“Yea, though I walk through the valley of the shadow of death, I will fear no evil …” begins a psalm that might comfort today’s crude-tanker investors.

Crude tankers have been condemned to an extended stay in “spot-rate hell,” lamented Stifel analyst Ben Nolan in his latest quarterly outlook. He wrote that the sector is only at the “halfway point in the very long road through the Valley of Death.” Nolan quoted Winston’s Churchill’s advice: “If you are going through hell, keep going.”

Clarksons Platou Securities estimated that very large crude carriers (VLCCs, tankers that carry 2 million barrels of crude) were earning a mere $4,100 per day on Friday. At those rates, VLCC owners bleed cash. They can’t even cover a voyage’s operating expenses.

On Feb. 1, Saudi Arabia began a voluntary two-month production cut of 1 million barrels per day to bolster OPEC+ cuts. Saudi Arabia’s surprise decision was yet another lashing for crude tankers on top of demand pain from COVID restrictions.

“There is no way to sugarcoat this. Especially as lockdowns have become more — not less — aggressive,” acknowledged Brian Gallagher, head of investor relations for Euronav (NYSE: EURN), during a quarterly call with analysts on Thursday. “We need consumption of crude to return to normalized levels and news on that front continues to disappoint.”

Floating storage finally unwinding

But there’s at least some glimmers of hope amid the infernal metaphors.

Crude-tanker stocks have traded up over recent days. Brent crude has just topped $60 a barrel, the highest price since before the pandemic. And floating storage — a major barrier to the crude-tanker rate recovery — is unwinding at a faster past than many market-watchers may realize.

Last March, the production-cut deal between Saudi Arabia and Russia broke down, spurring Saudi Arabia to open its spigots. At the same time, other countries could not pull back production fast enough to align with plunging oil demand due to COVID lockdowns. All of that extra crude had to go somewhere. A lot of it ended in floating storage aboard tankers.

Until those stored cargoes are unloaded, crude transport demand will be reduced, because cargoes are already waiting offshore of destinations. Furthermore, each tanker that unloads a storage cargo goes back into the spot market. That creates more competition, a negative for rates.

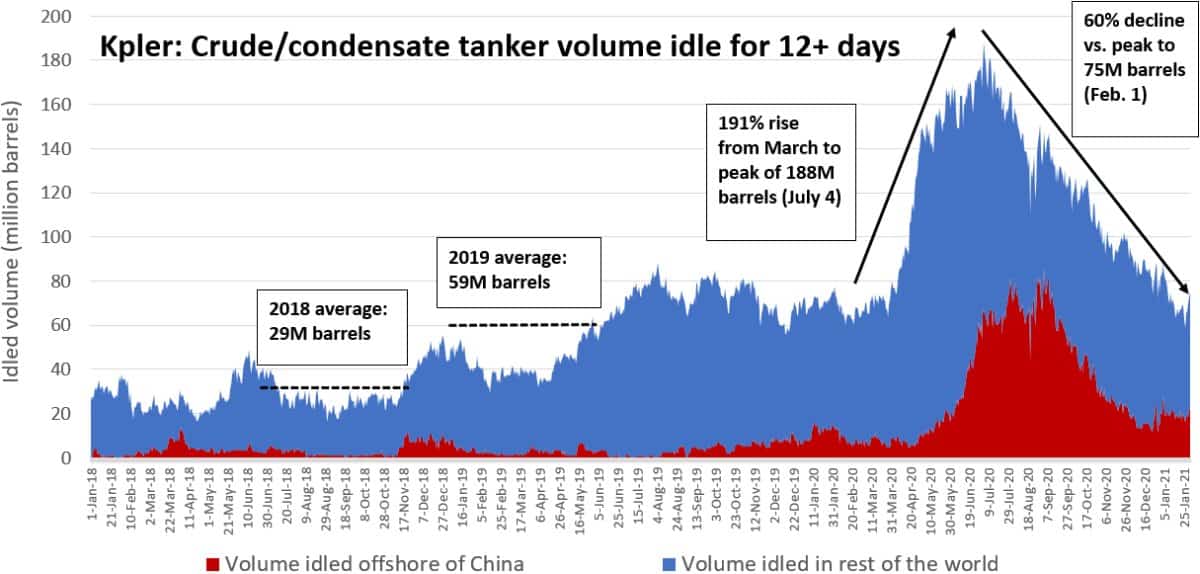

Floating storage lingers off China

Commodities analytics company Kpler provided American Shipper with its latest data on floating storage. Kpler tracks the cargo capacity of laden crude and condensate tankers that have been stationary for 12 or more days. The data covers floating storage as well as congestion delays caused by weather and other factors.

The Kpler data reveals that laden, idled crude-tanker capacity totaled 75 million barrels (37.5 VLCC equivalents) as of Feb. 1. That’s down sharply from the 188 million barrels at the peak on July 4. Idled capacity has been hovering around 65-75 million barrels since mid-January. It hit a recent low of 59 million barrels on Jan. 27.

