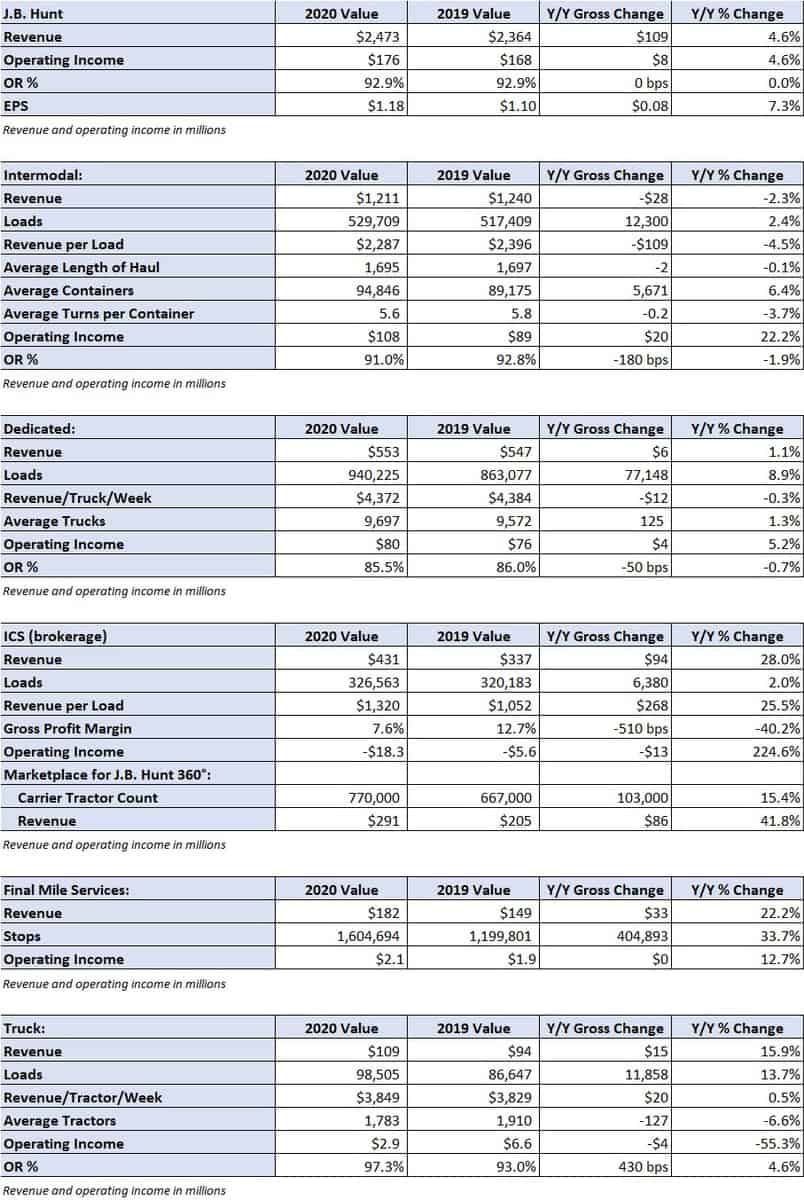

J.B. Hunt Transport Services (NASDAQ: JBHT) reported third-quarter earnings per share of $1.18, 9 cents below analysts’ expectations. The result was ahead of the 2019 third-quarter result of $1.10, but that period included $0.30 per share in arbitration charges related to the final award to BNSF Railway Company.

Total revenue of $2.47 billion was 5% higher year-over-year and ahead of the consensus estimate calling for revenue of $2.36 billion. The revenue increase was largely driven by a 25% increase in brokerage revenue per load, a 22% increase in final-mile revenue as total stops increased 34% and a 16% increase in the truck division as loads were up 14%. Total revenue, excluding fuel surcharges, climbed 9% compared to the 2019 period.

Operating income was also 5% higher year-over-year at $176 million, but down 17% year-over-year excluding the $44 million in charges related to the revenue-sharing dispute with BNSF. Higher purchased transportation costs on the railroads, widening losses in brokerage, increases in driver wages and recruiting expenses, higher third-party and drayage expenses, and increases in technology spending were listed as the culprits.

Shares of JBHT are down 6% in premarket trading.

The company will host a call at 10 a.m. EDT to discuss these results with analysts. Stay tuned to FreightWaves for continuing coverage of J.B. Hunt’s earnings results.