China’s Cosco Group — the world’s fourth-largest container line operator with an 11% market share — finally closed its books on 2022 just as the first quarter of 2023 came to an end.

The Chinese company’s results highlight the steep decline that began last year and that continues through today. Early revenue reporting on the first two months of this year by Taiwanese carriers indicate the first quarter could be down 40% or more from Q4 2022.

The takeaway: Liner profits are plummeting, but they’re coming down from such lofty levels that they still have a long way to go before reaching net-loss territory.

Industrywide profits for 2022, predictions for 2023

After Cosco belatedly released its results, independent analyst John McCown published his overview of container shipping profits for last year and his predictions for this year.

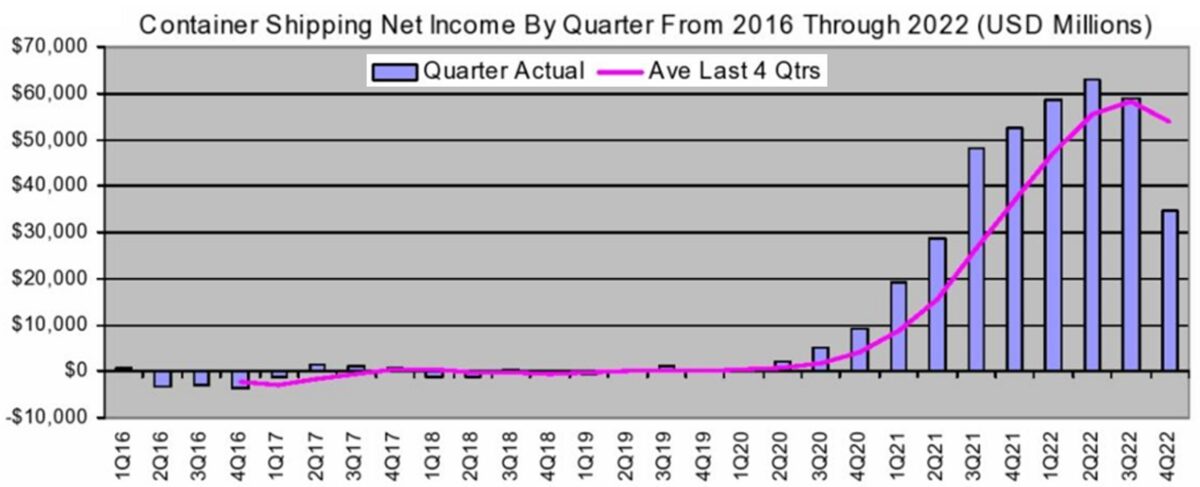

According to McCown’s data, container shipping companies earned a jaw-dropping aggregate net income of $215.3 billion in 2022. Profits in Q4 2022 totaled $34.7 billion, down 34% year on year (y/y) and 41% from the third quarter.

McCown predicts shipping lines will earn $43.2 billion in 2023, down 80% y/y. He assumes industry net income will drop to $14.9 billion in Q1 2023, a sequential fall of 57% versus the fourth quarter. He estimates net income will then fall to $10.8 billion in Q2 2023 and to $8.7 billion in both the third and fourth quarters.

Lars Jensen, CEO of Vespucci Maritime, dubbed McCown’s 2023 estimate “a bullish forecast.” Jensen said it’s “not out of the question” but would require the demand downturn to end in the face of high inventories and carriers to manage capacity given an onslaught of new ship deliveries.

Prior to Cosco’s results announcement, Sea-Intelligence estimated that industrywide earnings before interest and taxes would come in at $208 billion for 2022, following EBIT of $164 billion in 2021 and $24 billion in 2022.

“While it is hard to estimate historical industry EBIT, by our best estimates, the carriers have, over the past three years, made far greater operating profits than they did in the combined previous 63 years, since the maiden voyage of the first container ship,” said Sea-Intelligence.

Cosco results confirm Q4 plunge

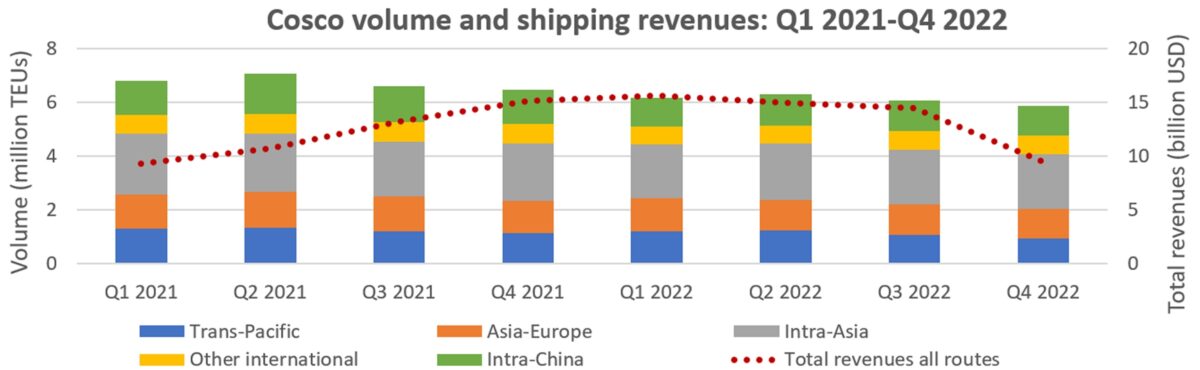

Looking specifically at Cosco’s liner business (excluding its terminals division), the group’s container shipping unit posted net income of $20.32 billion for full-year 2022, up 22% y/y.