To put that in context, the full-year average for this Kpler dataset in 2019 — before COVID and the OPEC+ production-agreement breakdown — was 59 million barrels daily. The 2018 average was considerably lower, at 29 million barrels daily. But the 2019 increase was largely driven by Iranian sanctions, and those sanctions remain in place.

“Slowly but surely things are moving back towards normality,” affirmed Reid l’Anson, senior commodity economist at Kpler.

The biggest remaining overhang is idled tankers offshore of China. That capacity totaled 22 million barrels as of Feb. 1, still far above last year’s daily average of 3 million barrels.

Timing the recovery

How long will the dark walk through the valley last for crude-tanker owners and stock investors? The consensus is: at least for the first half — and maybe longer.

According to Gallagher, “A return to normal activity in our lives has been constantly deferred. It looks like [oil] consumption will only return to 2019 peak levels in 2022.”

Euronav CEO Hugo De Stoop said that weak rates “will most likely continue into the second half of 2021, at least.” Underscoring how far away the recovery might be, he cited possible upside in the winter 2021-2022 season.

Evercore ISI analyst Jon Chappell wrote in his latest quarterly outlook, “It is always darkest before the dawn, but the question is: How long until the sun rises? Is it 5 a.m. in New York City in June or is it midnight in Oslo in December? To us, the fundamental view feels more like the latter.”

Chappell believes it is “too early to buy tanker stocks, but too late to sell.” (His one exception on the “sell” side is Nordic American Tankers [NYSE: NAT], which he calls “our top ‘short’ idea.”)

Chappell sees VLCCs averaging only $14,000 per day in the first quarter, rising to $28,000 per day in the fourth, with the full year averaging $21,000 per day.

Jefferies analyst Randy Giveans is likewise bearish on the first half, but much more bullish on the second half than Chappell. He projects VLCC rates averaging $13,000 per day in the first quarter, rising to $47,000 per day in the fourth, and averaging $30,000 per day for the year as a whole.

Tanker results roundup

On Monday, VLCC owner DHT (NYSE: DHT) reported net income of $7.6 million for Q4 2020 compared to net income of $75.9 million in Q4 2019. Adjusted earnings per share of 8 cents came in below the consensus forecast for a gain of 12 cents per share.

DHT’s spot-trading VLCCs earned $19,200 per day in the latest quarter, down 68% year-on-year. But the company was much less exposed to spot weakness than in the past: DHT’s spot exposure was only 39.3% in Q4 2020 — half the 81.5% exposure the year before.

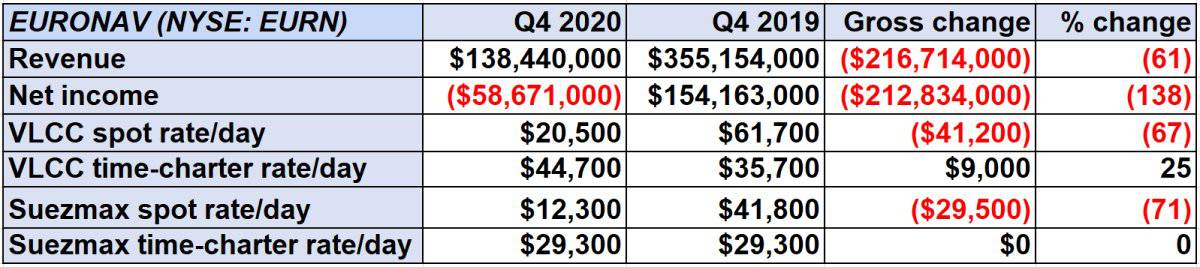

On Thursday, Euronav reported a net loss of $58.7 million for Q4 2020 versus net income of $154.2 million in Q4 2019. Its loss of 29 cents per share was steeper than the consensus forecast for a loss of 22 cents per share.

Euronav’s VLCCs in the spot market earned $20,500 per day during Q4 2020, down 67% year-on-year. The company’s spot Suezmaxes (tankers that carry 1 million barrels of crude) earned $12,300 per day, down 71% year-on-year.

Euronav has 46% of its available VLCC spot days for Q1 2021 fixed at $16,396 per day and 54% of spot Suezmax days fixed at $9,207 per day.

With rates this low, analysts’ focus is on strong balance sheets that will allow owners to survive and buy assets countercyclically — not Q4 2019 results. As Chappell put it, “Can we just skip this earnings season?” Click for more FreightWaves/American Shipper articles by Greg Miller

MORE ON TANKERS: Tanker recovery still distant prospect after Saudi surprise: see story here. Frontline’s disappearing dividend speaks volumes on tanker fears: see story here. Tanker shipping at risk of rare winter hibernation: see story here.