CSX beats estimates as coal volumes post strong gains, but increasing share in intermodal is the railroad’s next plan.

CSX Corporation (Nasdaq: CSX) reported third quarter earnings above Wall Street consensus estimates thanks to its ongoing implementation of precision scheduled railroading and a strong market for U.S. export coal.

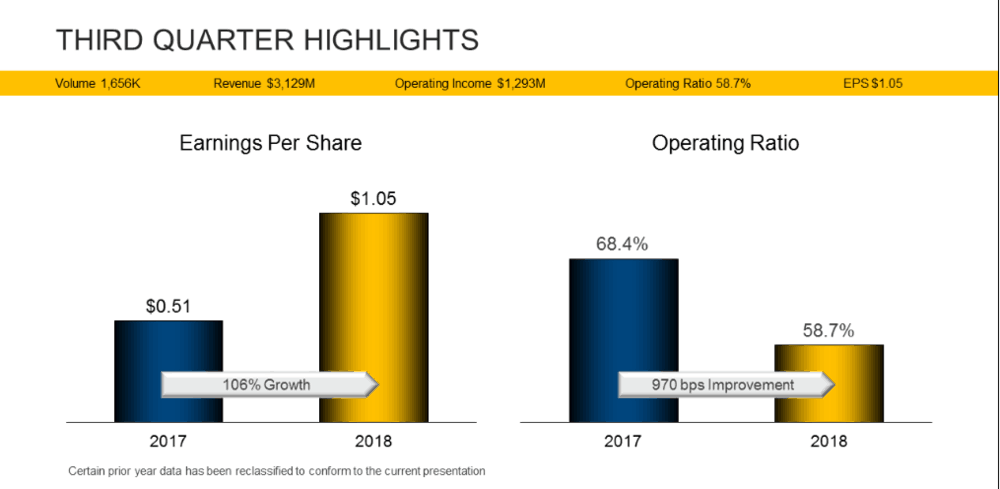

The third quarter marks the second consecutive that saw CSX’s operating ratio fall below 60%, with those results coming in two years ahead of the schedule set by chief executive James Foote.

“I am very excited by the strong performance of the railroad,” Foote said on the earning conference call. “Two words sum up everything: great performance.”

The Jacksonville, Fla.-based company reported net income of $894 million, nearly double last year’s net income of $459 million. Earnings per share of $1.05 beat the consensus sell-side estimate of $0.95 per share.

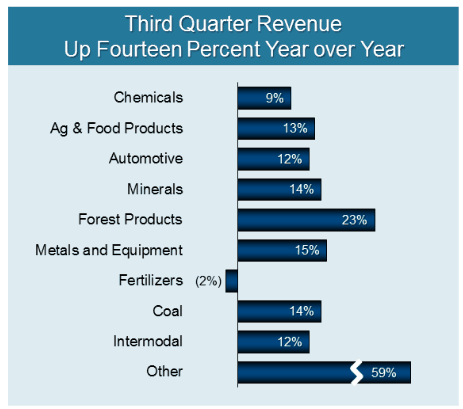

Revenue for the third quarter increased 14% year-on-year to $3.13 billion.

CSX saw volume increases in the mid-single digit percentage across almost all freight classes, with total volumes up 4% for the period to 1.656 million carloads during the quarter.

But better pricing and a more favorable freight mix led to double-digit percentage increases in revenue across freight categories with merchandise revenue up 12% to $1.89 billion, coal up 14% to $588 million and intermodal up 12% to $500 million.

Foote says most of the coal cargoes were for export markets, which have been showing strength this year. In the second quarter, U.S. coal exports hit a five-year high of 30.9 million tons. Low coal stockpiles at U.S. utilities may keep the volumes strong during the current quarter.

“Clearly, the strength of export coal helped our results,” Foote said. “But all groups are doing well.”

CSX’s operating ratio narrowed to 58.7%, 970 basis points better than last year’s levels.

Expenses were down 2% to $1.84 billion, as increased volume and higher fuel prices were offset by efficiency gains from implement scheduled railroading.

By most measures, CSX saw year-on-year improvements in operating statistics, with train velocity increasing and dwell decreasing. Railcars online also trended down even as volumes increased, Foote says.

Revenue ton-miles for coal and merchandise were up 10% and 8% during the quarter. Foote pointed to the data as evidence that “customers are moving more freight back to railroad.”

Intermodal saw revenue ton-miles grow only 1% for the quarter. But Foote says CSX’s intermodal service offering will gain thanks to new projects.

Those projects include the Northwest Ohio Intermodal Terminal, which will be expanded with a new logistics park to handle additional volume from the east coast. Foote says the company has had to rejigger the hub-and-spoke system that existed at the terminal, which resulted in “double and triple handling” of the same container on the network.

Foote also says the haulage agreement with BNSF which will allow intermodal service out of BNSF’s west coast terminals to the Northwest Ohio Intermodal Terminal will add volumes to the CSX network.

“The (BNSF haulage volumes) will offset some of the lane rationalizations,” Foote said. “Haulage is an effective way for us to work together in the Northwest Ohio market.”

Foote says the improved intermodal service offering will more freight to railroads as CSX aims to “win back share from customers that moved to truck last year.”