One of the earlier scenarios for container shipping’s 2023 peak season went like this: Importers would get cocky and keep much of their business in the spot market. Shipping lines would heavily curtail trans-Pacific transport capacity. America’s inventory overhang would evaporate just as holiday imports ramped up. Spot rates would jump — just as they did in 2020’s peak season after COVID lockdowns — and importers without sufficient contract coverage would get caught out.

No one’s really talking about that one anymore.

Inventory destocking has gone on longer than expected. Pressures on consumer demand are building. Trans-Pacific shipping capacity is not down as much as predicted. Spot rates bumped up in mid-April but have eased since and remain extremely weak.

The talk now is more about a moderate peak season at best, roughly in line with pre-COVID levels, with no fireworks.

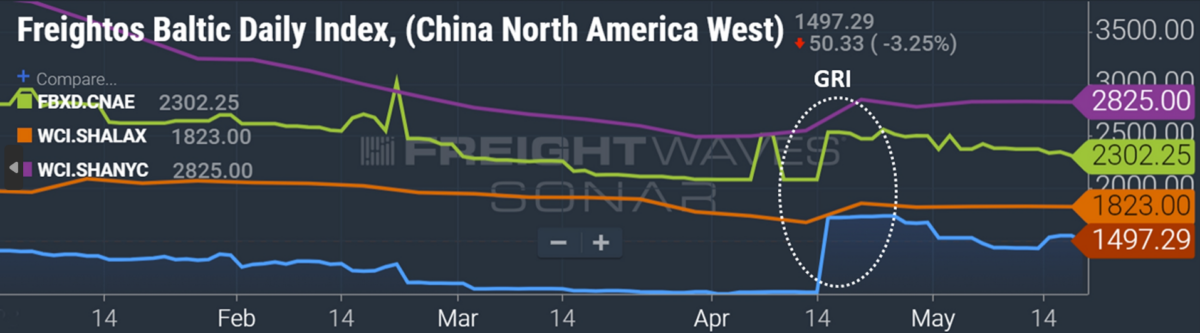

Spot rates still extremely weak

Container lines implemented a general rate increase (GRI) in mid-April that was at least partially successful, finally clawing rates off the floor. However, they reportedly delayed planned GRIs in early May and mid-May, and are now looking at GRIs in June.

Spot rate indexes show mid-April gains have partially stuck but rates have edged backward more recently. “Rate gains seen in April have been slipping gradually,” said Jefferies shipping analyst Omar Nokta in a research note Friday.

The Freightos Baltic Daily Index (FBX) for the China-West Coast lane was at $1,497 per forty-foot equivalent unit on Thursday. That’s up 48% from before the mid-April GRI but down 14% from April 25.

Drewry’s World Container Index (WCI) assessment for Shanghai-Los Angeles was at $1,823 per FEU for the week ending Thursday, up 9% from the week of April 13 but down 2% from the week of April 20.

The FBX China-East Coast index was at $2,302 per FEU on Thursday, up 10% from mid-April but down 10% from April 24. The WCI Shanghai-New York rate was at $2,825 per FEU, up 11% from the week of April 13 but down 1% from the week of April 20.

On the contract-rate front, pricing of new trans-Pacific annual agreements coming into force this month is sharply lower than for contracts signed the prior year.

Xeneta reported Wednesday that long-term contract rates on the Asia-West Coast route averaged $1,893 per FEU. That’s down 70% from the company’s assessment of average long-term rates on this route in late November, albeit 30% higher than Xeneta’s current average spot-rate assessment.

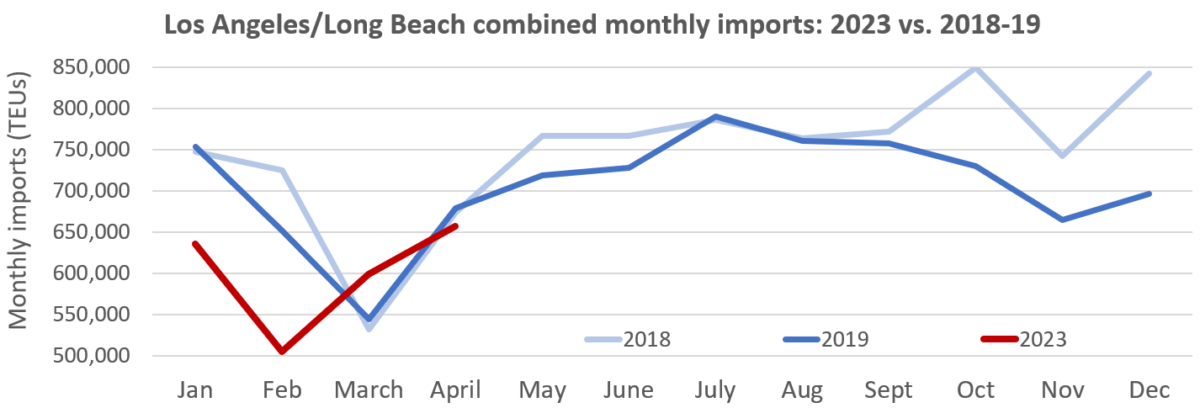

Retailer progress on inventory overhang

Ocean carriers Maersk and Hapag-Lloyd have predicted that trans-Pacific volumes will rise in the second half due to and end to inventory destocking, supporting higher rates.