However, that gain was heavily weighted toward the beginning of the year.

The shipping division (which includes liner companies Cosco and OOCL) reported net income of $2.68 billion for Q4 2022, down 37% y/y and a 53% plunge from the third quarter.

Cosco’s quarterly shipping net income reached its cycle peak in Q2 2022, at $6.76 billion, more than double profits in the latest period.

The company’s shipping revenues peaked in Q1 2022, at $15.62 billion. By the fourth quarter, shipping revenues had declined to $9.47 billion, 39% off the high.

Container volume also came down, particularly for Western trades. Cosco’s liner companies carried 5,877,589 twenty-foot equivalent units worldwide in Q4 2022, down 9% y/y. Its liner companies’ trans-Pacific volumes fell 15.5% y/y, with Asia-Europe down 12%. Volume in the company’s highest-volume market — intra-Asia — declined only 3% y/y.

Revenue per FEU vs. spot indexes

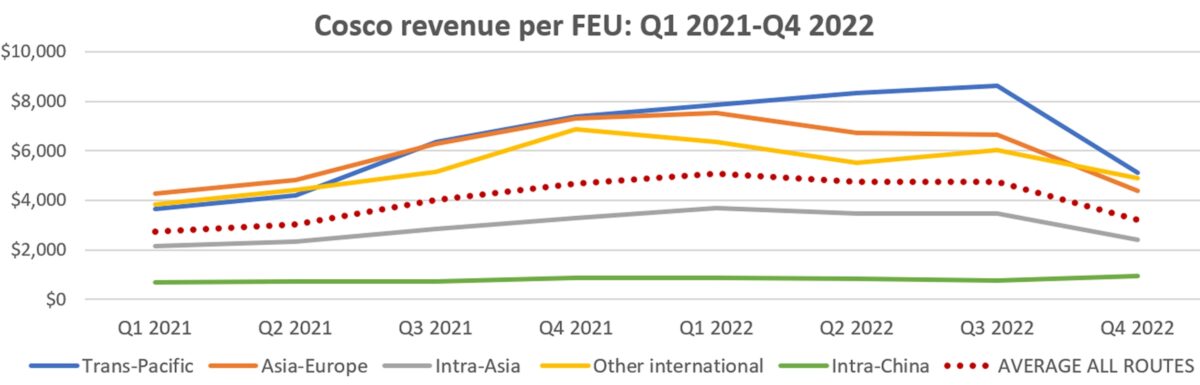

The company’s revenue per forty-foot equivalent unit peaked globally back in Q1 2022, at $5,072 per FEU. By Q4 2022, revenue per FEU was down to $3,223, 36% off the high.

Q4 2022 revenue per FEU was down 31% y/y and 32% sequentially versus the third quarter. The biggest sequential drop was in the trans-Pacific, where Cosco’s revenue per FEU fell 41% quarter on quarter.

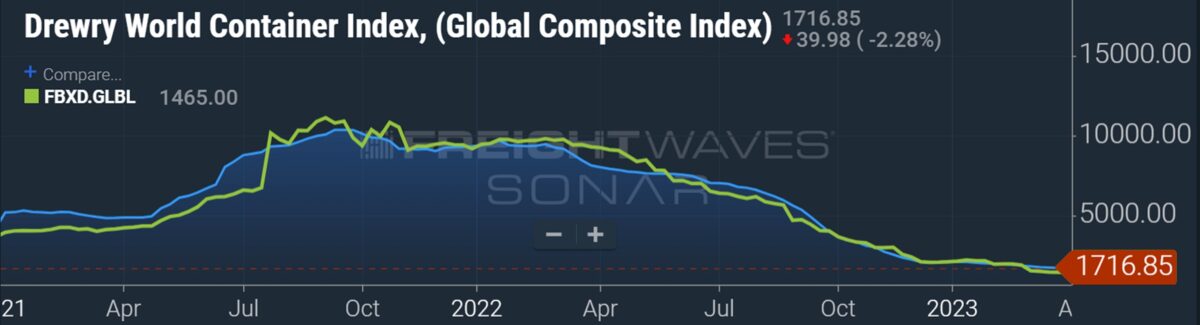

The Cosco revenue-per-FEU data underscores, yet again, the limitations of spot container freight indexes.

Spot indexes are good at showing the future direction the broader market is heading, not what carriers actually earn per FEU. The Cosco global revenue-per-FEU curve bears little resemblance to global spot index curves. The spot indexes fell earlier and by a much greater degree.

The majority of Cosco’s volumes are in the intra-China and intra-Asia markets, which are not covered by most global indexes. Furthermore, the majority of volume carried in the lanes that are covered by indexes are moved under annual contracts, and annual contract rates have significantly exceeded spot rates over the past year.

According to McCown, spot rates “have an impact on negotiations related to renewing contracts that move the large majority of loads. It is in that more indirect role where spot rate indices have their largest impact in container shipping. They are not an accurate measure of either the level or trend in actual container pricing.”

Click for more articles by Greg Miller

Related articles:

- How much will container lines ‘earn’ in 2023? It depends on the metric

- Zim Q4 results surprise to upside but 2023 ‘extremely challenging’

- Container shipping market yet to bottom as spot rates keep slipping

- ‘Colossal’ tidal wave of new container ships about to strike

- Container lines still chartering ships despite drop in cargo demand

- Container trade’s next turn: Price wars, cheap contracts, new ships

- Maersk: Container shipping contract rates will sink to spot levels