Numerous companies, including CPG companies, at FreightWaves’ The Future of Supply Chain conference last week highlighted the difficulty of accurately forecasting. We heard that sentiment expressed from numerous companies, including transportation companies and intermediaries as well as CPG companies and other shippers. Basically, market forecasts are almost always too reflective of current market conditions without fully incorporating upcoming changes in market conditions. For example, in a tightening freight market, forecasts are rarely bullish enough (from carriers’ perspective) and forecasts are rarely bearish enough (again, from carriers’ perspective) when conditions start to loosen.

For CPG companies, forecasting demand for consumer products has never been more challenging given the uncertainty created by changing work schedules (so far, working from home has kept CPG demand above pre-pandemic levels) and inflation (so far, elasticities for most CPG products have been below historical levels, but it’s not clear whether that trend will continue and will likely be mixed by product category).

Instead of relying on market forecasts, participants at last week’s conference are relying more heavily on reacting to the most up-to-the-date data points and being flexible enough to react to those data points quickly. Nestle gave the example that the “first mile” of transportation from the factory is key to having products in stock. With data in real time, CPGs can make routing decisions closer to the time of consumption and reduce stockouts without the need for higher inventory levels.

For CPG companies, automation is not just for reducing labor costs and preventing labor disruptions. Numerous companies at The Future of Supply Chain, including Tyson, discussed how automation is enabling companies to learn from their own data and leading to improved real-time data flow. The result is improved supply chain efficiency and lower inventory levels. Still, the benefit of automation on costs should not be understated, especially in the CPG industry. During the pandemic, the CPG industry experienced severe COVID outbreaks at meat packing plants, strikes at Mondelez and Kellogg and shortages of workers.

Unilever highlighted supply chain efficiency as a major source of synergies in its acquisition strategy. Unilever has acquired a steady stream of smaller consumer goods companies; Dollar Shave Club and Liquid IV are just two examples amid a laundry list of deals. According to Unilever, as startup CPG companies scale up, their supply chain and distribution can no longer be “managed on an Excel spreadsheet” and the capabilities of being aligned with the CPG giant enables for an efficient transition to true nationwide distribution. I had been thinking about Unilever’s acquisition strategy differently — that it was all about finding avenues for revenue growth in products and demographics that are outpacing broad industrywide growth rates. Of course, acquisitions in the CPG industry present their own set of challenges, including the need to not alienate the target company’s early supporters.

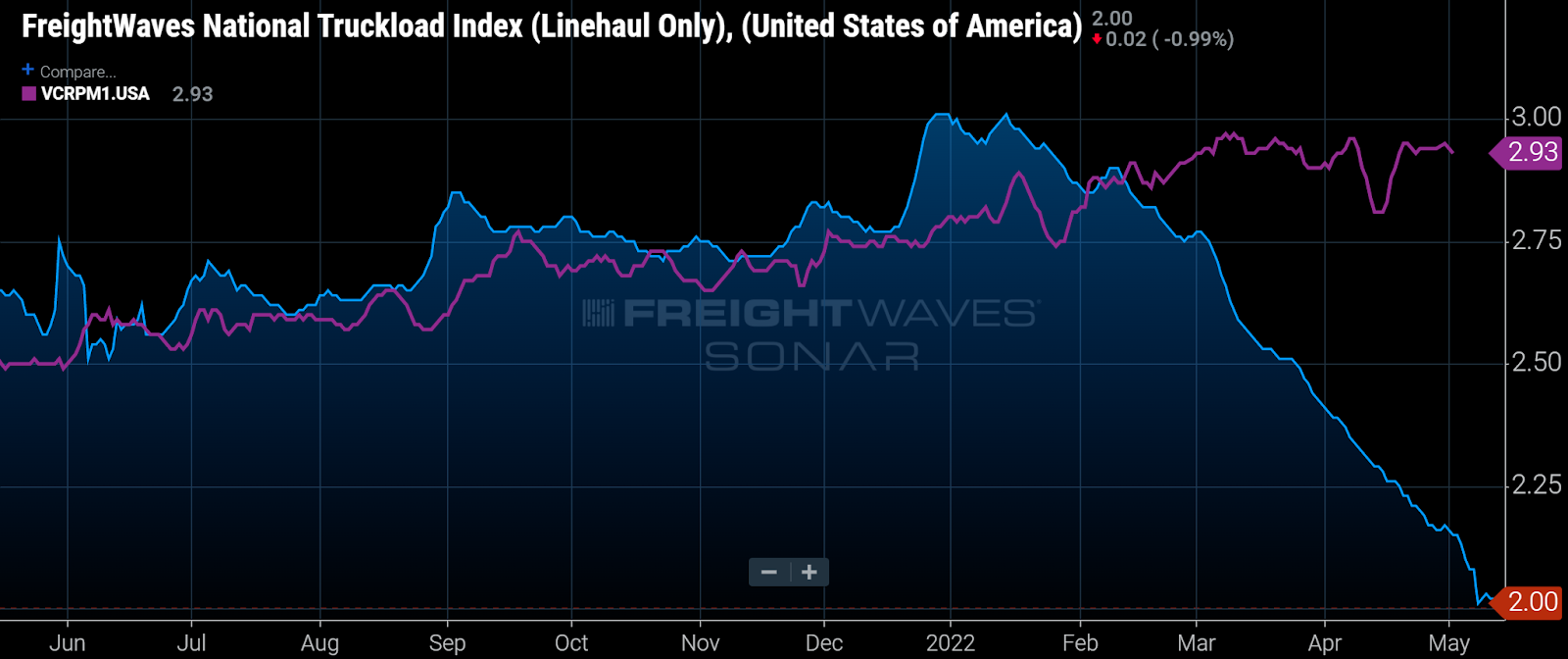

The newly established FreightWaves National Truckload Index (NTI) shows that spot rates are well below contract rates. The NTI is a composite of spot rates provided to us by a consortium of brokers and intermediaries; the rates represent what brokers pay for on-demand capacity.

SONAR: The nationwide average dry van spot rate and dry van contract rate is shown in blue and purple, respectively. Both datasets exclude fuel surcharges.

The above chart gets to one of the key questions in freight transportation right now: How long will it be before contractual shippers, after seeing spot rates fall well below contract rates, get more aggressive and rebid their freight or otherwise push for freight rate relief? At FreightWaves, our perception is that a meaningful spread between contract and spot rates, such as the one shown above, is likely to persist until shippers gain confidence that a looser freight market is here to stay. At that point, we will likely see shippers look to renegotiate contracts and move annual contractual commitments to quarterly or weekly mini-bids. We have heard anecdotes suggesting that food shippers in particular are waiting to see how produce season develops before adjusting contact rates. I plan to keep The Stockout readers updated on this issue.

Finally, congrats to the CPGs winning a FreightWaves Shipper of Choice award. Winners in the CPG space were Kellogg’s, Coca-Cola, Tyson, Pepsico, Boston Beer, Campbell’s, McCormick, Procter & Gamble, Kimberly-Clark, Kraft Heinz, Nestle, J.M. Smucker Company, and Unilever.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, please click here.