They pointed out that import volumes are below U.S. consumption as inventories are drawn. When inventories wind down, imports will align better with consumption, increasing volumes. The problem with this thesis is that consumption could go down in the second half versus the first, offsetting sequential gains from a return to inventory restocking.

This issue was a central focus of analyst client notes this week following quarterly results of mega-retailers Home Depot (NYSE: HD), Target (NYSE: TGT) and Walmart (NYSE: WMT).

Home Depot’s Q1 2023 inventories were still up 60% in nominal terms versus Q1 2019, pre-COVID. But Deutsche Bank transport analyst Amit Mehrotra maintained that “the vast majority of this likely reflects inflation.” On the consumption side, he pointed out that Home Depot “unit demand is already back to pre-pandemic levels” when adjusted for inflation.

Target’s inventories were down 16% year on year and up 30% versus Q1 2019, “implying unit inventory is about flat versus 2019 when adjusting for inflation,” said Mehrotra.

Evercore ISI retail analyst Greg Melich noted that Target’s sales growth since Q1 2019 exceeded its inventory growth, “suggesting that Target’s [inventory] overbuilding woes are behind them.”

Walmart President John Furner said on Thursday’s conference call: “Q1 last year would have been the peak of inventories. We worked through a backlog of something like 100,000 containers that had been delayed at ports. So, lapping those costs gets bigger as you look forward to the next quarter or so. When you get into the back half of the year, things tend to normalize.”

Concerns grow on consumption

According to Mehrotra, “The bottom line is that based on demand today, we think inventory levels are back to normalized levels. But the risk is more broad-based demand destruction as consumers pull back. Home Depot’s results clearly showcased demand destruction in the space that the company focuses on — home improvement.”

Mehrotra also noted that retail sales are still above where the pre-pandemic trend line would place them, meaning sales have further to fall as they normalize.

“U.S. retail sales ex-auto and gasoline were on a very consistent trend prior to the pandemic,” he wrote Friday. Extrapolating that trend suggests April retail sales excluding automotive and gasoline sales were 15% higher than the historical trend line on a nominal basis and 5% higher on an inflation-adjusted basis, he explained.

“This implies that monthly retail sales need to decline by 5% to normalize to the pre-COVID trend. Said another way, the large spread between where we are today and the trend is mostly explained by inflation, with one-third explained by a pull-forward in spending: 5% is due to pull-forward, 10% due to inflation.”

According to Jon Chappell, transport analyst at Evercore ISI, “Destocking has been a massive headwind to freight demand over the last year-plus and the near completion of this punitive process provides some credibility to the bottoming thesis.”

However, he warned that “the demand side and what retailers are solving for when contemplating ‘right-sized’ inventories is also a moving target, and is likely much lower — when looking at the upcoming peak season — than many would have expected at the start of the year.”

“So, progress for sure on the backward-looking inventory front, but still a lot of uncertainty left to play out as retailers must consider the pace of restocking in the immediate future,” said Chappell.

When could Christmas goods buoy imports?

The holiday goods trade is yet another peak-season variable.

Many of the holiday cargoes were already in the bookings pipeline at this time in 2022. This year, they’re being shipped later, which should theoretically provide some support to second-half volumes.

During a press conference in October 2022, Port of Los Angeles Executive Director Gene Seroka said: “September is traditionally a high-volume month for end-of-year products. Think toys and games, clothing, footwear and other products. Those holiday gift items dropped precipitously compared to [September 2021], mainly because they came in earlier. Our peak season was in June and July as importers moved up the arrival of these goods to bring some certainty to when they could get to market.”

The early peak season in 2022 was driven by fears of delivery delays due to port congestion and potential West Coast port labor unrest. Carrier schedules are not fully back to normal yet but there are no port queues this year. And importers have already switched supply chains to the East and Gulf coast ports to avoid the labor risk. Thus, there’s no need to rush holiday-goods imports.

Seroka said during a conference call Thursday that this year’s peak season will come later — and could be abbreviated.

“My estimation on peak season based on purchase orders that have already gone out and discussions with retailers, manufacturers and automotive companies is that we’ll probably see a relatively short peak season between the months of September and October,” said Seroka.

“That may start a little bit earlier for folks who want to ensure in-store and D.C. [distribution center] dates and it may run a little bit later into November if folks are trying to get that last-minute cargo through.”

Alan McCorkle, CEO of the Los Angeles’ Yusen Terminals, said during the same press conference: “What we’re hearing from our customer base is that … we will see a little bit more of a traditional peak. As we get into later in the summer months and into the fall, we’ll start to see volume pick back up to resupply for the holiday season.”

Click for more articles by Greg Miller

Related articles:

- Shipping boom hangover: When measuring markets gets tricky

- US imports up again in April as market mirrors pre-COVID ‘normal’

- 2nd-half freight rebound increasingly unlikely

- Hapag-Lloyd: Higher costs will inevitably push up shipping rates

- Maersk: Downturn on predicted course, liners acting ‘rationally’

- Container shipping warning: Green shoots are ‘transitory illusion’

- As Asia-US shipping rates rise, so does skepticism on staying power

- Mixed signals: Container shipping downturn not following the script