As first-quarter earnings are set to begin next week when J.B. Hunt Transport Services (NASDAQ: JBHT) reports on Tuesday, some onlookers are interested to see if the COVID-19-related volume surge provided the lift needed to save what could have been a slightly worse-than-expected quarter for truckload (TL) and less-than-truckload (LTL) carriers.

That said, first-quarter results aren’t likely to matter much as all observers will be more focused on what management teams have to say about a post-surge environment, potential green shoots, and when and what a recovery will look like.

Unfortunately, it’s likely just too early for any company to call its shot for the rest of the year as the virus curve has yet to peak and plateau in most regions across the nation. Further, any company with official earnings guidance will likely suspend it, a move that has been commonplace among the airlines and truck original equipment manufacturers (OEMs) and their suppliers.

First quarter likely decent for trucking companies

In a Wednesday note to clients, Morgan Stanley (NYSE: MS) transportation equity research analyst Ravi Shanker said that while first-quarter results “may be better than expected,” they will be “irrelevant as investors look ahead to a 3Q rebound (once we make it past the historic 2Q trough).” In the note, he informed investors that he was pulling up his first-quarter 2020 forecasts from recently lowered levels for most of the TL and LTL carriers he covers.

“We expect [management] to provide little by way of a forward outlook given unprecedented uncertainty,” Shanker continued.

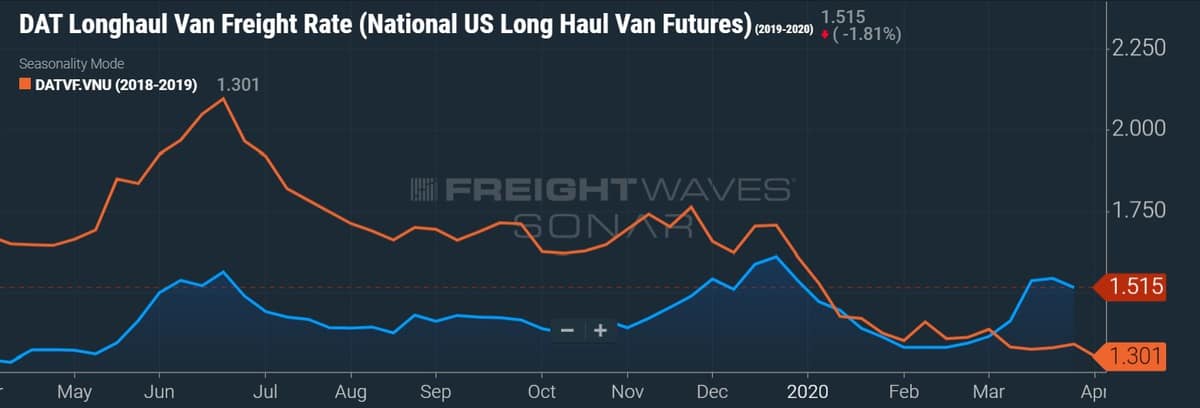

2020 began with the expectation that truck capacity would continue to exit the market, allowing rates to climb higher. An additional catalyst for improved rates could come in the form of a positive inflection in volumes at some point in the year. However, many analysts didn’t believe that this was a requirement given the rate of the capacity exodus.

