Before the market open on May 1, Atlas Air Worldwide Holdings (NASDAQ: AAWW) reported adjusted earnings of $0.98 per share, ahead of the fourth quarter 2018 and the NASDAQ consensus estimate of $0.86.

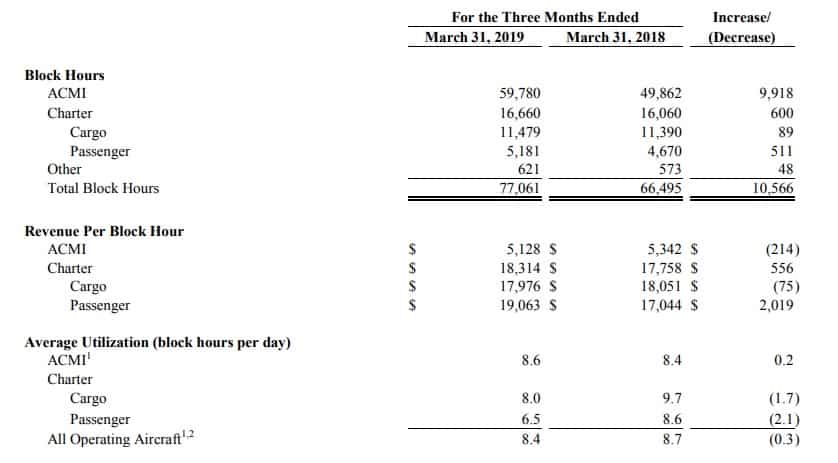

The global provider of outsourced aircraft and aviation operating services reported a year-over-year revenue increase of 15 percent to $679.7 million. Total volumes, or block hours, increased 16 percent year-over-year to 77,061.

Total direct contribution for all of AAWW’s segments increased 21 percent to $104.7 million. (AAWW uses the metric, “direct contribution,” which measures the income contribution from its separate units after allocation of direct ownership costs).

“Our first quarter results exceeded our expectations. We are benefitting from a full year of flying the 16 aircraft we added during 2018 for customers such as Amazon, Asiana Cargo, DHL Express, Inditex and SF Express, as well as the three aircraft for Nippon Cargo Airlines that we are adding this year,” said Atlas Air Worldwide President and Chief Executive Officer William J. Flynn.

Aircraft, Crew, Maintenance and Insurance (ACMI) reported a 15 percent increase in revenue as increases in volume were only partially offset by declines in revenue per block hour. Direct contribution was 2 percent lower year-over-year at $40 million even with increased volumes. Management cited higher crew costs, increased maintenance and repair costs and increased amortization costs as the reasons.

Revenue from the charter segment increased 7 percent as both volumes and rates improved. Higher block hours from military passenger and increased commercial cargo demand drove the increase. Direct contribution for this division was 15 percent lower at $29.1 million.

The dry leasing division (which provides aircraft and engine leasing solutions only) saw direct contribution more than triple to $35.5 million as revenue nearly doubled. The division benefitted from $17.9 million (after tax) in maintenance payments as 777 freighter service resumed in March 2019 and as additional aircraft placements occurred in the quarter.

Management provided an updated outlook for 2019 in the earnings press release, “Global economic activity and airfreight demand, supported by ongoing faster growth in express and e-commerce, are expected to continue to expand at a modest pace, while airfreight tonnage continues to grow from record levels. Looking ahead, we expect to generate higher volumes, revenue, adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) and adjusted net income in 2019.”

The company reiterated its full-year guidance calling for volumes to increase to approximately 340,000 block hours, revenue of approximately $3 billion, adjusted EBITDA of about $600 million, and mid- to upper-single-digit adjusted net income growth. The only change to guidance is that the company now believes that start-up expenses associated with 737-CMI (crew, maintenance and insurance) will be an incremental cost not assumed in the original 2019 guide.

AAWW will hold a call to discuss these results with analysts and media at 11:00 a.m. EDT.