Flatbed truckload company Daseke (NASDAQ: DSKE) saw trends moderate in the fourth quarter compared to a third-quarter blowout, which benefited from an increase in highly profitable project freight. Management cautioned investors on the third-quarter call that a fourth-quarter repeat was unlikely.

On Friday, the Addison, Texas-based company reported fourth-quarter adjusted earnings per share of 12 cents, excluding the divestiture of its energy business Aveda, which was better than the consensus expectation of 4-cent loss and last year’s 6-cent result.

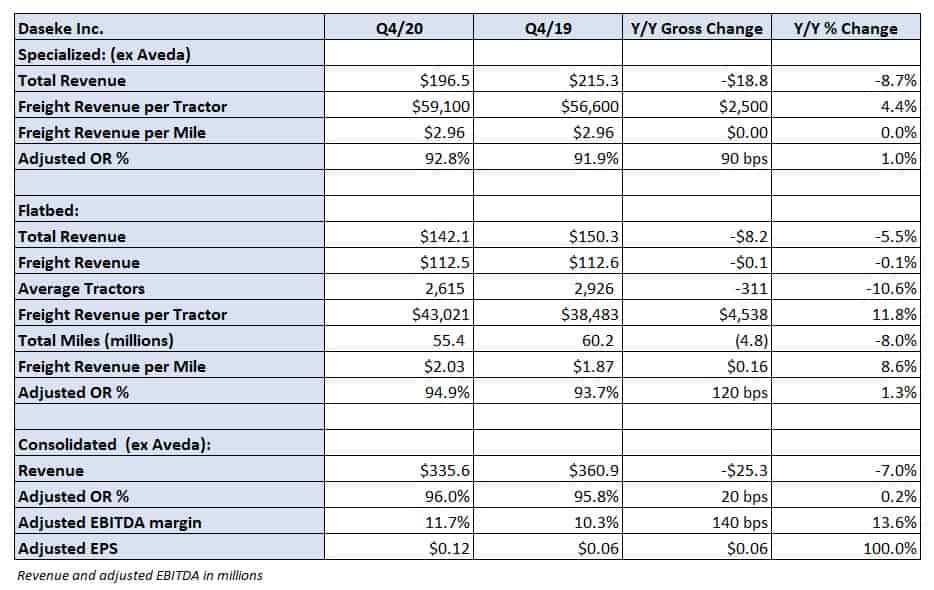

However, the quarter appears to be evidence that the companywide restructuring won’t be linear. Revenue dipped on a year-over-year comparison with operating ratios sliding modestly as well. The company’s 2021 guidance was mixed.

2020 was a big year for Daseke. The company’s turnaround initiatives led to a full-year adjusted OR of 93.6%, excluding Aveda, 280 basis points better year-over-year. Adjusted earnings before interest, taxes, depreciation and amortization increased 15% to $179 million, free cash flow generated was $169 million and net debt was reduced by $105 million.

“2020 was a highly successful and transformational year for Daseke. We streamlined the business, built a high-performing executive team and supporting organization and demonstrated the resilience and diversity of our business by delivering strong profitability and free cash flow despite the challenging economic backdrop,” said Interim CEO Jonathan Shepko.

Daseke reported a 7% year-over-year decline in consolidated revenue to $336 million, excluding the divestiture. Timing of the project freight and the overhang of COVID on the industrial economy were the culprits.

Revenue in the company’s specialized freight segment was 9% lower, excluding Aveda, but revenue per tractor was up 4.4% on a flat rate per mile. The OR deteriorated 90 bps to 92.8% on increased insurance costs, which were partially offset by the turnaround initiatives.

The flatbed segment experienced similar fundamentals, which led to a 5% year-over-year reduction in revenue as the average tractor count declined 11%. Rate per mile was up 9% and revenue per tractor climbed 12%. The division’s OR backed up 120 bps to 94.9%.

The company expects full-year 2021 revenue to range between $1.4 billion and $1.5 billion, which brackets the $1.47 billion consensus estimate. Adjusted EBITDA is forecast to be in a range of $165 million to $175 million, slightly worse year-over-year.

“Rates remain strong to start the year, and we are seeing pockets of strength throughout our industrial customer base that were previously pressured by the pandemic. As a result, we will look to optimize our improved platform and prepare the business to pivot to growth as pandemic conditions dissipate,” said Daseke CFO Jason Bates.

Daseke will host a conference call at 11 a.m. Friday to discuss results with analysts. Stay tuned to FreightWaves for more coverage on Daseke’s earnings report.

Shares of DSKE are up slightly in early trading Friday compared to the S&P 500, which is off nearly 1%.