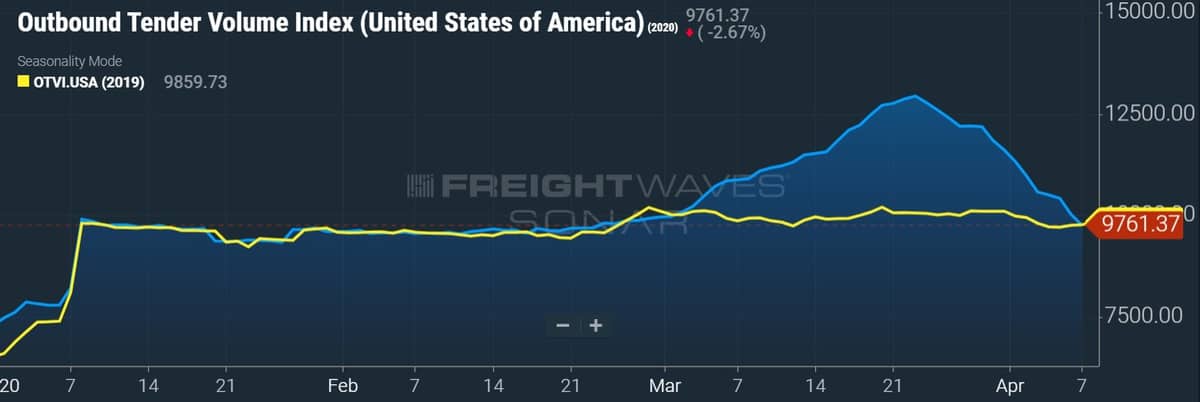

The first two months of the year were largely as scripted, with sluggish volumes and subdued but hopeful commentary from the carriers. The forward-looking expectation for rate improvement was still intact. While the outbreak worsened abroad in late February, sending equity markets lower, volumes remained largely level with 2019.

However, as many states invoked shelter-in-place and self-quarantine ordinances, volumes surged. Year-over-year outperformance occurred from early March to early April, with FreightWaves’ Outbound Tender Volume Index peaking roughly 30% higher during the height of the surge. Some analysts believe that this was the bump needed to take a fairly normal, in-line type of quarter to something that may be better than previously expected, at least for trucking companies.

But first-quarter results are unlikely to matter. As households have built up inventory for necessities like groceries, cleaning supplies and other consumer staples, carriers are faced with even more uncertainty of how to plan for and what the next leg of this cycle may be. The severity of a potential freight falloff is still unknown, especially as many small to medium-size businesses remain under a forced closure.

Shanker believes that any commentary around April trends will be more relevant and helpful in determining “which companies may be dealing with the 2Q cliff better than others.”

While interested parties await direction into the shape of the recovery curve — “V,” “U” or “L” — Shanker expects an “extended recovery for the overall macro” but believes the transportation sector could see a “quicker V-shaped recovery” as supply chain restocking will continue.

Further, there has been conjecture around the industry that many supply chains ran on thin inventory, relying on tech-enabled precision to meet just-in-time delivery requirements of goods. This approach may be altered somewhat given the recent shock to supply chains, possibly prompting some managers to rethink their approach to inventory. This theory could also be bolstered by interest rates that are hovering around zero, leading to lower inventory carrying costs. Even modest adjustments to inventory policy would be a positive for carriers.

In the piece, Shanker largely fine-tuned his estimates for 2020, taking some higher and some lower for the asset-based carriers, logistics companies and railroads that he follows. He had previously made more meaningful changes in March, taking his TL forecasts down by high single digits.

On the TLs Shanker concluded, “trucking remains our preferred space in transports especially TLs given their defensive end-markets, high variable cost, clean balance sheet and ability to defer capex.”

Opinions diverge on brokerage

One battleground that has formed in the 2020 earnings debate is over the freight brokers. Most analysts agree that the first quarter will be a tough one for truck brokers, highlighted by margin compression as the market tightened during the quarter, spot rates rose and brokers were forced to pay up for truck capacity to fulfill load commitments already under contract.

Analysts’ opinions diverge from there. Some believe that the expected TL volume declines in the second quarter will relieve margin pressure as rates recede. Further, some are viewing easier year-over-year comparisons for companies like C.H. Robinson Worldwide (NASDAQ: CHRW) now that the company has likely roundtripped what has been an extremely tough operating environment for more than a year now.

Shanker sees the volume cliff as presenting more pain for the group as “numbers are likely to be pressured by a sharp decline in volumes against a cost structure that may not be as variable as the bulls think (given stable headcount and ongoing tech investments).” Further, he believes that shippers will “overwhelmingly [move] toward asset-based carriers vs. brokers to secure truck capacity” when the rebound unfolds. He also noted that the competition from “new digital entrants” remains a threat.

Uncertainty overhang

While the year of meaningful truck capacity contraction remains in play, how the pandemic plays out remains front and center.

Record truck additions during and after the 2018 peak were met with a sustained period of demand lower than what was required to support the industry’s new capacity. 2019 provided a year of lower rates and cost inflation on most lines of the carrier P&L, especially surging insurance expenses. Many carriers were forced to exit the market. These trends remain and in some cases have accelerated for those carriers not materially exposed to consumer packaged goods markets.

As first-quarter earnings season approaches, there are many questions. Most of them will likely go unanswered.