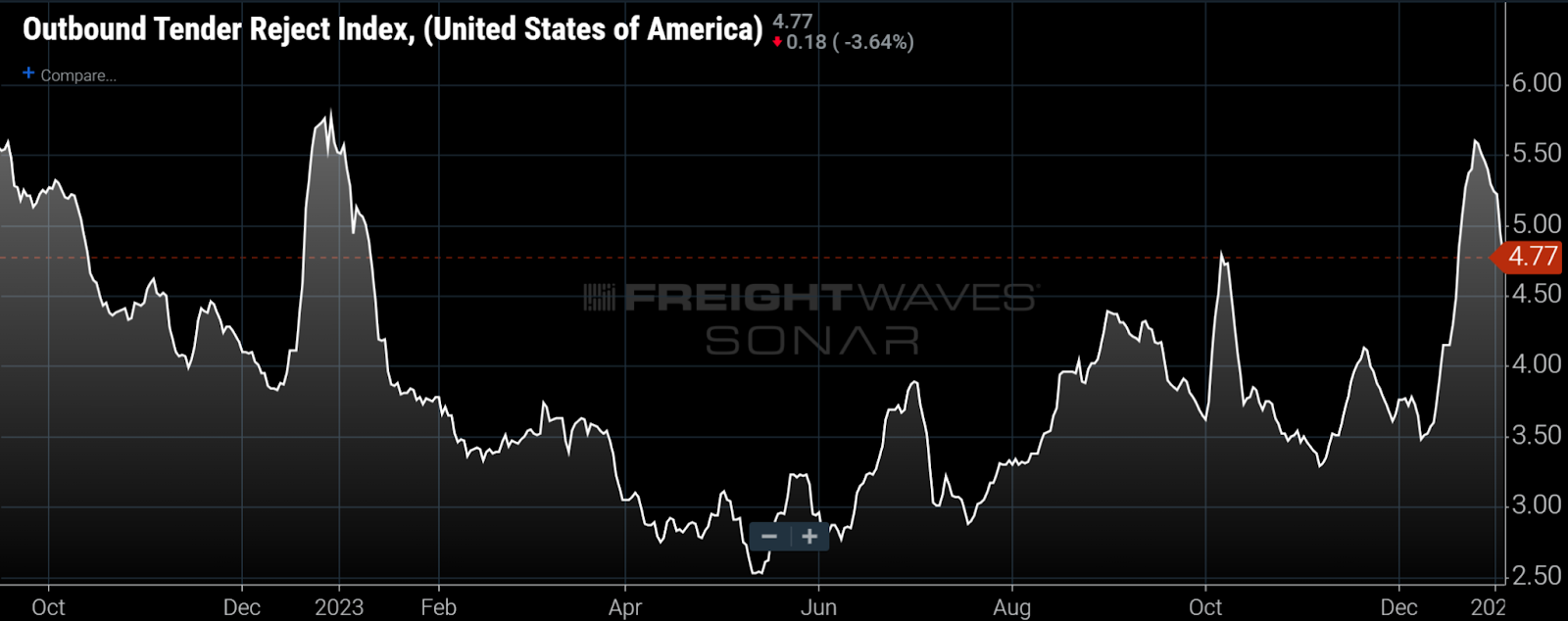

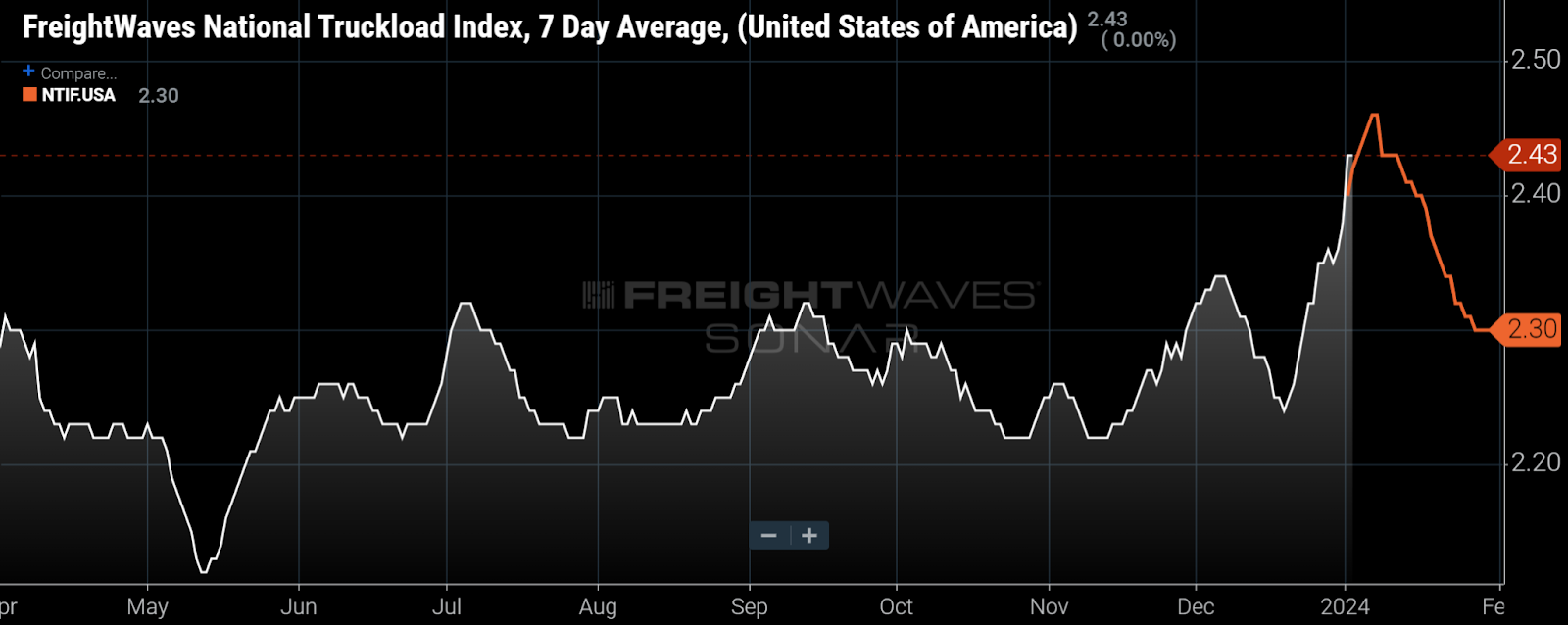

Tender rejection rates likely to stay below 5% amid seasonal weakness

Red Sea turmoil could boost rail intermodal volume

While the trade lanes that traverse the Red Sea and Suez Canal are far more important for Europe than for North America, the situation is also having an impact on rates and routings for Asia-to-U.S. cargo. Prior to the attacks, ocean carriers, including Maersk, had been diverting vessels away from trans-Pacific routings in favor of routings through the Suez Canal in response to drought conditions at the Panama Canal. The situation changed by the day as ocean carriers have taken different approaches and have gone back and forth on whether they would traverse the region. If the attacks continue, a greater share of U.S. imports would traverse trans-Pacific routes, hitting the U.S. West Coast. Freight hitting that coast is far more likely to move via rail intermodal than freight that hits the East Coast ports. (Some estimates are 65%-70% versus 20%-25%.) In addition, longer routes’ avoidance of the Red Sea not only reduces the productivity of oceangoing vessels, but also reduces the productivity of international containers, including disrupting the repositioning of those containers. The potential for a scarcity of international containers encourages the transloading of imported goods hitting the West Coast ports from international containers to domestic containers, which could benefit carriers including J.B. Hunt, Hub Group and Schneider. For ongoing coverage of the Red Sea, see our maritime articles here.

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.