DryShips (NASDAQ: DRYS) – a public ship-owning company that’s either famous or infamous, depending on who you ask – has reported steady albeit slim profits and announced a major retrofitting program for its vessels.

The mixed-fleet owner, led by high-profile Greek magnate George Economou, reported net income of $1.5 million for the first quarter of 2019, up slightly from $1.2 million in the same period last year.

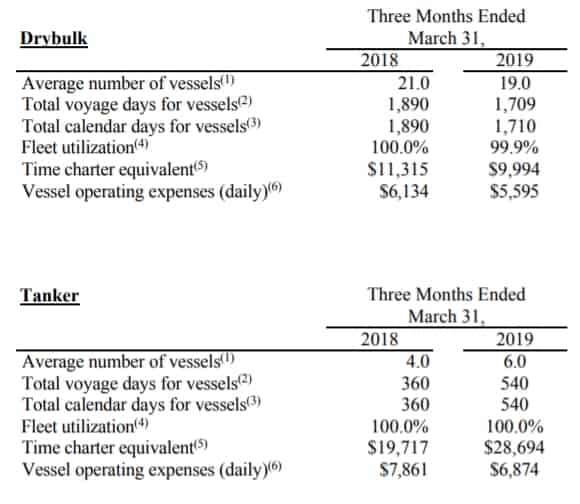

DryShips owns 31 vessels with a total carrying capacity of 3.5 million deadweight tons (DWT) – 19 dry bulk vessels totaling 2.5 million DWT, six tankers totaling 975,324 DWT, and six offshore-service vessels totaling 8,328 DWT.

The offshore-service vessels are laid up; the tankers are in the spot market; 11 of the 19 bulkers are in the spot market; and the remaining eight bulkers are on index-linked time charters, meaning they are also exposed to spot rates.

During the first quarter of 2019, DryShips’ bulkers achieved an average rate of $9,994 per day, down 12 percent year-on-year, while its tankers earned $28,694 per day, up 46 percent year-on-year.

When announcing its results after market close on May 15, DryShips revealed that it would spend $80-100 million in 2019-2020 and incur between 1,100 and 1,300 off-hire days to “future proof” its fleet by performing drydockings to install exhaust-gas scrubbers and ballast-water treatment systems.

DryShips and its founder Economou have long embodied one of the most controversial aspects of the public shipping community – public ship-owning entities controlled by private sponsors that do substantial related-party business with those sponsors. The public entity pays the private side fees for all technical and commercial management, and in many cases – particularly in the case of DryShips – it buys much of its fleet from the private related party.

Wells Fargo analyst Michael Webber puts out a periodic public shipping corporate governance scorecard. In Webber’s latest ranking of 56 companies, released on May 6, DryShips ranked 56th. It has been at or near the bottom since Webber began the series in 2016.

DryShips, a holding company with only a handful of employees, emerged as a poster child of high-flying shipping stocks during the shipping boom in the mid-2000s. DryShips went public in 2005 at $18 per share and by 2007, its stock was selling for over $120 – a surge that attracted a huge and dedicated following of retail investors and day traders.

The company’s stock collapsed in the wake of the 2009 financial crisis, after which it conducted a series of stock offerings that further diminished its share value. It was targeted by multiple lawsuits in that period, none of which prevailed.

DryShips diversified into tankers in 2010, buying newbuilding contracts that were linked to Economou, and when that plan didn’t work out, the company sold its tanker fleet in 2015 – back to Economou.

The chain of events that followed led some shipping insiders to privately express awe, prompted some investors to file lawsuits, and spurred the Securities & Exchange Commission (SEC) to launch an investigation.

Economou owned 18% of the company at the end of 2015, but almost no common shares by the end of 2016 (although he retained control through preferred voting shares). In late 2016, Economou bought almost all of the outstanding debt of DryShips at a steep discount – essentially becoming his own company’s banker and avoiding a potential default with the original lender.

In 2016-17, DryShips conducted a series of fund-raising deals with a Canadian group called Kalani Investments, grossing around $700 million. In several of these transactions, Kalani was given discounted shares by DryShips, which Kalani then sold to investors at a profit, a process that was fully disclosed in securities filings. The transactions were extremely dilutive to shareholders, wiping out almost all of the common stock value.

The proceeds were used by DryShips to buy ships, many of them from Economou. Economou then converted his debt in DryShips into equity, and solidified his shareholdings via a rights offering. As of today, Economou owns 83.4 percent of DryShips.

The company continues to be the target of lawsuits and investigations. Both DryShips and Kalani are defendants in an ongoing case in the U.S. Eastern District Court of New York that alleges securities fraud. DryShips asserted in its quarterly filing on March 15 that it “believes the complaint is without merit” and that it will “vigorously” defend itself.

It also reiterated that it had “received subpoenas from the SEC requesting certain documents and information in connection with offerings made by the company between June 2016 and August 2017” and that it is “providing the requested information and continues to respond from ongoing requests from the SEC.”