CPG companies expect continued inflation on transportation costs this year. While there are plenty of signs on the horizon that suggest that a freight recession may be forthcoming, 2022 freight costs for most CPG companies are expected to be higher than they were in 2021. Procter & Gamble and Mondelez are among the major CPG companies that have warned analysts of higher freight costs on their earnings calls the past two weeks.

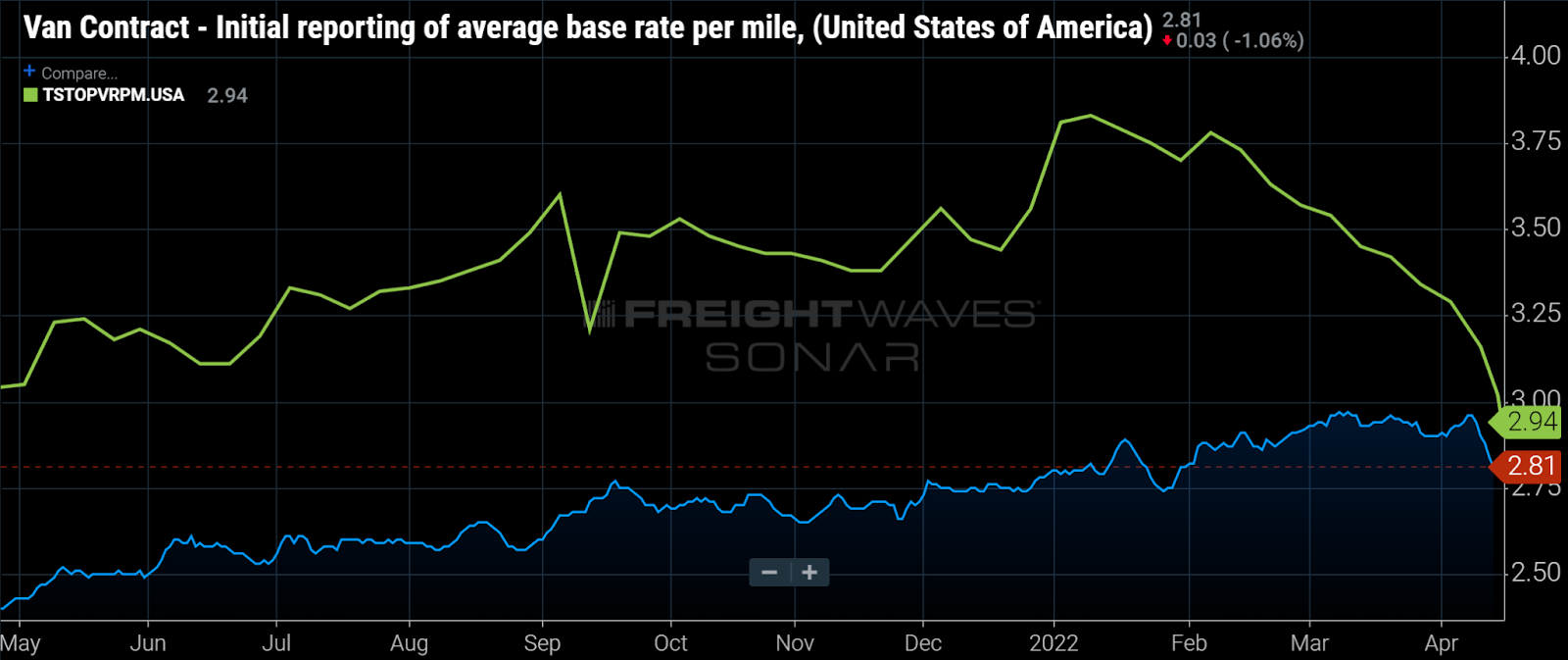

The SONAR chart below is an illustration of why a loosening freight market will not be immediately felt in CPG companies’ financials. CPGs are large-volume shippers with relatively consistent freight and primarily participate in the contract market. It takes time for contract rates, which are often annual contracts, to adjust downward to changing market conditions. Contract rates rose steadily throughout last year and, currently, contract freight rates remain well above where they were last year at this time. The SONAR chart below shows average dry van freight rates 39 cents a mile above this time last year, not including fuel surcharges.

Spot and contract freight rates are now close to parity. The CPG companies most likely to experience a year-over-year reduction in freight costs are those that were forced to move a significant number of loads on the spot market. Clorox is one such example; in recent quarters, the cleaning supplies maker had difficulty getting loads covered and paid exorbitant spot rates (well above averages in SONAR) to get loads moved. In recent weeks, carriers have become more compliant with contracts and the associated financial risk of having to move spot loads has fallen. Also, the change in spot rates tends to be a leading indicator for the change in contract rates. So while contract rates are still being repriced above year-ago levels, the trajectory of contract rates this year is likely to be downward.

The Indonesian government’s protectionism is rippling through vegetable oil markets, which are major CPG ingredients. After announcing in January that 20% of Indonesian palm oil would be reserved for domestic consumption and withdrawing that protection in March, the Indonesian government announced new restrictions on palm oil exports the past several days. The government has gone back and forth on whether the bans would cover all palm oil or only refined palm oil. The latest, according to Food Dive, is that the ban on exports will include both crude and refined palm oil.

Vegetable oils have been among the most inflationary ingredients in CPG items this year. After today’s surge, palm oil futures have risen about 55% year-to-date and are up about 95% from the year-ago level. Other vegetable oils, such as soybean oil and canola oil, serve as substitutes and the added protectionism is similarly impacting the market for those edible oils. The label on Oreos is a good illustration of this: One of the first ingredients listed is palm oil and/or canola oil.

Palm oil goes into a wide range of CPG items including edible items such as ice cream and confectionary items as well as non-edible items, such as detergents and cosmetics. Mondelez, Nestle and Unilever are all major consumers of palm oil. According to snack maker Mondelez, it represents approximately 0.5% of global demand for palm oil.

Food Processing described how Nestle is adjusting production in Ukraine to keep plants running. The makeshift operational procedures include:

- Converting below-ground space in plants to bomb shelters.

- Reducing staffing levels to fit into the sheltered spaces within plants.

- Adding flexibility to production schedules for more frequent starts and stops.

- Sourcing ingredients from abroad that were formerly sourced locally.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, please click here.